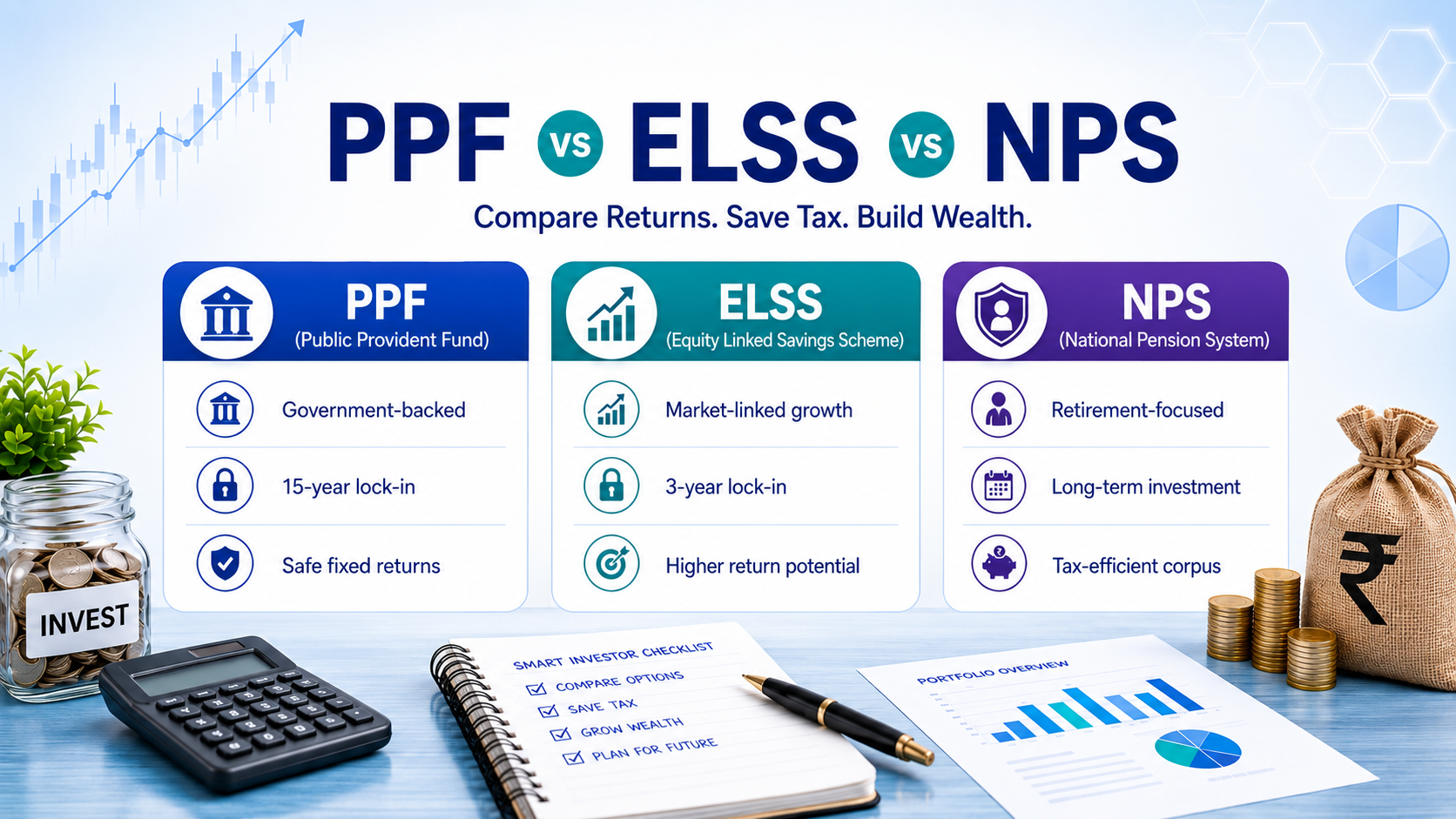

PPF vs ELSS vs NPS: Best Tax Saving Investment Comparison 2026

PPF vs ELSS vs NPS comparison is the most important 80C decision a salaried professional makes each financial year. All three are among the most popular Section 80C instruments, but they serve completely different financial goals. PPF gives you sovereign-backed tax-free returns. ELSS gives you equity growth with the shortest lock-in. NPS gives you an extra Rs. 50,000 deduction over and above the Rs. 1.5 lakh 80C limit and is the only instrument that does.

In my seven years of working with salaried professionals on tax planning, I find that most people choose one of these three based on habit or peer influence rather than a structured comparison. A 30-year-old professional and a 55-year-old professional need very different answers to this question. This guide gives you the numbers, the tax treatment, and the decision framework to choose right for your situation.

Quick Comparison: PPF vs ELSS vs NPS

| Feature | PPF | ELSS | NPS |

|---|---|---|---|

| Nature | Government savings scheme | Equity mutual fund | Pension scheme (PFRDA regulated) |

| Lock-in Period | 15 years | 3 years (shortest) | Till age 60 (longest) |

| Current Returns | 7.1% p.a. (Q1 FY 2026-27) | Market-linked (~12% CAGR historical) | Market-linked (10-12% CAGR historical) |

| Returns Guarantee | Government-declared quarterly | Not guaranteed | Not guaranteed |

| Capital Safety | 100% sovereign | No guarantee | Partial (market exposure) |

| Section 80C Deduction | Yes (old regime only) | Yes (old regime only) | Yes via 80CCD(1) (old regime only) |

| Extra Deduction | None | None | Rs. 50,000 under Section 80CCD(1B) |

| Tax on Returns | Fully tax-free (EEE) | LTCG 12.5% above Rs. 1.25L | 60% lump sum tax-free; annuity taxable |

| Premature Exit | Partial from Year 6; full at 15 years | After 3 years lock-in | Restricted till 60 |

| Minimum Investment | Rs. 500 per year | Rs. 500 via SIP | Rs. 1,000 per year |

| Maximum Investment | Rs. 1.5 lakh per year | No limit (80C on Rs.1.5L) | No limit on contribution |

| New Regime 80C Benefit | Not available | Not available | 80CCD(2) employer contribution available |

| Best For | Long-term safe tax-free savings | Equity growth, shorter horizon | Retirement corpus, extra deduction |

Under the new tax regime, the Section 80C deduction on PPF and ELSS contributions is not available. However, two important points on NPS: employer contributions to NPS under Section 80CCD(2) remain deductible even under the new regime, and PPF interest continues to be tax-free regardless of which regime you choose. If you are evaluating whether the old regime is still worth it for you, refer to my guide on the old vs new tax regime.

PPF: Public Provident Fund

The PPF interest rate for Q1 FY 2026-27 is 7.1% per annum, compounded annually. The Ministry of Finance confirmed in its quarterly notification that small-savings rates for the first quarter of FY 2026-27 would stay unchanged.

This rate has remained steady for the seventh consecutive year since the last revision on April 1, 2020.

Key Features

EEE Status: PPF is one of the very few investment instruments in India with Exempt-Exempt-Exempt (EEE) tax treatment contributions are deductible under Section 80C, interest earned is tax-free, and the maturity amount is fully exempt. This makes the effective pre-tax yield significantly higher than the stated 7.1%.

For a salaried professional in the 30% tax bracket, PPF’s 7.1% tax-free return is equivalent to a pre-tax return of approximately 10.1%. Any bank FD or debt instrument would need to offer more than 10.1% to match PPF on an after-tax basis which no bank deposit currently offers.

Deposit timing matters: PPF interest is calculated monthly on the minimum balance between the 5th and last day of each month. This means if you deposit Rs. 50,000 on April 3, the full amount earns interest for April. If you deposit the same amount on April 7, it earns zero interest for April. For lump-sum investors, depositing the full Rs. 1.5 lakh on or before April 5 every year maximises returns.

PPF Corpus: Rs. 1.5 Lakh per Year for 15 Years

| Particulars | Amount |

|---|---|

| Annual investment | Rs. 1,50,000 |

| Total invested over 15 years | Rs. 22,50,000 |

| Corpus at maturity (7.1%, 15 years) | Rs. 40,68,209 |

| Total interest earned | Rs. 18,18,209 |

| Tax on maturity | Rs. 0 (fully exempt) |

| Post-tax corpus | Rs. 40,68,209 |

PPF Liquidity

PPF is not entirely illiquid despite the 15-year tenure. Partial withdrawals are allowed from the 7th financial year onwards up to 50% of the balance at the end of the 4th year or the preceding year, whichever is lower. Loans against PPF are available from the 3rd to the 6th financial year at 1% interest above the prevailing PPF rate.

NRIs cannot open new PPF accounts. Existing accounts opened before becoming an NRI can be continued till maturity but no fresh contributions are allowed after change of residency status.

Who Should Choose PPF

PPF suits investors who want completely tax-free, risk-free long-term savings and can commit to a 15-year horizon. It is particularly powerful for those in the 20%-30% slab where the EEE advantage is most pronounced, and for those building an emergency corpus alongside their equity investments.

ELSS: Equity Linked Savings Scheme

ELSS is a diversified equity mutual fund qualifying for Section 80C deduction. It has the shortest lock-in among all 80C options at 3 years and the highest return potential when equity markets perform well.

Returns

Historical data from PFRDA shows that the equity component has delivered 10-13% CAGR over a decade. ELSS funds, being more flexibly managed than NPS equity funds, have delivered comparable or better returns historically. For this comparison, I am using a conservative 12% CAGR.

Example: Rs. 1,50,000 invested in ELSS (lump sum)

| Tenure | Maturity Value | Gain | LTCG Tax | Post-Tax Value |

|---|---|---|---|---|

| 3 years (minimum) | Rs. 2,10,739 | Rs. 60,739 | Rs. 0 | Rs. 2,10,739 |

| 5 years | Rs. 2,64,351 | Rs. 1,14,351 | Rs. 0 | Rs. 2,64,351 |

| 10 years | Rs. 4,65,877 | Rs. 3,15,877 | Rs. 24,814 | Rs. 4,41,063 |

| 15 years | Rs. 8,21,035 | Rs. 6,71,035 | Rs. 70,985 | Rs. 7,50,050 |

At 3 and 5 years, the total gain stays within the Rs. 1.25 lakh annual LTCG exemption – zero tax. At 10 and 15 years, gains exceed the exemption and attract 12.5% LTCG tax plus 4% cess on the taxable portion.

Annual SIP Rs. 1.5 lakh for 15 years at 12% CAGR:

| Particulars | Amount |

|---|---|

| Total invested | Rs. 22,50,000 |

| Corpus at 15 years | Rs. 62,62,992 |

| Total gain | Rs. 40,12,992 |

| LTCG tax (12.5% + cess on amount above Rs.1.25L) | Rs. 5,05,439 |

| Post-tax corpus | Rs. 57,57,553 |

ELSS delivers significantly higher post-tax corpus than PPF at the same tenure if returns hold at 12% but the risk is real. In a poor market cycle, 15-year ELSS returns could be closer to 8%-9%.

ELSS funds are open-ended equity mutual funds that qualify for deduction under Section 123 of the New Income Tax Act 2025; you can verify the current list of qualifying funds on the AMFI India website.

Who Should Choose ELSS

ELSS suits investors in the 20%-30% tax slab with a long investment horizon of 7 years or more, who are comfortable with equity market volatility and want the flexibility of a 3-year lock-in rather than being locked in till retirement.

NPS: National Pension System

NPS is where this comparison gets more complex and more interesting. NPS is the only 80C instrument that offers an additional Rs. 50,000 deduction under Section 80CCD(1B) over and above the Rs. 1.5 lakh 80C limit. This makes the total deduction potential Rs. 2 lakh per year.

Deduction Structure

| Deduction | Section | Limit | Applicable Regime |

|---|---|---|---|

| Employee’s own contribution | 80CCD(1) within 80CCE | Up to Rs. 1.5 lakh (within 80C) | Old regime only |

| Extra NPS contribution | 80CCD(1B) | Additional Rs. 50,000 | Old regime only |

| Employer’s NPS contribution | 80CCD(2) | Up to 10% of basic+DA | Both old and new regime |

For a salaried professional in the 30% bracket contributing Rs. 2 lakh to NPS annually, the total tax saving is Rs. 62,400 (30% plus cess on Rs. 2 lakh) compared to Rs. 46,800 from PPF or ELSS. This Rs. 15,600 extra tax saving every year, invested elsewhere, compounds meaningfully over time.

Returns

NPS typically delivers annual returns ranging from 9% to 12%, depending on the investor’s asset allocation and fund performance. Tier 1 equity investments have shown average returns of around 11.2% over 5 years.

NPS offers four asset classes: Scheme E (equity, highest return potential), Scheme G (government securities, stable), Scheme C (corporate bonds), and Scheme A (alternative assets discontinued from January 2026). For younger investors, an equity-heavy allocation is generally recommended.

Annual SIP Rs. 1.5 lakh for 15 years at 10% CAGR (mixed allocation):

| Particulars | Amount |

|---|---|

| Total invested | Rs. 22,50,000 |

| Corpus at Year 15 | Rs. 52,42,459 |

| Lump sum withdrawal (60%, tax-free) | Rs. 31,45,476 |

| Compulsory annuity (40%) | Rs. 20,96,984 |

| Monthly annuity income (at 5.5%) | ~Rs. 9,611/month |

| Annual annuity income (taxable at slab) | ~Rs. 1,15,334 |

NPS Tax Treatment: The Catch

This is where NPS loses some of its shine for investors not focused on retirement.

At maturity (age 60): 60% of the corpus can be withdrawn as a lump sum fully tax-free. The remaining 40% must mandatorily be used to purchase an annuity. The annuity income is taxable at your applicable slab rate every year.

For a 30% slab investor receiving Rs. 1,15,334 in annual annuity income, tax at 30% plus cess works out to approximately Rs. 36,000 per year. This ongoing tax on annuity income is the structural disadvantage of NPS compared to PPF’s fully exempt maturity.

Before age 60 (partial withdrawal): After 3 years in NPS, you can withdraw up to 25% of your own contributions for specific purposes – higher education, home purchase, critical illness. This is allowed three times during the tenure. Full withdrawal before 60 is not permitted except in the case of terminal illness or death.

Who Should Choose NPS

NPS suits investors who specifically want to build a retirement corpus, are willing to accept the annuity structure, and want to maximise deductions by using the extra Rs. 50,000 under Section 80CCD(1B). It is also particularly valuable for those whose employers contribute to NPS – the employer’s contribution under Section 80CCD(2) is deductible even under the new tax regime, making NPS the only 80C-type instrument with any new regime benefit.

Returns Comparison: Rs. 1.5 Lakh Per Year for 15 Years

| PPF | ELSS (12% CAGR) | NPS (10% CAGR) | |

|---|---|---|---|

| Total Invested | Rs. 22,50,000 | Rs. 22,50,000 | Rs. 22,50,000 |

| Gross Corpus | Rs. 40,68,209 | Rs. 62,62,992 | Rs. 52,42,459 |

| Tax on Corpus | Rs. 0 | Rs. 5,05,439 | 40% annuity taxable at slab |

| Post-Tax Lump Sum | Rs. 40,68,209 | Rs. 57,57,553 | Rs. 31,45,476 (60%) |

| Ongoing Post-Retirement Income | Nil | Nil | ~Rs. 9,611/month (taxable) |

ELSS delivers the highest post-tax lump sum at 12% CAGR. But this is market-dependent. PPF delivers the most predictable post-tax outcome. NPS sits between the two on return potential, but the compulsory annuity structure reduces the effective lump sum at retirement.

Tax Efficiency Comparison (30% Tax Bracket)

| PPF | ELSS | NPS | |

|---|---|---|---|

| Annual 80C tax saving (Rs.1.5L) | Rs. 46,800 | Rs. 46,800 | Rs. 46,800 |

| Extra 80CCD(1B) tax saving (Rs.50K) | Nil | Nil | Rs. 15,600 |

| Total annual tax saving | Rs. 46,800 | Rs. 46,800 | Rs. 62,400 |

| Tax on returns | Nil (EEE) | LTCG 12.5% on gains above Rs.1.25L | 40% annuity taxable at slab |

| Tax on maturity/withdrawal | Nil | LTCG on gain above Rs.1.25L | 60% lump sum tax-free |

| New regime benefit | Interest exempt (no 80C) | None | 80CCD(2) employer contribution |

PPF wins on tax efficiency at the returns stage – 100% tax-free maturity. ELSS wins on flexibility with only LTCG tax at a preferential 12.5% rate. NPS wins on the entry-stage deduction – Rs. 62,400 annual tax saving vs Rs. 46,800 for the other two.

Who Should Choose What: Decision Framework

Choose PPF if:

- You are in the old tax regime and want completely tax-free returns

- You have a 15-year horizon and want sovereign-backed safety

- You are in the 20%-30% slab where the EEE advantage compounds significantly

- You want a guaranteed return that outperforms FDs on post-tax basis

- You are building a fixed-income foundation to balance equity investments elsewhere

Choose ELSS if:

- You are in the old tax regime and want equity market exposure within 80C

- Your investment horizon is at least 7 years (3-year lock-in is the minimum, not the ideal)

- You are comfortable with market volatility

- You want the flexibility to redeem after 3 years if needed

- You already have adequate debt exposure through PPF or EPF

Choose NPS if:

- You specifically want to build a retirement corpus and accept the pension structure

- You want the extra Rs. 50,000 deduction under Section 80CCD(1B)

- Your employer contributes to NPS – the 80CCD(2) benefit survives even in the new regime

- You are in the 30% slab and want to push your total 80C-type deduction to Rs. 2 lakh

- You are disciplined enough to not need the corpus before retirement

Combination approach used by most 30% slab investors:

- Rs. 50,000 to NPS for the extra 80CCD(1B) deduction

- Rs. 1,00,000 to ELSS for equity growth within 80C

- PPF for any remaining fixed-income allocation outside 80C

- This maximises both tax saving and long-term growth

For a complete breakdown of all Section 80C instruments and how to use the full Rs. 1.5 lakh limit, refer to my guide on Section 80C deductions. For overall tax saving strategies covering both regimes, refer to tax saving tips for salaried employees.

NPS vs PPF: Which Is Better for a 30-Year-Old?

This is the most common question I get from salaried professionals starting their tax planning journey.

A 30-year-old has 30 years till retirement. At 10% CAGR, every Rs. 1 invested in NPS at 30 becomes Rs. 17.45 at 60. At 7.1% in PPF, every Rs. 1 invested becomes Rs. 2.80 at maturity after 15 years. The longer compounding horizon makes NPS’s equity component particularly powerful for younger investors.

However, 40% of the NPS corpus at retirement is locked into an annuity – which reduces the effective lump sum. For a 30-year-old, my recommendation is to use NPS primarily for the Rs. 50,000 extra deduction and use ELSS or direct equity for the primary long-term wealth creation.

Conclusion

PPF, ELSS, and NPS are complementary instruments rather than direct substitutes. PPF gives you sovereign-backed EEE returns at 7.1% – the most tax-efficient fixed-income instrument available. ELSS gives you equity growth with a short 3-year lock-in and preferential LTCG tax treatment. NPS gives you the unique Rs. 50,000 extra deduction under Section 80CCD(1B) and powerful long-term retirement compounding, offset by the annuity structure at maturity.

For a salaried professional in the 30% tax bracket under the old regime, the most tax-efficient combination in 2026 is to use Rs. 50,000 in NPS for the extra deduction, Rs. 1 lakh in ELSS for equity growth within 80C, and maintain PPF for the tax-free fixed-income component.

For a complete picture of how your salary, these investments, and your total tax liability interact, refer to my Complete Income Tax Guide for India.

Frequently Asked Questions

Can I invest in all three – PPF, ELSS, and NPS – simultaneously? Yes. You can split your investments across all three. The 80C limit of Rs. 1.5 lakh is cumulative across all eligible instruments. NPS gets an additional Rs. 50,000 under Section 80CCD(1B) over and above this limit.

Under the new tax regime, should I still invest in PPF? PPF interest continues to be fully tax-free under both old and new tax regimes. The 80C deduction on contributions is not available under the new regime, but the investment itself remains attractive for its tax-free compounding. It is worth continuing if you already have a PPF account.

Is NPS better than ELSS for tax saving? NPS provides a larger initial tax deduction (up to Rs. 2 lakh vs Rs. 1.5 lakh for ELSS). But ELSS gives complete flexibility at redemption, while NPS mandates 40% annuity at retirement. For pure tax saving, NPS wins. For long-term wealth flexibility, ELSS wins.

What is the NPS fund management charge? NPS fund management charges are capped at 0.09% per annum – significantly lower than most equity mutual funds. Over a 30-year retirement horizon, this cost advantage compounds meaningfully.

Can NRIs invest in PPF or NPS? NRIs cannot open new PPF accounts. Existing PPF accounts can be continued till maturity. NRIs can invest in NPS if they have an active NPS account, but they cannot claim 80C deductions since they may not be filing Indian income tax returns.

Is PPF available under the new tax regime? The Section 80C deduction on PPF contributions is not available under the new regime. However, the interest earned and maturity proceeds remain fully tax-free irrespective of which regime you choose.