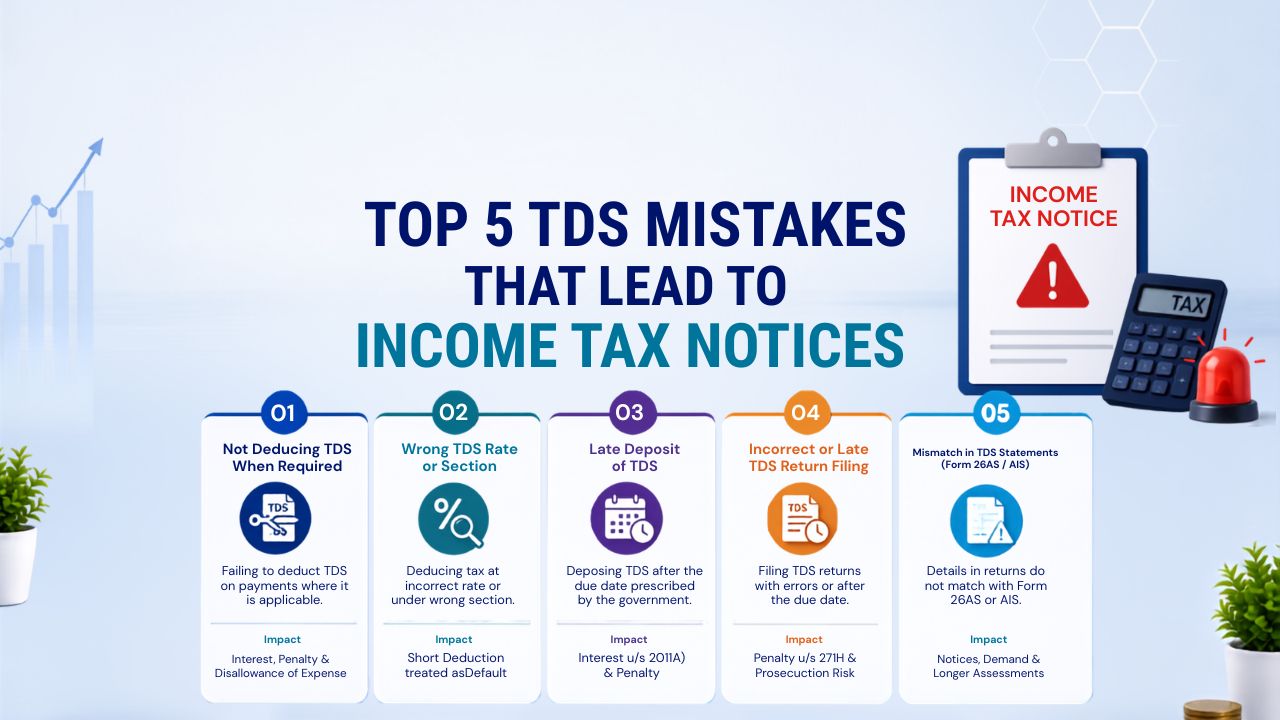

Top 5 TDS Mistakes That Lead to Income Tax Notices in 2026

TDS mistakes income tax notice connections are more common than you think – every July, I see salaried professionals who filed confidently but still received a demand from the Income Tax Department. They file their ITR confidently, assuming everything is in order since their employer has been cutting TDS from their salary all year. Then, weeks later, they get a notice from the Income Tax Department.

Nine times out of ten, it comes down to a TDS mistake. Either a mismatch in numbers, a deduction that was missed, or a deposit that was delayed by someone in the chain. The painful part is that most of these are avoidable if you know what to look for before you hit the submit button.

With the ITR filing deadline for FY 2025-26 being July 31, 2026, here are the five TDS mistakes that are generating the most income tax notices this year, and what you can do to avoid them.

Mistake 1: Not Checking Your Form 168 (Previously Form 26AS) Before Filing

This is the most common reason for receiving a Section 143(1) intimation from the Income Tax Department.

When you file your ITR, you declare TDS that has been deducted from your income across all sources: salary, bank interest, rent received, freelance payments, and so on. The department cross-checks every rupee you claim against what actually appears in their system via your Form 168 (the new name for Form 26AS under the Income Tax Act 2025).

If there is any mismatch, even by a small amount, you will get a notice asking you to explain the difference.

Why this happens: Your employer deducts TDS from your salary every month. But for that TDS to reflect in your Form 168, your employer must also deposit it with the government and file a quarterly TDS return. If they delay the return or make an error in quoting your PAN, the credit simply does not show up in your account.

What to do: Before filing your ITR, log in to the Income Tax portal and download your Form 168 (or AIS). Cross-check the TDS amounts with your salary slips, bank interest certificates, and Form 130 (the new Form 16). Only claim TDS that actually reflects in Form 168. If something is missing, follow up with your employer or payer first and ask them to correct the TDS return.

You can learn more about reading your tax credit statement in our guide on how to read Form 26AS and AIS.

Mistake 2: Missing TDS on Rent Above Rs. 50,000 Per Month

This one catches a lot of salaried professionals off guard, because most people think TDS on rent is only an issue for businesses and landlords. It is not.

Under Section 194IB of the Income Tax Act, if you are an individual (not a company, not a firm) paying rent of more than Rs. 50,000 per month, you are required to deduct TDS at 2% from the rent and deposit it with the government. This applies even if you are a salaried employee with no business income.

Example: You pay your landlord Rs. 60,000 per month for a house in Bengaluru.

Annual rent paid: Rs. 7,20,000 TDS @ 2% (Section 194IB): Rs. 14,400 This Rs. 14,400 needs to be deducted and deposited before April 30 of the following financial year.

If you skip this entirely and your landlord reports the rental income, the department will notice that you were paying rent above the threshold but no TDS was deducted. A notice under Section 201 follows, along with interest of 1% per month from the date the TDS was due.

What to do: If your monthly rent exceeds Rs. 50,000, deduct 2% TDS from the last month’s rent or from any month during the year. Deposit it using Form 26QC on the Income Tax portal. Provide your landlord with Form 16C as a TDS certificate. Note that under the new Income Tax Act 2025 framework, this will be governed by equivalent provisions when Tab 2 takes effect for TY 2026-27, but for your July 2026 ITR filing, Section 194IB rules under the 1961 Act apply.

Mistake 3: Assuming Bank FD Interest Will Automatically Have TDS Deducted

Many salaried professionals believe that if TDS has been deducted from their FD interest, the job is done and they do not need to do anything more. This thinking leads to two types of problems.

Problem A: The interest income is not declared at all. Some people simply leave FD interest out of their ITR because “TDS is already taken care of.” However, you are required to declare all income, including interest, even if TDS has been deducted. The gross interest must appear in your ITR under “Income from Other Sources.” Not declaring it is treated as concealment of income.

Problem B: TDS was not deducted because you were below the threshold, but income was still taxable. Banks deduct TDS on FD interest only if it crosses Rs. 40,000 per year (Rs. 50,000 for senior citizens) per bank (across all branches). If your interest is Rs. 35,000, no TDS will be cut. But if your total income including salary puts you in the 20% or 30% tax bracket, you still owe tax on that Rs. 35,000. The department knows your FD details via AIS (Annual Information Statement), so they will flag the mismatch.

What to do: Always declare your FD interest income in full in your ITR, regardless of whether TDS was deducted. If you owe additional tax on interest income, pay it as advance tax or self-assessment tax before filing. Our guide on advance tax explains how to calculate and pay this.

Mistake 4: Submitting an Incorrect or Outdated Form 15G or 15H

Many individuals submit Form 15G or Form 15H to their bank at the beginning of the year to prevent TDS deduction on FD interest. Under the new Income Tax Act 2025, these are now called Form 121, but the mechanism and eligibility conditions remain the same.

The mistake happens when people submit these forms even though they are not eligible.

Who can legitimately use Form 15G (or Form 121): Individuals below 60 years of age whose estimated total income for the year does not exceed the basic exemption limit of Rs. 3 lakh (under the new regime) or Rs. 2.5 lakh (under the old regime).

Who can legitimately use Form 15H (or Form 121 for seniors): Senior citizens (60 years and above) where the tax on estimated total income for the year is nil.

The problem: If your actual income for the year turns out to be higher than what you estimated when filing the form, your Form 15G or Form 15H declaration becomes invalid. TDS should have been deducted. If TDS was avoided based on an incorrect declaration and you did not pay the tax yourself, the department will issue a notice with interest under Section 201(1A).

What to do: Before submitting Form 15G or Form 15H (Form 121) at the start of a financial year, honestly estimate your total income including salary, interest, rent, and any freelance income. If there is any doubt about eligibility, it is safer to let the bank deduct TDS at 10% and then claim a refund when you file your ITR.

Mistake 5: Not Verifying Your Employer’s TDS Deposits

This mistake is entirely outside your control to cause, but entirely within your power to catch early.

Your employer deducts TDS from your salary every month under Section 192 (Section 392 under the new Act 2025). But their obligation does not stop at deduction. They must also deposit that amount with the government by the 7th of the following month (or April 30 for the March deduction) and file a quarterly TDS return.

If your employer delays the deposit or files an incorrect return with a wrong PAN or wrong TDS amount, the credit does not appear in your Form 168. You will then face a demand notice when you claim TDS credit in your ITR that the department cannot verify.

Real scenario: An employer deducts Rs. 52,500 as TDS from your annual salary (Rs. 4,375 per month for the example of Rs. 12 lakh gross salary in the new regime). If they deposit only Rs. 45,000 due to an error or cash flow problem, only Rs. 45,000 shows up in your Form 168. When you claim Rs. 52,500, there is a shortfall of Rs. 7,500 in the government’s records. You get a notice.

You can read more about how TDS on salary is calculated and what your employer should be depositing in our detailed guide on TDS on salary under Section 192.

What to do: Download your Form 168 from the Income Tax portal by the end of June 2026. Check quarterly: after July 31 (for Q1 returns), October 31 (Q2), January 31 (Q3), and May 31 (Q4). If something is missing, flag it with your employer immediately, well before the ITR deadline of July 31, 2026. Do not wait until you are about to file.

Quick Summary: 5 TDS Mistakes Income Tax Notices to Avoid

| Mistake | What Gets Triggered | Fix | |

|---|---|---|---|

| 1 | Not checking Form 168 before filing | Section 143(1) mismatch notice | Download Form 168 and AIS, cross-check before filing |

| 2 | Skipping TDS on rent above Rs. 50,000/month | Section 201 notice + 1% interest per month | Deduct 2% TDS via Form 26QC |

| 3 | Not declaring FD interest income | Demand notice for income concealment | Always report gross interest in ITR |

| 4 | Filing Form 15G/15H incorrectly | Interest under Section 201(1A) | Verify eligibility before submitting Form 121 |

| 5 | Not checking if employer deposited TDS | Demand for tax credit mismatch | Monitor Form 168 quarterly, not just at filing time |

What Happens If You Receive a TDS-Related Notice?

Most TDS notices under Section 143(1) are system-generated and resolve themselves once you respond with the correct information. Here is what to do:

Log in to the Income Tax portal and read the notice carefully. It will specify the exact discrepancy: either a TDS credit mismatch or undeclared income.

If it is a credit mismatch because your employer or bank made an error, contact the deductor immediately. They need to file a correction in their TDS return (called a correction statement). Once they do, the correct credit will reflect in your Form 168 and the notice can be resolved by filing a rectification request.

If the notice is for undeclared income, you may need to file a revised return or respond with the correct income details.

The important thing: do not ignore any notice. The department has a deadline for your response, and missing it leads to ex-parte assessment orders that are much harder to undo.

Conclusion

TDS is not just your employer’s responsibility. As a taxpayer, you are equally accountable for ensuring the right amounts are deducted, deposited, and reflected in your Form 168 before you file.

The five mistakes covered here – missing Form 168 verification, skipping TDS on rent, ignoring FD interest income, filing incorrect Form 15G or 15H, and not tracking your employer’s deposits are all avoidable with a little preparation before the July 31, 2026 deadline.

Spend 30 minutes this week downloading your Form 168 and AIS from the Income Tax portal. Cross-check every TDS entry against your salary slips and bank statements. If something does not match, you still have time to fix it before you file your ITR for FY 2025-26.

A notice from the Income Tax Department is not the end of the world, but avoiding one is always better than responding to one.

Frequently Asked Questions

Does TDS apply even if my total income is below the taxable limit?

TDS is deducted at the source based on the threshold for each payment type, regardless of your total annual income. However, you can claim a full refund of TDS deducted when you file your ITR, if your total income is below the taxable limit.

What is the penalty for late deposit of TDS?

Interest under Section 201(1A) is charged at 1.5% per month (or part of a month) from the date of deduction to the date of actual payment. This applies to the deductor, but ultimately affects your tax credit if the deposit is not made.

My employer gave me Form 130 but the TDS amount is different from Form 168. Which one should I follow?

Always follow Form 168 for claiming TDS credit in your ITR. Form 130 (your TDS certificate) is issued by your employer, but what the department recognises is only what has actually been deposited and reflected in their system. Flag the discrepancy with your employer before filing.

I missed deducting TDS on rent for the whole year. What do I do now?

Deduct the entire year’s TDS from the last rent payment and deposit it via Form 26QC before the end of the financial year. Pay applicable interest and late fees. It is better to correct this voluntarily than to wait for a notice.

Can I file my ITR even if TDS is missing from Form 168?

Yes, you can file your ITR, but you should only claim TDS that actually appears in your Form 168. If you claim more, you will get a demand notice for the difference. Pursue the correction with your employer separately and file a rectification later once it reflects.