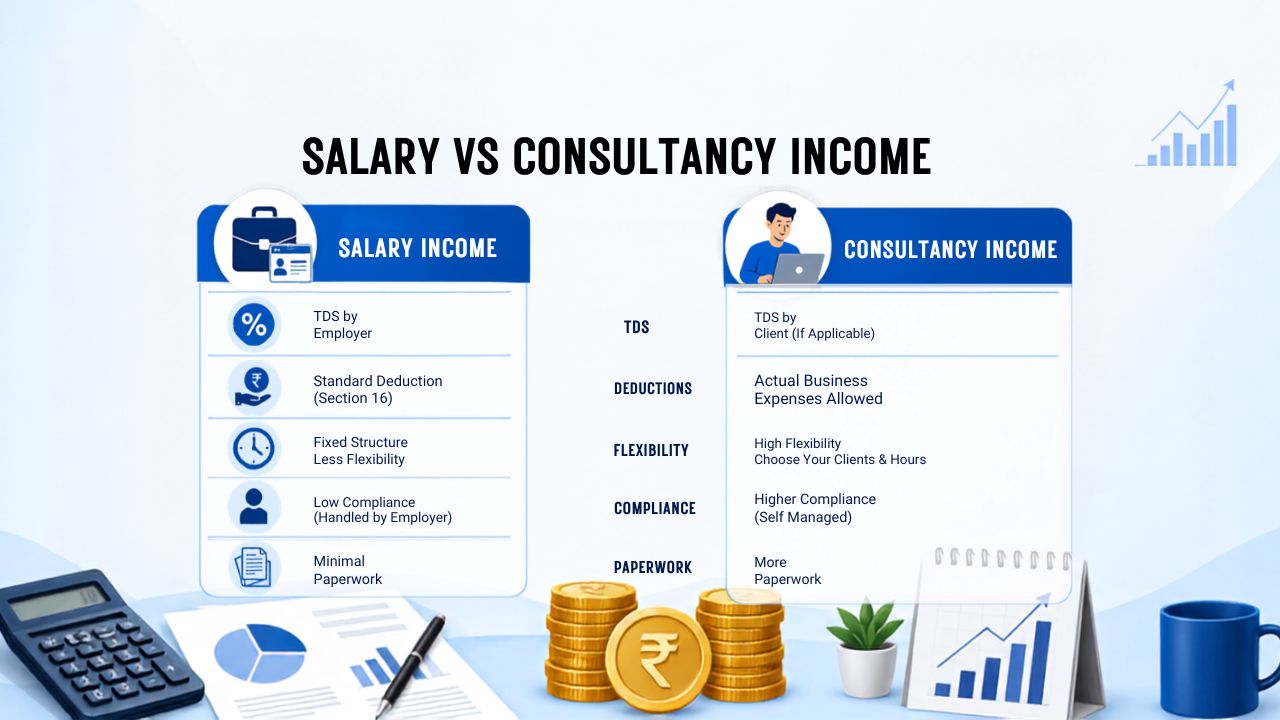

Salary vs Consultancy Income: Tax Treatment Comparison 2026

Salary vs consultancy income tax comparison 2026 is one of the most relevant questions for professionals in India right now. Whether you are a salaried employee thinking about going independent, a consultant evaluating your tax efficiency, or someone who does both, the tax treatment of these two income types is fundamentally different in ways that directly affect your take-home income.

Table of Contents

In my 7 years of working with salaried professionals and independent consultants, I have seen many people switch between these arrangements without fully understanding the tax implications. The differences go beyond just TDS rates. They affect which ITR form you file, whether GST applies to you, how you pay advance tax, and what deductions you can claim.

Here is a complete side-by-side breakdown of how salary and consultancy income are taxed in FY 2025-26.

The Fundamental Difference: Which Tax Head Applies

This is where everything begins. The income head determines which sections of the Income Tax Act apply to you, what deductions are available, and how your tax is calculated.

Salary income is taxed under “Income from Salaries” (Sections 15 to 17 of the Income Tax Act 1961). You are an employee. Your employer deducts TDS every month under Section 192 (Section 392 under the new Act 2025) and deposits it with the government. You receive Form 16 (now called Form 130 under the new Income Tax Act 2025) at the end of the year showing your salary and TDS details.

Consultancy income is taxed under “Profits and Gains of Business or Profession” (PGBP). You are self-employed. Your clients deduct TDS under Section 194J before paying you. You are responsible for calculating and paying your own advance tax, maintaining records, and filing GST returns if applicable.

This single difference in income head cascades into almost every other aspect of tax treatment.

TDS: Who Deducts, How Much, and When

For salaried employees: Your employer deducts TDS every month based on your estimated annual tax liability. The rate varies based on your income and the tax regime you choose. You do not need to do anything – TDS is handled entirely by your employer. For more on how this works, see our TDS on salary Section 192 guide.

For consultants: Your clients deduct TDS under Section 194J before paying your invoice. The TDS rate depends on the nature of your services:

Professional services (legal, medical, accounting, architectural): 10% TDS. Technical services (IT, software, engineering consultancy): 2% TDS.

The threshold for TDS deduction under Section 194J is Rs. 30,000 per year per client. If a single client pays you less than Rs. 30,000 in a year, they do not deduct TDS.

Key difference: As a consultant, TDS deducted by clients may not fully cover your actual tax liability. You are responsible for paying the balance through advance tax.

Standard Deduction: Available for Salary, Not Consultancy

One of the most straightforward differences between the two income types is the standard deduction.

Salaried employees get a flat standard deduction of Rs. 75,000 under the new tax regime and Rs. 50,000 under the old tax regime. This is automatic – no proof required.

Consultants do not get a standard deduction on their professional income. There is no equivalent flat deduction available.

However, consultants have something far more powerful: actual business expense deductions or the Section 44ADA presumptive scheme, both of which can reduce taxable income far more than a flat Rs. 75,000 deduction.

The Section 44ADA Advantage: Consultancy’s Biggest Tax Benefit

Section 44ADA is the most important tax provision for independent consultants and freelancers in India. Under this scheme, if your gross professional receipts are up to Rs. 75 lakh in a year, you can declare 50% of your receipts as your taxable income. The remaining 50% is automatically treated as expenses, with no need to maintain detailed books or prove actual expenses.

Note that the Rs. 75 lakh threshold applies when cash receipts do not exceed 5% of your total gross receipts. If cash receipts are higher, the applicable limit is Rs. 50 lakh.

Who can use Section 44ADA: Professionals in specified fields including legal, medical, engineering, architecture, accountancy, technical consultancy, interior decoration, information technology, and company secretaries.

Tax Calculation Example: Rs. 25 Lakh Income

Let us compare the actual tax liability on the same Rs. 25 lakh gross income under salary and consultancy arrangements using the new tax regime for FY 2025-26.

Salaried employee – new tax regime:

Gross salary: Rs. 25,00,000

Standard deduction: Rs. 75,000

Taxable income: Rs. 24,25,000

Tax calculation:

- Rs. 4 lakh to Rs. 8 lakh at 5%: Rs. 20,000

- Rs. 8 lakh to Rs. 12 lakh at 10%: Rs. 40,000

- Rs. 12 lakh to Rs. 16 lakh at 15%: Rs. 60,000

- Rs. 16 lakh to Rs. 20 lakh at 20%: Rs. 80,000

- Rs. 20 lakh to Rs. 24 lakh at 25%: Rs. 1,00,000

- Rs. 24 lakh to Rs. 24.25 lakh at 30%: Rs. 7,500

Total tax: Rs. 3,07,500

Cess at 4%: Rs. 12,300

Total tax payable: Rs. 3,19,800

Consultant under Section 44AD – new tax regime:

Gross receipts: Rs. 25,00,000

Presumptive income at 50%: Rs. 12,50,000

Tax calculation:

- Rs. 4 lakh to Rs. 8 lakh at 5%: Rs. 20,000

- Rs. 8 lakh to Rs. 12 lakh at 10%: Rs. 40,000

- Rs. 12 lakh to Rs. 12.5 lakh at 15%: Rs. 7,500

Total tax: Rs. 67,500

Cess at 4%: Rs. 2,700

Total tax payable: Rs. 70,200

The consultant saves Rs. 2,49,600 in income tax on the same Rs. 25 lakh income. This is the core tax advantage of consultancy income under Section 44ADA.

Note: The Section 87A rebate (zero tax for income up to Rs. 12 lakh under the new regime) does not apply in this example since both taxable incomes exceed Rs. 12 lakh.

Business Expense Deductions: Consultancy Wins Clearly

If you do not opt for Section 44ADA and instead maintain regular books of accounts, you can deduct all legitimate business expenses from your consultancy income before calculating tax.

Expenses consultants can deduct:

Rent for office space or a dedicated portion of home rent used for work. Internet and phone bills. Laptop, equipment, and software purchased for work (depreciation). Travel expenses for client meetings. Professional subscriptions and memberships. Salaries paid to assistants or support staff. Accounting and legal fees. Marketing and advertising costs.

Salaried employees cannot claim any of these deductions, regardless of whether they actually spend money on such items for work. The only deduction available is the flat standard deduction.

Under the old tax regime, salaried employees can additionally claim HRA, LTA, Section 80C investments, and Section 80D health insurance. But these are personal deductions, not work-related expense deductions.

You can compare how deductions work across both regimes in our old vs new tax regime guide.

GST: A Compliance Layer That Only Consultants Face

This is one of the most important practical differences that many people overlook when comparing salary and consultancy income.

Salary: GST does not apply. The employer-employee relationship is outside the scope of GST. Your salary is not subject to GST regardless of the amount.

Consultancy: If your annual professional receipts exceed Rs. 20 lakh (Rs. 10 lakh in special category states), GST registration is mandatory. You can verify GST applicability and file returns on the GST portal. The applicable GST rate on consultancy and professional services is 18%.

What this means practically: you need to raise GST invoices to your clients, collect 18% GST over and above your fee, file GSTR-1 and GSTR-3B returns, and deposit the collected GST with the government.

GST does not reduce your earnings directly since you collect it from clients. Your clients can claim input tax credit on the GST you charge them in B2B arrangements, so it is generally not a deal-breaker for business consulting. For individual clients who cannot claim ITC, the effective cost is higher.

Advance Tax: Employer Handles It for Salary, You Handle It for Consultancy

Salaried employees: Your employer calculates and deducts TDS every month. In most cases, you do not need to worry about advance tax unless you have significant additional income from other sources such as interest, rent, or capital gains that pushes your remaining tax liability above Rs. 10,000.

Consultants: You must calculate and pay advance tax yourself in four instalments during the financial year:

By June 15: At least 15% of estimated annual tax. By September 15: At least 45% of estimated annual tax. By December 15: At least 75% of estimated annual tax. By March 15: 100% of estimated annual tax.

One exception: Consultants opting for Section 44ADA get a relaxation. They can pay their entire advance tax in a single instalment by March 15 instead of spreading it across four dates.

Missing advance tax instalments attracts interest under Section 234B and Section 234C. Our advance tax payment guide explains how to calculate and pay advance tax correctly.

ITR Form: Different Forms for Different Income Types

Salaried employees:

- ITR-1 (Sahaj): If salary is the only income and total income is up to Rs. 50 lakh

- ITR-2: If you have salary plus capital gains, foreign income, or multiple house properties

Consultants:

- ITR-4 (Sugam): If opting for presumptive taxation under Section 44ADA and total income is up to Rs. 50 lakh

- ITR-3: If maintaining regular books of accounts or if total income exceeds Rs. 50 lakh

Filing the wrong ITR form results in a defective return notice under Section 139(9). The ITR filing last date for FY 2025-26 is July 31, 2026.

EPF and Social Security: Only for Salaried Employees

Salaried employees in establishments with 20 or more employees are covered under EPF (Employees Provident Fund). Both employee (12% of basic salary) and employer (12% of basic salary) contribute to EPF. While this reduces your take-home salary, it builds a retirement corpus that is completely exempt from tax after 5 years of continuous service.

Consultants have no EPF obligation. There is no employer contributing on their behalf. However, consultants can voluntarily invest in NPS (National Pension System) to build retirement savings and claim deductions under Section 80CCD(1B) for up to Rs. 50,000 per year under the old tax regime.

Tax Audit: When It Becomes Mandatory for Consultants

Salaried employees never require a tax audit regardless of their income level.

Consultants face a mandatory tax audit under Section 44AB if their gross professional receipts exceed Rs. 75 lakh in a financial year. If you opt out of Section 44ADA and want to declare profits below 50% of receipts, you also need a tax audit even if receipts are below Rs. 75 lakh.

A tax audit must be conducted by a Chartered Accountant and the audit report must be filed by October 31, 2026 for FY 2025-26.

Both Salary and Consultancy in the Same Year

Many professionals have both salary income and consultancy income in the same year. This happens commonly when someone does part-time consulting alongside a salaried job, or transitions from employment to consulting mid-year.

In this case:

- Salary is taxed under “Income from Salaries”

- Consultancy income is taxed under PGBP

- Both incomes are clubbed for computing total tax liability

- Section 44ADA remains available for the consultancy portion even if you have salary income

- You can file ITR-4 if you are using Section 44ADA and your total income is up to Rs. 50 lakh

- ITR-3 is required only if your total income exceeds Rs. 50 lakh or you are maintaining regular books of accounts

- Advance tax becomes your responsibility for the consultancy portion

Note: If you have non-professional business income (such as trading income) alongside consultancy, Section 44ADA is not available. It is only unavailable when non-professional business income is involved, not salary income.

Our income tax guide for freelancers covers this mixed income situation in more detail.

Complete Comparison Table

| Factor | Salary | Consultancy |

|---|---|---|

| Income head | Income from Salaries | PGBP |

| TDS section | Section 192 | Section 194J (2% or 10%) |

| TDS responsibility | Employer | Client |

| Standard deduction | Rs. 75,000 (new) / Rs. 50,000 (old) | Not available |

| Presumptive scheme | Not available | Section 44ADA – 50% of receipts |

| Business expenses | Not deductible | Fully deductible |

| GST | Not applicable | 18% if receipts exceed Rs. 20 lakh |

| Advance tax | Employer manages | Self – 4 instalments (or 1 under 44ADA) |

| EPF | Mandatory (if applicable) | Not applicable |

| ITR form | ITR-1 or ITR-2 | ITR-3 or ITR-4 |

| Tax audit | Never required | If receipts exceed Rs. 75 lakh |

| Compliance burden | Low | Higher |

| Tax on Rs. 25L income (new regime) | Rs. 3,19,800 | Rs. 70,200 (under 44ADA) |

Which Is More Tax Efficient?

On pure income tax calculations, consultancy income under Section 44ADA is significantly more tax efficient than salary income at the same gross level. The 50% presumptive deduction reduces taxable income far more than the Rs. 75,000 standard deduction available to salaried employees.

However, the comparison is not just about income tax:

Consultants pay 18% GST if receipts exceed Rs. 20 lakh (collected from clients but adds compliance burden). Consultants handle their own advance tax. Consultants have no employer EPF contribution. Consultants carry income risk – there is no fixed monthly salary.

For many salaried professionals considering a switch to consulting, the income tax saving under Section 44ADA is attractive, but the full picture includes GST compliance, loss of EPF, health insurance costs, and irregular income. The tax advantage is real, but so is the additional responsibility.

Final Thoughts

The tax treatment of salary and consultancy income in India is genuinely different in almost every dimension. Salary is simpler – your employer handles most of the compliance. Consultancy gives you more flexibility and potentially lower income tax through Section 44ADA, but requires you to actively manage GST, advance tax, and ITR filing.

If you are currently salaried and considering consulting, understand the full tax picture before making the switch. And if you already have consultancy income, make sure you are using Section 44ADA correctly and paying advance tax on time to avoid interest penalties. You can read our complete income tax guide for a broader overview of the Indian tax system.

Frequently Asked Questions

Is consultancy income always more tax efficient than salary?

Under Section 44ADA, consultancy income is taxed on only 50% of gross receipts, which results in significantly lower income tax than the same amount received as salary. However, consultants also face GST compliance if receipts exceed Rs. 20 lakh, advance tax obligations, and no employer EPF contribution, so the full comparison goes beyond just income tax.

Can I claim Section 44ADA if I am an IT professional?

Yes. IT and software professionals are covered under Section 44ADA as technical consultancy. If your gross receipts are up to Rs. 75 lakh in FY 2025-26 and cash receipts do not exceed 5% of total receipts, you can opt for 44ADA and declare 50% of receipts as taxable income.

Do I need to register for GST as a consultant?

Yes, if your annual professional receipts exceed Rs. 20 lakh (Rs. 10 lakh in special category states). Once registered, you must collect 18% GST from clients, file GSTR-1 and GSTR-3B returns, and deposit the collected GST with the government.

What ITR form should I file if I have both salary and consultancy income?

You can file ITR-4 if you are using Section 44ADA for the consultancy portion and your total income is up to Rs. 50 lakh. ITR-3 is required only if your total income exceeds Rs. 50 lakh or you are not using presumptive taxation.

What happens if I miss advance tax payments as a consultant?

Interest is charged under Section 234B (1% per month for shortfall in advance tax) and Section 234C (1% per month for deferment of instalments). These can add up significantly if you have a large tax liability.

Can a consultant still claim Section 80C deductions?

Yes, under the old tax regime. Section 80C deductions for ELSS, PPF, LIC, and EPF contributions are available to consultants just as they are for salaried employees, provided they choose the old tax regime.

Is there a TDS on consultancy income below Rs. 30,000?

No. Section 194J TDS is deducted only if payments to a consultant exceed Rs. 30,000 per year from a single client. If multiple clients each pay you less than Rs. 30,000, no TDS is deducted, but your income is still taxable and you must pay advance tax on it.