Bonus vs Increment vs Incentive: TDS Comparison 2026

Every year around bonus season, I get the same message from readers: “My bonus was Rs. 3 lakh but I only received Rs. 2.2 lakh, why did they deduct so much?” The bonus vs increment vs incentive tds 2026 confusion comes from a genuine gap in how salary components get explained to employees. None of these three actually carry a lower tax rate or any special exemption. What differs is how and when the tax gets collected, and a few side effects that matter more than people realise.

What is Bonus, Increment, and Incentive

A bonus is typically a lump sum, paid once or twice a year, either as a statutory bonus under the Payment of Bonus Act or as a discretionary annual payout tied to company or individual performance.

An increment is a permanent upward revision to your base salary, usually effective from a fixed date like April 1st, that raises your monthly pay going forward.

An incentive is variable pay linked to targets, commonly seen in sales roles, that can be paid monthly, quarterly, or annually depending on company policy.

The Core Truth: None of These Save You Tax

This is the part most people get wrong. Unlike HRA or LTA, there is no exemption attached to bonus, increment, or incentive income. All three are fully taxable as salary, at your normal slab rate, with no ceiling and no special treatment. If your total annual taxable salary is the same, your total tax liability for the year is the same, whether that money arrived as one bonus, twelve months of higher basic pay, or four quarterly incentive payouts. The real differences lie in the timing of TDS, one specific relief provision, and the impact on your retirement savings.

How TDS Actually Differs: The Average Rate Method

Section 192 doesn’t apply a flat percentage to each payment the way some other TDS sections do. Instead, your employer estimates your total salary for the full financial year, works out the tax on that estimate using the applicable slabs, and divides it by your estimated annual income to get an “average rate.” That average rate is then applied to what you’re paid each month. This average-rate mechanism is really the engine behind the whole bonus vs increment vs incentive tds 2026 comparison, since it’s the same formula applied to very differently shaped payments.

The moment a bonus or a one-time incentive payout lands, your employer revises the annual estimate upward, recalculates the average rate, and true-up your TDS accordingly, usually in that same payout cycle. This is exactly why bonus months feel like a bigger cut than expected. It isn’t a penalty. It’s the same tax you’d owe anyway, just collected in a lump sum because it arrived as a lump sum. You can read the full mechanics of how this average rate is computed in my TDS on salary guide.

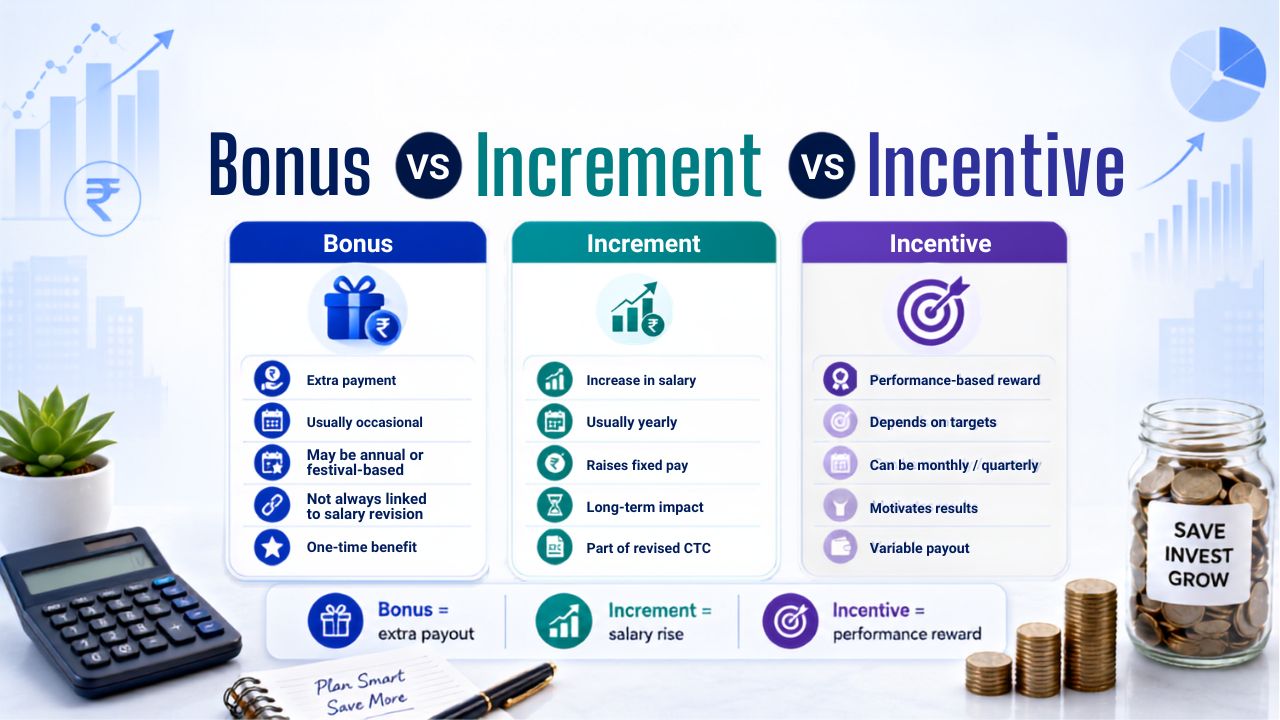

Bonus vs Increment vs Incentive TDS 2026: Side-by-Side Comparison

| Factor | Bonus | Increment | Incentive |

|---|---|---|---|

| Payment pattern | Lump sum, one or two payouts a year | Permanent monthly increase | Monthly, quarterly, or annual, target-linked |

| Tax exemption | None | None | None |

| TDS impact | Sudden spike in payout month | Spread evenly across remaining months | Spike if lump sum, smoother if recurring |

| Affects PF/Gratuity base | No | Yes, since it usually raises Basic | No |

| Section 89(1) relief possible | Only if genuinely delayed from a prior year | Yes, for backdated/arrears portion | Only if genuinely delayed from a prior year |

| Total annual tax liability | Same as any other salary of equal amount | Same as any other salary of equal amount | Same as any other salary of equal amount |

Real Example: Ramesh’s Bonus Month TDS Spike

Ramesh earns Rs. 15,00,000 a year, new regime. Before his October bonus, his employer’s running estimate for the year works out to Rs. 97,500 in tax. In October, he receives a Rs. 3,00,000 bonus, taking his estimated annual salary to Rs. 18,00,000. His employer recalculates: tax on the revised estimate comes to Rs. 1,50,800.

That’s an increase of Rs. 53,300 in tax purely because of the bonus, which usually gets recovered largely in that one payout. Effectively, close to 18% of his bonus amount goes toward this incremental tax. Ramesh isn’t being taxed unfairly. If that same Rs. 3,00,000 had arrived as a permanent increment starting in April instead, the very same Rs. 53,300 in extra tax would still be owed for the year, just spread quietly across twelve months instead of landing all at once in October.

When Increment Arrears Qualify for Section 89(1) Relief

There is one genuine exception where the government gives you real relief, and it applies specifically to arrears, most commonly from a backdated increment that spans more than one financial year, not just a lump sum within the same year.

Sunita’s company finalised a pay revision in FY 2026-27 that was backdated to cover part of FY 2025-26 as well. She received Rs. 2,40,000 as arrears this year. Without any relief, adding this to her FY 2026-27 income pushed her taxable income past the Rs. 12 lakh rebate threshold, creating an extra tax bill of Rs. 72,540 that she wouldn’t have owed otherwise. But since that Rs. 2,40,000 was genuinely due in FY 2025-26, when her income was low enough that it would have attracted zero tax even with the arrears added, she was entitled to claim the full Rs. 72,540 back under Section 89(1).

The catch is procedural: this relief is never automatic. You must file Form 10E on the income tax e-filing portal before filing your ITR, not after. If you claim the relief in your return without filing Form 10E first, it gets disallowed and you’ll receive a demand notice. You can find the official form and guidance on the Income Tax Department’s portal. A straightforward annual bonus paid on schedule usually doesn’t qualify for this relief, since it isn’t genuinely “due” from an earlier year, it’s simply this year’s regular bonus.

The Hidden Difference: PF and Gratuity Impact

This is the part almost nobody factors in when comparing the three. Provident Fund contributions are calculated only on Basic Salary plus Dearness Allowance, both from the employee and the employer, at 12% each. Bonus, incentive, and commission are explicitly excluded from this calculation under the EPF Act, a position the Supreme Court reaffirmed in 2019 for any payment tied to individual performance or output.

This means an increment that raises your Basic Salary quietly compounds your retirement savings every single year it stays in effect. A permanent Rs. 8,000 a month increment to Basic adds roughly Rs. 96,000 a year to your Basic, which pulls in an extra Rs. 11,520 a year in employer PF contribution alone, on top of the same amount from your own side. A bonus or incentive of the exact same amount adds nothing to your PF or gratuity base, however large it is. Over a ten or fifteen year career, this difference compounds into a meaningfully larger retirement corpus purely from how the same rupee got labelled on your payslip.

Which One Should You Prefer?

If you’re negotiating your next appraisal, the bonus vs increment vs incentive tds 2026 answer comes down to structure, not tax rate, since the tax owed ends up identical either way. Given a choice between a one-time bonus and an equivalent permanent increment, the increment usually wins twice over: it builds your PF and gratuity base for the rest of your tenure, and it avoids the psychologically jarring TDS spike that comes with a lump sum. Incentives make sense where they exist to reward variable performance, but treat them as bonus-equivalent for tax planning purposes rather than expecting any special treatment. Whichever mix you end up with, understanding whether the old or new regime suits your overall income shape still matters more than any of this. My old vs new tax regime guide, complete income tax guide and the current income tax slabs for FY 2026-27 are good starting points before your next salary discussion.

Frequently Asked Questions

Why does my bonus get taxed more than my regular salary?

It isn’t taxed at a higher rate. Your employer recalculates your full year’s estimated tax once the bonus is known and recovers the incremental amount in that payout, which feels larger because it arrives all at once.

Can I get tax relief on my bonus?

Generally no, unless the bonus was genuinely delayed from an earlier financial year, in which case Section 89(1) relief may apply, subject to filing Form 10E before your ITR.

Does an increment affect my PF contribution?

Yes, if it raises your Basic Salary, since PF is calculated on Basic plus DA only. Bonus and incentive amounts do not affect your PF contribution at all

Is incentive income taxed differently from salary?

No. Incentive income is fully taxable as salary at your normal slab rate, with no special exemption or reduced rate.

Do I need to do anything differently when I receive a bonus?

Not usually. The TDS is handled by your employer. Just check your Form 16 at year-end to confirm the total tax deducted matches your actual liability, and file Form 10E separately if you’re claiming Section 89(1) relief on any arrears.