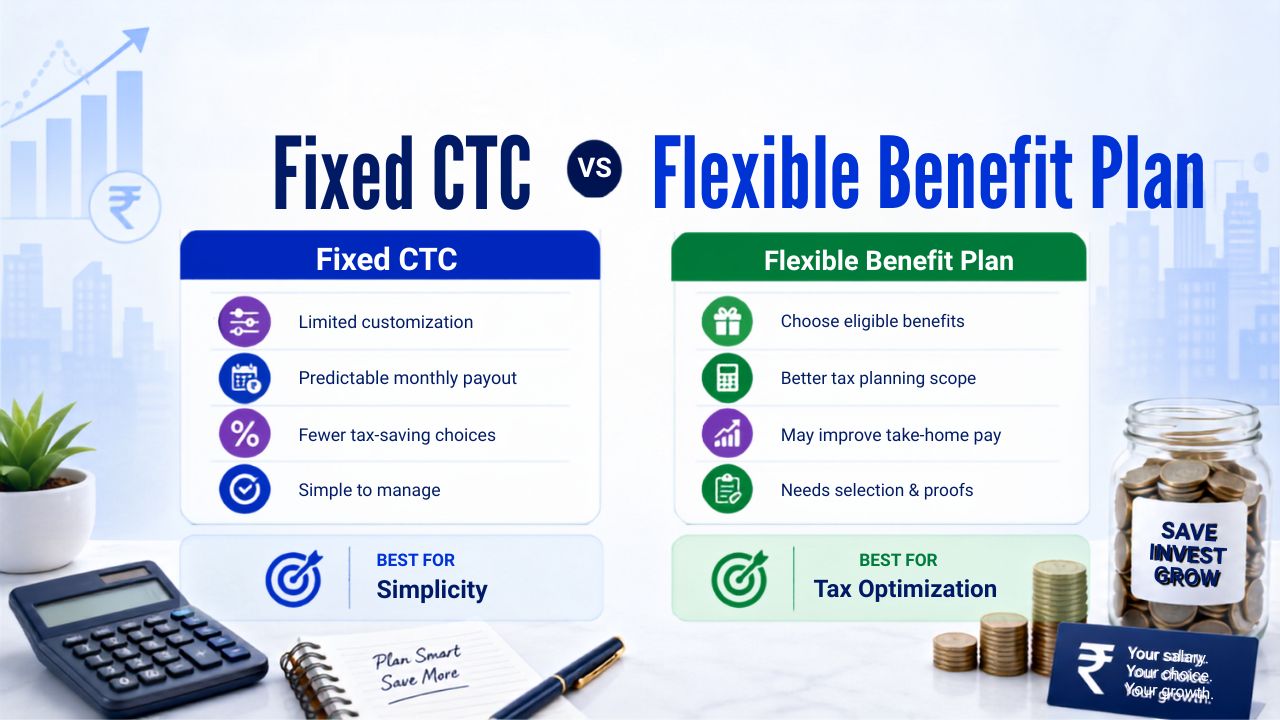

Fixed CTC vs Flexible Benefit Plan: Tax Optimization Comparison 2026

Almost every offer letter I review for friends and readers has some version of this line: “Special Allowance” sitting as one large, fully taxable number. When I ask whether their CTC includes a Flexible Benefit Plan, most people aren’t sure. The fixed ctc vs flexible benefit plan tax 2026 question comes up constantly during appraisal season, and once you see how the two structures actually behave, the choice becomes obvious. Let me walk you through both.

What is Fixed CTC

A Fixed CTC structure pays out most of your compensation as predetermined components, typically Basic Salary, HRA, and a large chunk labelled Special Allowance or Fixed Allowance. Basic and HRA are set by policy, and the Special Allowance is simply cash, paid out monthly, fully added to your taxable salary. There is nothing to declare, nothing to submit, and nothing to optimise. It is the simplest structure to administer, and also the least tax-efficient one, because a large slice of your CTC never gets the chance to become exempt.

What is a Flexible Benefit Plan

A Flexible Benefit Plan, commonly called FBP or a flexi-basket, takes that same Special Allowance pool and lets you redirect part of it into specific, tax-recognised heads instead of receiving it as plain cash. Depending on your employer’s policy, this basket can include LTA, meal vouchers, telephone and internet reimbursement, fuel and driver reimbursement, and employer NPS contribution, among others. This is really the heart of the fixed ctc vs flexible benefit plan tax 2026 decision: the CTC number on your offer letter doesn’t change, only how efficiently that number gets taxed. You declare your allocation at the start of the year, spend against it, and submit bills. Whatever you do not use with proper documentation gets paid out as taxable salary anyway, which is the one condition that makes FBP a discipline rather than a free lunch.

Which FBP Components Actually Save Tax

Not every FBP head behaves the same way, and this is where most salary structuring advice gets vague. Here is what each component actually does, and under which regime:

| Component | Basis | Regime Availability |

|---|---|---|

| HRA | Lowest of HRA received, 50%/40% of basic, rent minus 10% of basic | Old regime only |

| LTA | Lowest of employer LTA and actual eligible travel fare, twice per 4-year block | Old regime only |

| Meal vouchers | Up to Rs. 200 per meal, roughly Rs. 1,05,600 a year, from FY 2026-27 | Both regimes from FY 2026-27 |

| Telephone/internet reimbursement | Full bill amount, no prescribed ceiling, against actual bills for official use | Both regimes |

| Employer NPS contribution (Section 80CCD(2)) | 10% of basic and DA for private sector under old regime, 14% for private sector under new regime, 14% for government employees under either regime | Both regimes |

| Fuel and driver reimbursement | Nil if wholly for official use with logbook, flat perquisite value if mixed use | Largely regime-neutral, confirm with payroll |

The meal voucher change is worth pausing on. Until FY 2025-26, the exemption was capped at Rs. 50 per meal, working out to Rs. 26,400 a year, and it wasn’t even available under the new regime. From FY 2026-27, the cap has been raised to Rs. 200 per meal, taking the annual exemption to roughly Rs. 1,05,600, and it now applies under both the old and new tax regimes. This alone changes how useful FBP is for new-regime employees, which I’ll come back to shortly.

Fixed CTC vs Flexible Benefit Plan Tax Comparison 2026

| Factor | Fixed CTC | Flexible Benefit Plan |

|---|---|---|

| How Special Allowance is paid | Fully as cash, fully taxable | Split across exempt or partially exempt heads, plus a residual taxable balance |

| Effort required | None | Annual declaration, ongoing bill submission |

| Portability | N/A | Resets with every employer, does not carry over on job change |

| Risk | None | Unused or undocumented allocation becomes taxable at year-end |

| Best suited for | Employees who cannot produce bills or prefer simplicity | Employees with genuine rent, travel, phone, and fuel expenses |

| Tax outcome | Higher taxable salary for the same CTC | Lower taxable salary for the same CTC, when used correctly |

Real Example: Neha’s Fixed CTC vs FBP Tax Saving

Neha works in Bengaluru on an 18 lakh CTC in the old regime. Her Basic and HRA are fixed either way. What differs is how her remaining Rs. 6,00,000 flexible pool gets paid out.

Structure A, Fixed CTC: The entire Rs. 6,00,000 comes as Special Allowance, fully taxable. At the 30% slab, that costs her Rs. 1,80,000 in tax.

Structure B, FBP-optimized: Neha allocates the same pool as follows:

- LTA: Rs. 50,000 employer component, she travels by AC first class train with her family, actual fare Rs. 46,000. Exempt: Rs. 46,000. Taxable: Rs. 4,000.

- Meal vouchers: Rs. 1,05,600, fully exempt under the FY 2026-27 rule.

- Telephone and internet reimbursement: Rs. 36,000, fully exempt against her actual bills.

- Residual Special Allowance: Rs. 4,08,400, fully taxable.

Her total exempt amount comes to Rs. 1,87,600, leaving Rs. 4,12,400 taxable. At the 30% slab, that’s Rs. 1,23,720 in tax.

Neha saves Rs. 56,280 a year, on the exact same CTC, purely by routing the same money through FBP instead of taking it as flat cash. No pay cut, no extra investment, just better structuring.

Does FBP Still Help Under the New Tax Regime?

This is where most people assume the fixed ctc vs flexible benefit plan tax 2026 comparison collapses into “doesn’t matter,” and until recently they’d have been right. But with meal vouchers and telephone reimbursement now regime-neutral, FBP still has something to offer even under the new regime.

Take Rohan, on a 12 lakh CTC, new regime. He cannot touch HRA or LTA. But he can still structure Rs. 1,05,600 into meal vouchers and Rs. 30,000 into telephone reimbursement, both fully exempt regardless of regime. That’s Rs. 1,35,600 kept out of his taxable salary, saving him roughly Rs. 27,120 at a 20% marginal slab, money that would otherwise have sat inside a taxable Special Allowance doing nothing for him.

If Rohan’s employer also contributes to his NPS account, the new regime actually works in his favour here: private-sector employer NPS contributions are deductible up to 14% of basic and DA under the new regime, compared to only 10% under the old regime for private-sector employees. That’s a rare case where the new regime is the more generous side of the comparison.

Common FBP Mistakes That Cost You the Tax Benefit

The exemption only holds if the paperwork holds. A few patterns I see repeatedly:

- Allocating to heads you can’t use. A fuel reimbursement allocation with no car, or a driver reimbursement with no driver, just becomes taxable salary at year-end with extra effort for nothing.

- Missing the submission window. Most employers set a January or February deadline for annual proofs. Miss it, and the exemption is lost even if you genuinely spent the money.

- Taking a fixed monthly payout instead of a reimbursement. If telephone allowance is paid every month regardless of bills, it becomes a taxable allowance, not an exempt reimbursement. The distinction is entirely about documentation.

- Ignoring the old vs new tax regime decision first. If your total exemptions and deductions don’t clear the new regime’s lower slab advantage, all the FBP optimisation in the world won’t make the old regime win. Run that comparison before you build your FBP allocation.

Which Should You Choose

Between the two, the fixed ctc vs flexible benefit plan tax 2026 answer is straightforward: FBP is never worse than Fixed CTC, and is usually meaningfully better, provided you can actually produce the bills. If you pay rent, travel occasionally, and use your phone for work, an FBP-enabled structure will almost always beat an equivalent Fixed CTC. The only real case for staying with Fixed CTC is if you know you won’t have the documentation discipline to claim the components, in which case the paperwork becomes wasted effort rather than wasted money. For a broader look at how these pieces fit into your salary slip, my guides on HRA exemption calculation and the full list of Section 10 exemptions go deeper into each individual component. And since FBP allocation directly changes how much TDS on salary your employer deducts each month, it’s worth getting this right at the start of the year rather than fixing it in March.

Frequently Asked Questions

Is Flexible Benefit Plan always better than Fixed CTC?

Almost always, as long as you can genuinely produce bills for the components you allocate. If you cannot, the unused allocation simply becomes taxable salary, so there’s no downside beyond the extra paperwork.

Can I use FBP under the new tax regime?

Yes, though with fewer components. Meal vouchers and telephone/internet reimbursement are available under both regimes, and employer NPS contribution under Section 80CCD(2) is actually more generous under the new regime for private-sector employees.

What happens if I don’t submit bills for my FBP allocation?

The unclaimed amount is added back to your taxable salary, usually in your final payroll cycle of the year, and taxed at your normal slab rate.

Does changing from Fixed CTC to FBP change my total CTC?

No. Your total CTC stays the same. Only how much of it is taxable changes, based on how efficiently the components are used.

Can I change my FBP allocation mid-year?

This depends entirely on your employer’s policy. Most companies open the declaration window once a year, though some allow limited revisions. Check your HR portal for your specific policy, and refer to the official provisions on the Income Tax Department’s website for the underlying rules.