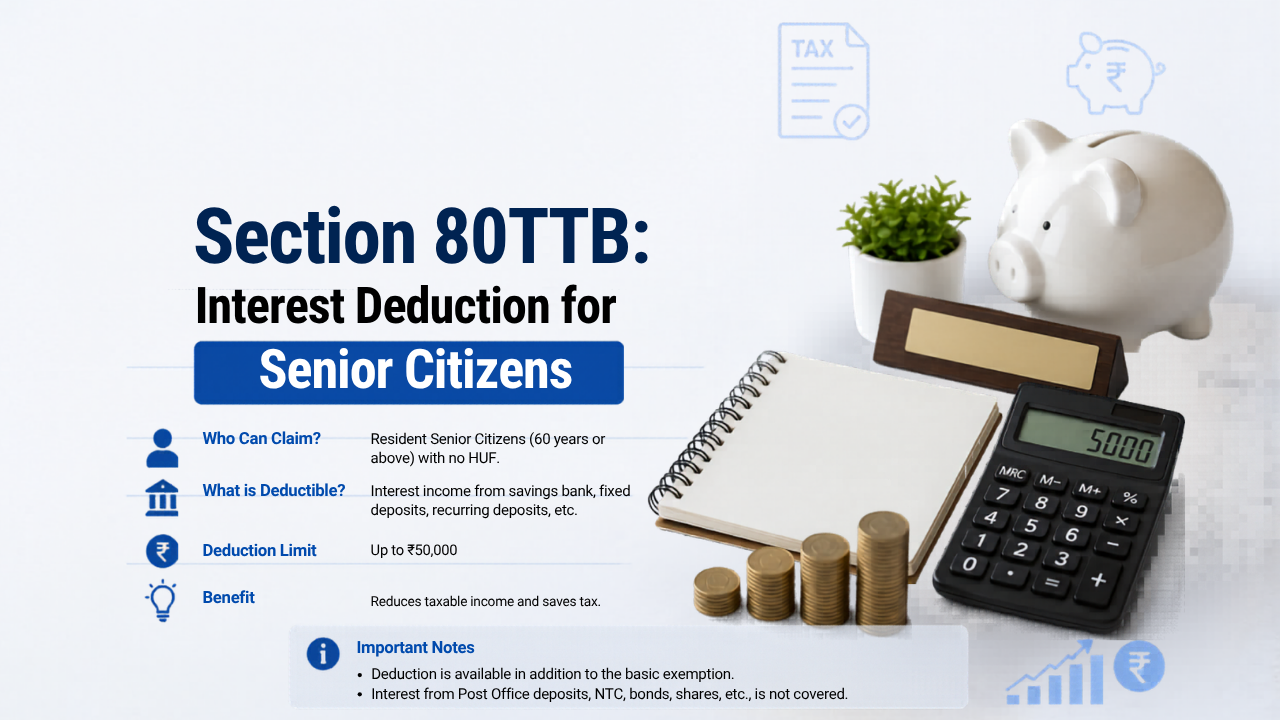

Section 80TTB: Interest Deduction for Senior Citizens

What Is Section 80TTB?

Section 80TTB of the Income Tax Act allows resident senior citizens to claim a deduction of up to Rs. 50,000 on interest income earned from deposits with banks, post offices, and co-operative banks. It was introduced in the Union Budget 2018 specifically to provide tax relief to senior citizens who depend on interest income from savings and fixed deposits after retirement.

Before Section 80TTB was introduced in Budget 2018, senior citizens could only claim Rs. 10,000 under Section 80TTA, which covered only savings account interest and excluded fixed deposits entirely. When Section 80TTB was introduced, senior citizens became ineligible for Section 80TTA. Instead, they get the much higher Rs. 50,000 limit under 80TTB, which also covers FD and RD interest, two categories that 80TTA never covered.

This deduction is available only under the old tax regime. If you have opted for the new tax regime, Section 80TTB cannot be claimed.

Who Can Claim Section 80TTB?

To claim Section 80TTB, you must satisfy all of the following conditions:

Age: You must be 60 years of age or older at any point during the financial year. This includes both senior citizens (60 to 79 years) and super senior citizens (80 years and above). If you turn 60 on any date during FY 2025-26, including April 1, 2025, you are eligible for the full year.

Resident individual: You must be a resident of India during the financial year. NRIs are not eligible for Section 80TTB, even if they are above 60 years of age.

Old tax regime: The deduction is available only under the old tax regime. Senior citizens who have opted for the new tax regime under Section 115BAC cannot claim this deduction.

Important: Section 80TTB is available only to individual senior citizens. HUFs, firms, companies, AOPs, and BOIs cannot claim it. Additionally, if the interest income comes from a deposit held in the name of a firm or AOP, the individual partners or members cannot claim 80TTB on that income.

Which Interest Income Qualifies Under Section 80TTB?

Not all interest income qualifies. The deduction covers only interest earned from the following sources:

Savings accounts with banks: Interest earned on savings accounts held with any scheduled commercial bank or co-operative bank qualifies.

Fixed deposits (FDs) with banks: Interest earned on term deposits or time deposits held with banks qualifies. This is the primary reason senior citizens benefit significantly from 80TTB compared to 80TTA, which excluded FD interest.

Recurring deposits (RDs) with banks: Interest earned on recurring deposits held with banks also qualifies.

Post office deposits: Interest from post office savings accounts and post office time deposits (FDs) qualifies. Note that interest from Post Office Monthly Income Scheme (MIS) and Post Office Recurring Deposits does not qualify under Section 80TTB. Senior Citizens Savings Scheme (SCSS) interest qualifies as it is a time deposit with the post office.

Co-operative bank deposits: Interest from deposits held with co-operative societies engaged in the business of banking, including co-operative land mortgage banks and co-operative land development banks, qualifies.

What Does Not Qualify?

Company fixed deposits: FDs held with NBFCs or companies such as Bajaj Finance FD, Mahindra Finance FD, or similar do not qualify. Only bank and post office deposits are covered.

Bonds and debentures: Interest from government bonds, corporate bonds, or non-convertible debentures (NCDs) does not qualify.

RBI bonds: Interest from RBI Floating Rate Savings Bonds does not qualify under Section 80TTB.

Loans given to others: Interest received on personal loans given to friends or family members does not qualify.

Deduction Limit Under Section 80TTB

The deduction allowed is the lower of Rs. 50,000 or the actual interest income earned from eligible sources during the financial year.

If your total interest income from all eligible sources (savings accounts, FDs, RDs, post office deposits) is Rs. 38,000, your deduction is Rs. 38,000. If your total interest income is Rs. 90,000, your deduction is capped at Rs. 50,000.

This Rs. 50,000 limit applies to the combined interest income from all eligible sources combined across all banks and post offices. It is not Rs. 50,000 per bank.

Note: The TDS threshold under Section 194A is separate from the deduction limit. Banks are not required to deduct TDS on interest paid to a senior citizen if the total interest from that bank does not exceed Rs. 1,00,000 in a financial year (increased from Rs. 50,000 in Budget 2025). This TDS threshold is per bank. However, the Section 80TTB deduction limit remains Rs. 50,000 in total across all banks and post offices combined.

How to Calculate the Section 80TTB Deduction

The calculation is straightforward. Add up all interest income from eligible sources, then claim whichever is lower: the total interest income or Rs. 50,000.

Worked Example

Rajesh is a 67-year-old retired government employee in Bengaluru. He has the following interest income for FY 2025-26:

Savings account interest (SBI): Rs. 8,000

Fixed deposit interest (SBI): Rs. 55,000

SCSS interest (Post Office): Rs. 32,000

Total eligible interest income: Rs. 95,000

Section 80TTB deduction = Lower of Rs. 95,000 or Rs. 50,000 = Rs. 50,000

Rajesh claims Rs. 50,000 as a deduction under Section 80TTB, reducing his taxable income by that amount. The remaining Rs. 45,000 of interest income is taxable at his applicable slab rate. For the complete income tax framework for senior citizens and others, see our complete income tax guide.

Example Where Full Amount Is Deductible

Meena is a 63-year-old resident of Delhi. She has the following interest income for FY 2025-26:

Savings account interest: Rs. 12,000

Recurring deposit interest: Rs. 18,000

Total eligible interest income: Rs. 30,000

Section 80TTB deduction = Lower of Rs. 30,000 or Rs. 50,000 = Rs. 30,000

Meena claims her full interest income of Rs. 30,000 as a deduction. She pays zero tax on this interest income.

How to Claim Section 80TTB in Your ITR

Section 80TTB does not require a separate form like Form 10BA for Section 80GG. You claim it directly in your ITR. Here is how:

Step 1: Report all interest income (from savings accounts, FDs, RDs, post office deposits) under the head Income from Other Sources in your ITR. Do not skip this step. Many senior citizens mistakenly leave out interest income thinking it is exempt. It must be declared first, then the deduction is claimed against it.

Step 2: In the deductions section under Chapter VI-A, enter the eligible interest income (up to Rs. 50,000) under Section 80TTB.

Step 3: The deduction reduces your gross total income, lowering your tax liability.

Log in to incometax.gov.in to file your ITR and claim this deduction. For the due date to file ITR for FY 2025-26, see our guide on the ITR filing last date for AY 2026-27.

Section 80TTB vs Section 80TTA

| Feature | Section 80TTA | Section 80TTB |

|---|---|---|

| Who can claim | Individuals below 60 and HUFs | Resident senior citizens (60+) |

| Maximum deduction | Rs. 10,000 | Rs. 50,000 |

| Savings account interest | Covered | Covered |

| FD interest | Not covered | Covered |

| RD interest | Not covered | Covered |

| Post office deposits | Covered (savings only) | Covered (all deposits) |

| Tax regime | Old regime only | Old regime only |

| Can both be claimed together? | No. A senior citizen can only claim 80TTB, not 80TTA. | |

Once a taxpayer qualifies as a senior citizen (60+), they move entirely to Section 80TTB. They cannot claim Section 80TTA for savings account interest and Section 80TTB for FD interest simultaneously. Only 80TTB applies, but with the higher Rs. 50,000 limit covering all eligible deposit interest together.

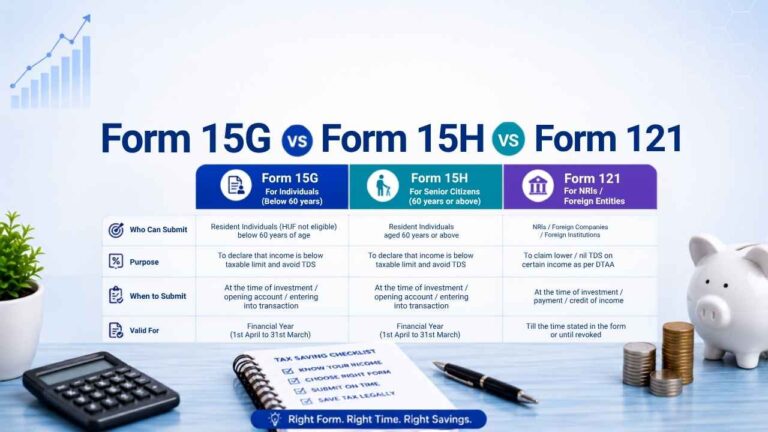

How to Avoid TDS on Interest Using Form 15H

Banks and post offices deduct TDS on interest income if it crosses the threshold limit. For senior citizens, the TDS threshold under Section 194A was increased in Budget 2025 to Rs. 1,00,000 per bank per financial year. This means a bank will not deduct TDS if the total interest credited to a senior citizen from that bank does not exceed Rs. 1,00,000 in the year.

However, if your total income (from all sources including interest) is below the taxable limit, you can submit Form 15H to your bank at the beginning of the financial year to request that no TDS be deducted. Form 15H is a self-declaration form specific to senior citizens (Form 15G is for those below 60).

Key points about Form 15H:

Submit at the start of the year: Submit Form 15H to your bank at the beginning of April each year, before any interest is credited. If submitted mid-year, TDS already deducted for earlier months will not be reversed.

Submit to each bank separately: If you have accounts at multiple banks, submit Form 15H to each bank individually.

Eligibility: You can submit Form 15H only if your estimated total income for the year is below the taxable limit, meaning your total tax liability for the year is nil.

Even if TDS has been deducted, you can claim it as a tax credit when filing your ITR, and if your total tax liability is lower than the TDS deducted, you will receive a refund. Always reconcile TDS entries with your Form 26AS before filing your ITR.

Frequently Asked Questions

Does Section 80TTB apply to super senior citizens (80 years and above)?

Yes. The section applies to all resident individuals aged 60 and above, which includes both senior citizens (60 to 79 years) and super senior citizens (80 years and above). The deduction limit is Rs. 50,000 for both categories.

Can I claim Section 80TTB on interest from my SCSS account?

Yes. Interest earned on the Senior Citizens Savings Scheme (SCSS) held at a post office qualifies as post office deposit interest and is eligible under Section 80TTB.

I have FDs with both SBI and HDFC Bank. Is the Rs. 50,000 limit per bank or combined?

The Rs. 50,000 limit is the combined limit for all eligible interest income across all banks and post offices. If you earn Rs. 35,000 from SBI and Rs. 25,000 from HDFC Bank, your total eligible interest is Rs. 60,000, but the deduction is capped at Rs. 50,000.

Can I claim both Section 80TTB and Section 80C in the same year?

Yes. Section 80TTB and Section 80C are separate deductions and can both be claimed in the same year under the old tax regime. Section 80TTB covers interest income deduction (up to Rs. 50,000) while Section 80C covers investments like PPF, tax-saving FDs, and life insurance premiums (up to Rs. 1,50,000). For a complete list of investments covered under 80C, see our guide on Section 80C deductions.

My interest income is Rs. 1,20,000. How much is taxable after 80TTB?

After claiming Section 80TTB, Rs. 50,000 is deducted. The remaining Rs. 70,000 is added to your gross total income and taxed at your applicable slab rate under the old tax regime.

Is interest from a company FD eligible under Section 80TTB?

No. Company fixed deposits (with NBFCs or corporates) are not eligible. Section 80TTB covers only deposits with banks, co-operative banks, and post offices. Interest from company FDs is fully taxable with no deduction available.

Can an NRI senior citizen claim Section 80TTB?

No. Section 80TTB is available only to resident senior citizens. NRIs, even if they are above 60 years of age, are not eligible for this deduction.

If you are a senior citizen filing your ITR for FY 2025-26, check the ITR filing last date for AY 2026-27 to plan your filing on time. And if you are also investing in tax-saving instruments, review the full list of deductions available under Section 80C to maximise your savings under the old tax regime.