Form 15G vs Form 15H vs Form 121: Who Should File Which in 2026

Your FD just matured. The bank credited Rs. 42,000 as interest, but only Rs. 37,800 landed in your account. Rs. 4,200 was quietly deducted as TDS.

The frustrating part? You did not owe that tax. Your income was below the taxable limit. You just forgot to submit a simple form at the start of the year.

Form 15G and Form 15H exist precisely to prevent this. They are declarations you submit to your bank or deductor telling them that your income is below the taxable limit, so please do not deduct TDS. And from Tax Year 2026-27 onwards, both these forms will be replaced by a single unified Form 121 under the New Income Tax Act 2025.

In my 7 years of working with salaried professionals and retirees, I have seen this mistake repeat every April. People either do not know these forms exist, or they confuse 15G with 15H and submit the wrong one. This guide will make sure that does not happen to you.

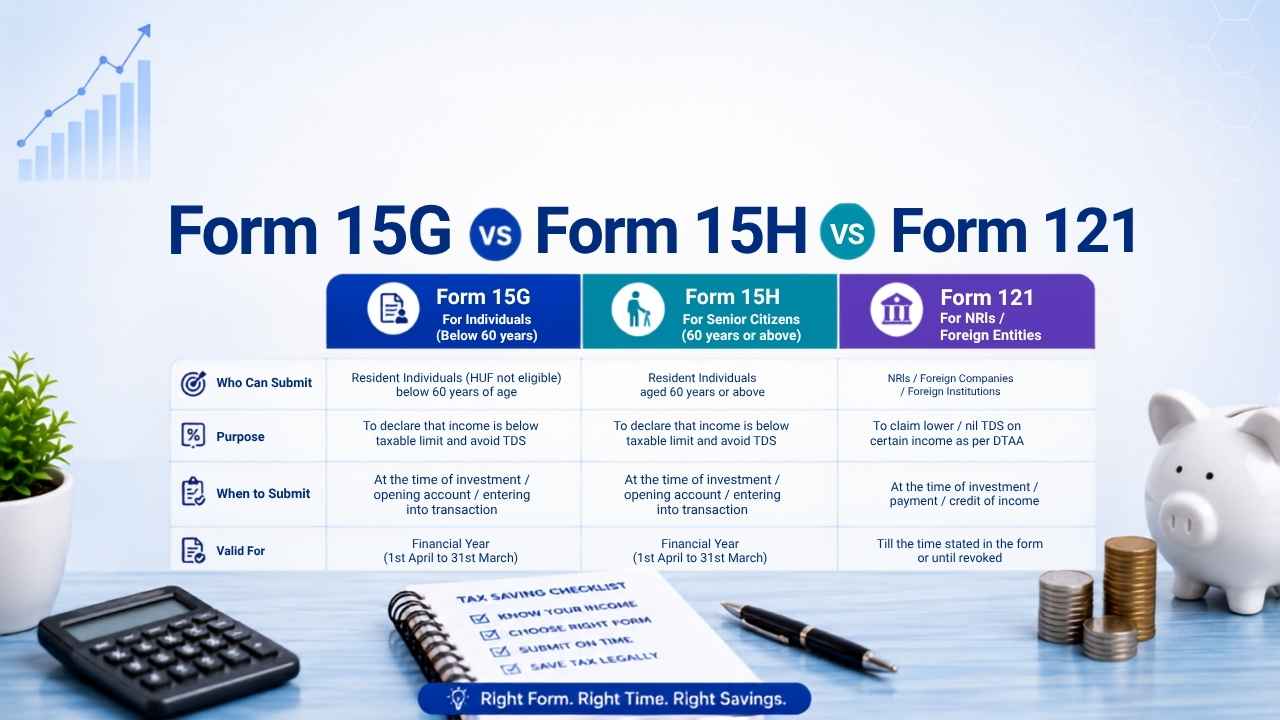

What is Form 15G?

Form 15G is a self-declaration form submitted by resident individuals below 60 years of age to request NIL TDS deduction on certain income. When you submit this form to your bank or deductor, you are declaring that your total income for the year is below the basic exemption limit and therefore no tax should be deducted at source.

Two conditions must be satisfied to file Form 15G. First, your estimated total income for the financial year must be below the basic exemption limit: Rs. 2,50,000 under the old tax regime or Rs. 3,00,000 under the new tax regime. Second, the tax on your estimated total income for the year must be NIL.

Form 15G can also be filed by Hindu Undivided Families, trusts, and associations of persons. However, companies and partnership firms cannot file this form.

The most common situations where you would file Form 15G are when your FD interest is likely to cross Rs. 40,000 in a year but your total income is still below the taxable limit, or when you are withdrawing from your EPF before five years of service and the withdrawal exceeds Rs. 50,000.

What is Form 15H?

Form 15H is a self-declaration form submitted by resident individuals who are 60 years of age or older, meaning senior citizens. The purpose is the same as Form 15G , to request NIL TDS , but the eligibility condition is different and significantly more flexible.

For Form 15H, the only condition is that the tax calculated on your estimated total income for the year should be NIL. There is no upper income cap. This means a senior citizen with income above the basic exemption limit can still file Form 15H, provided their total tax liability after all deductions and exemptions works out to zero.

This flexibility exists because senior citizens have access to a higher basic exemption of Rs. 3,00,000, a higher TDS threshold on FD interest of Rs. 1,00,000, and additional deductions under Section 80D and Section 80TTB. When all these are applied, many senior citizens end up with zero tax liability even on income of Rs. 4 lakh or Rs. 5 lakh.

What is Form 121?

Form 121 is the new unified NIL TDS declaration form introduced under the New Income Tax Act 2025. It replaces both Form 15G and Form 15H with a single form that covers all categories of taxpayers.

The key thing to understand here is timing. For FY 2025-26, which you are filing in July 2026, you are still under Tab 1 on the Income Tax Portal, which means the old Income Tax Act 1961 applies. So you will use Form 15G or Form 15H as applicable for this year.

Form 121 will come into use from Tax Year 2026-27 onwards, which is the first year covered under Tab 2 of the portal and the New Income Tax Act 2025. You can read more about this transition in the complete guide on New Income Tax Act 2025 vs Income Tax Act 1961.

Form 15G vs Form 15H vs Form 121: Comparison Table

| Parameter | Form 15G | Form 15H | Form 121 |

|---|---|---|---|

| Who files | Individuals below 60, HUF, Trust, AOP | Resident individuals 60 years or above | All categories (replaces both) |

| Age condition | Below 60 years | 60 years or above | No separate age-based form |

| Income condition | Total income below basic exemption limit | Tax on total income must be NIL | Tax on total income must be NIL |

| Income cap | Yes, below Rs. 2,50,000 (old) or Rs. 3,00,000 (new regime) | No fixed cap | No fixed cap |

| Applicable law | Income Tax Act 1961 | Income Tax Act 1961 | New Income Tax Act 2025 |

| Applicable from | Currently in use | Currently in use | Tax Year 2026-27 onwards |

| Valid for | One financial year | One financial year | One tax year |

| Submitted to | Bank, EPFO, deductor | Bank, EPFO, deductor | Bank, EPFO, deductor |

Who Should File Which Form in 2026?

This is the question most people get wrong. Here is a simple way to decide:

Are you below 60 years of age? File Form 15G, but only if your total annual income is below Rs. 2,50,000 (old regime) or Rs. 3,00,000 (new regime). If your income is above this, you cannot file Form 15G even if you end up owing zero tax due to deductions.

Are you 60 years or above? File Form 15H, if your total tax liability after all deductions works out to NIL. Your income can be higher than the basic exemption limit as long as the final tax is zero.

Are you filing for Tax Year 2026-27 (from April 2026 income)? Use Form 121, which covers all categories in a single form.

Practical Examples: Who Can and Cannot File

Can file Form 15G

A 35-year-old with total annual income of Rs. 2,40,000 under the old regime can file Form 15G. The income is below the Rs. 2,50,000 basic exemption limit, so no tax is due and TDS should not be deducted on FD interest.

A 45-year-old homemaker with only FD interest income of Rs. 60,000 for the year can file Form 15G. Even though TDS would otherwise be deducted since interest crosses Rs. 40,000, the total income is well below the basic exemption limit.

Cannot file Form 15G

A 38-year-old with salary income of Rs. 3,50,000 cannot file Form 15G even if deductions bring the taxable income to zero. The total income before deductions exceeds the basic exemption limit, which disqualifies them. This is a very common mistake I see people make , they confuse taxable income with total income for this condition.

Can file Form 15H

A 62-year-old retiree receiving pension of Rs. 3,50,000 and claiming Rs. 50,000 deduction under Section 80D on health insurance. Net taxable income is Rs. 3,00,000. Tax on Rs. 3,00,000 for a senior citizen is NIL since the basic exemption itself is Rs. 3,00,000. This person can file Form 15H.

Cannot file Form 15H

A 65-year-old with total income of Rs. 8,00,000 and deductions of Rs. 1,50,000. Taxable income is Rs. 6,50,000. Tax calculation under old regime: NIL on first Rs. 3,00,000, 5% on next Rs. 2,00,000 equals Rs. 10,000, and 20% on remaining Rs. 1,50,000 equals Rs. 30,000. Total tax comes to Rs. 40,000. Since the tax liability is not NIL, this person cannot file Form 15H.

Where and When to Submit These Forms

When to submit: Always submit at the beginning of the financial year, ideally in April. If you submit after TDS has already been deducted, the deduction stands and you will need to claim a refund when you file your ITR.

Where to submit: Submit to the deductor directly: your bank branch for FD interest, EPFO for EPF withdrawal, the company for dividend income. Most major banks now allow online submission of Form 15G and Form 15H through net banking or their mobile apps.

One form per deductor: If you have FDs in three different banks, you need to submit Form 15G or Form 15H to all three separately. One submission does not cover multiple deductors.

Validity: These forms are valid for one financial year only. You must submit fresh forms every April. Many people submit once and assume it carries forward , it does not.

Key TDS Sections Where These Forms Apply

Form 15G and Form 15H are most commonly used in the following situations:

Section 194A: Interest on fixed deposits and recurring deposits: TDS is deducted if interest exceeds Rs. 40,000 in a year for regular taxpayers and Rs. 1,00,000 for senior citizens. Submitting Form 15G or Form 15H stops this deduction. You can read how TDS works across different payment types in the TDS vs TCS guide.

Section 192A: EPF withdrawal before 5 years: If you withdraw more than Rs. 50,000 from EPF before completing five years of service, TDS at 10% is deducted. Form 15G stops this if your income is below the exemption limit.

Section 194: Dividend income: If dividend income from shares or mutual funds exceeds Rs. 5,000 in a year, TDS at 10% applies. Form 15G or Form 15H can be submitted to the company or fund house.

Section 194DA: Life insurance maturity proceeds: If the maturity amount of a life insurance policy is taxable and exceeds Rs. 1,00,000, TDS at 5% applies. Form 15G can be submitted to the insurer.

Section 194EE: NSS withdrawals: Withdrawals from National Savings Scheme attract TDS at 10%. Form 15G can be submitted to the post office to avoid this.

What Happens If You File the Wrong Form?

Filing Form 15G when you should not, for example, when your income exceeds the basic exemption limit , is treated as filing a false declaration. Under Section 277 of the Income Tax Act 1961, this can attract prosecution and a fine. It is not a minor paperwork error.

If you are unsure whether you qualify, the safer option is to let TDS be deducted and claim it as a refund when you file your ITR. Incorrect Form 15G filings have led to tax notices for several of my clients over the years.

Form 15G, 15H and the New Income Tax Act 2025

Under the New Income Tax Act 2025, both forms are consolidated into Form 121. The purpose remains identical : a declaration to the deductor that no TDS should be deducted since the tax liability is NIL.

For the current ITR filing season in July 2026, covering FY 2025-26, you continue using Form 15G and Form 15H as before. Form 121 will become relevant when income earned from April 1, 2026 onwards is filed under Tax Year 2026-27 in July 2027.

This transition is part of the broader simplification under the new act, where multiple forms serving similar purposes have been merged. You can check the complete income tax guide for India for a full overview of how the new act is changing the filing landscape.

How to Submit Form 15G and Form 15H Online

Most banks today accept these forms digitally. Here is how it typically works for FD interest:

Log in to your bank’s net banking portal and look for the TDS or tax section. Most banks have a dedicated option to submit Form 15G or Form 15H. Fill in your PAN, estimated income, and income from the specific investment. Submit and download the acknowledgement number.

For EPFO submissions, log in to the EPFO member portal using your UAN and submit Form 15G under the claim section before initiating an EPF withdrawal.

The Income Tax Portal at incometax.gov.in does not accept these forms directly ; they go to the deductor, who then reports them to the income tax department in their quarterly TDS returns.

Common Mistakes to Avoid

Submitting too late. Once TDS is deducted, the form cannot reverse it. You will have to wait for your refund after filing ITR.

Confusing total income with taxable income for Form 15G. The condition for Form 15G is based on total income before deductions, not net taxable income. Many people get this wrong and file Form 15G incorrectly.

Not submitting to all deductors. One Form 15G to one bank does not protect you from TDS at another bank or institution.

Skipping the annual resubmission. These forms expire at the end of each financial year. A fresh submission is needed every April.

Assuming the new regime changes eligibility for 15G. Under the new tax regime, the basic exemption is Rs. 3,00,000. If you choose the new regime and your income is below Rs. 3,00,000, you can file Form 15G. But remember the rebate under Section 87A that makes income up to Rs. 12,00,000 effectively zero-tax does not help here , that rebate does not change your eligibility for Form 15G. The condition remains that income must be below the basic exemption limit.

Frequently Asked Questions

Can a salaried person with income of Rs. 5 lakh file Form 15G? No. Even if deductions bring the taxable income to zero, the total income of Rs. 5 lakh exceeds the basic exemption limit. Form 15G cannot be filed in this case. TDS will be deducted and you will need to claim it as a refund in your ITR.

I am 59 years old. Can I file Form 15H? No. Form 15H is only for individuals who are 60 years or above. At 59, you must use Form 15G if eligible.

Does submitting Form 15G mean I do not need to file ITR? No. Form 15G only prevents TDS deduction. Your obligation to file an ITR remains if your income exceeds the basic exemption limit or if you meet any other ITR filing condition. The two are completely separate requirements.

What if I submitted Form 15G but TDS was still deducted? Contact your bank or deductor with proof of submission. If the deduction was an error on their part, they can rectify it in their TDS return. Alternatively, claim the credit when you file your ITR and get a refund.

Will Form 15G and Form 15H still work in April 2026? Yes. For income earned in FY 2025-26, you continue using Form 15G and Form 15H. Form 121 applies only to Tax Year 2026-27 income under the New Income Tax Act 2025.

Can I submit Form 15G for multiple FDs at the same bank? Yes, but you need to mention all FDs and the aggregate interest income in the single declaration. Submitting one form per FD at the same bank is not required ; one form covering all FDs at that branch is sufficient.

What is the penalty for wrongly filing Form 15G? Filing a false declaration under Form 15G is an offence under Section 277 of the Income Tax Act. It can attract prosecution and rigorous imprisonment from three months to two years, along with a fine. Always ensure you genuinely qualify before submitting.