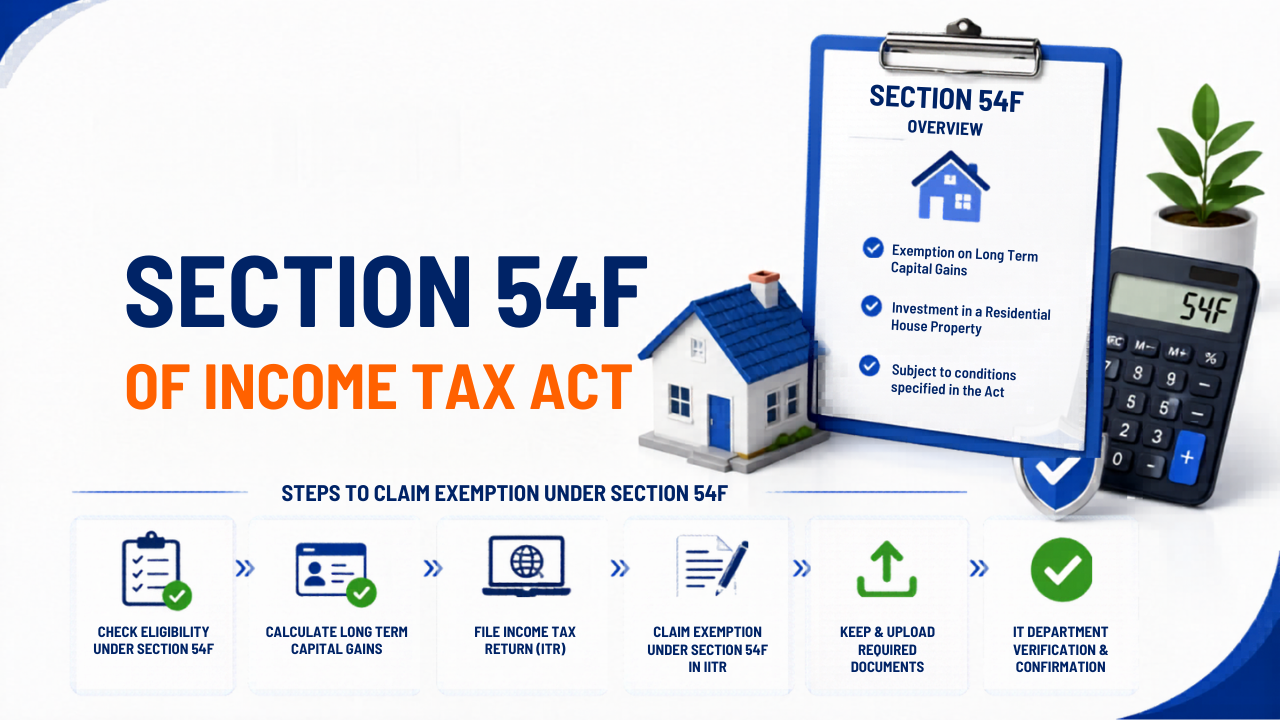

Section 54F: Capital Gain Exemption on Property

If you sold shares, gold, land, or any asset other than a house property and made a long-term capital gain, Section 54F of the Income Tax Act gives you a legal way to avoid paying tax on that gain, provided you reinvest the sale proceeds into a residential house.

This exemption is one of the most useful and least understood provisions in Indian income tax law. Many salaried professionals who sell equity, mutual funds, or inherited land miss out on this benefit simply because they are not aware of it.

This article breaks down Section 54F completely, with conditions, calculation method, practical examples, and the key mistakes to avoid.

What is Section 54F?

Section 54F provides exemption from Long-Term Capital Gains (LTCG) tax when you sell a long-term capital asset other than a residential house property and use the net sale consideration to purchase or construct a new residential house in India.

Note the key difference from Section 54: Section 54 applies when you sell a house and buy another house. Section 54F applies when you sell anything else (shares, gold, jewellery, land, commercial property, mutual funds, bonds) and buy a residential house.

Under the new Income Tax Act 2025, this provision continues under the same framework. For ITR filing in July 2026 (FY 2025-26), use the Act 1961 provisions via Tab 1 on the income tax portal. For a full overview of income tax rules applicable this year, refer to our complete income tax guide India.

Which Assets Qualify Under Section 54F?

Section 54F applies to any long-term capital asset that is not a residential house property. This includes:

- Listed equity shares held for more than 12 months

- Equity mutual funds held for more than 12 months

- Gold, jewellery, and precious metals held for more than 36 months

- Land (non-agricultural) held for more than 24 months

- Commercial property held for more than 24 months

- Debt mutual funds held for more than 24 months (though taxed at slab rate now)

- Unlisted shares held for more than 24 months

- Bonds and debentures held for more than 36 months

The holding period determines whether the gain is long-term. If the gain is short-term, Section 54F does not apply.

Conditions to Claim Section 54F Exemption

All of the following conditions must be satisfied to claim this exemption:

Condition 1: The asset sold must be a long-term capital asset, not a residential house

If you sell a residential house, Section 54F does not apply. You would look at Section 54 instead.

Condition 2: You must purchase or construct one residential house in India

- Purchase: Within 1 year before or 2 years after the date of transfer

- Construction: Within 3 years from the date of transfer

The property must be in India. Buying a house abroad does not qualify.

Condition 3: You must not own more than one residential house on the date of transfer

This is a critical condition. On the date you sell the original asset, you should not own more than one residential house (other than the new one being purchased). If you already own two houses, you cannot claim Section 54F.

Condition 4: You must not purchase another residential house within 1 year or construct within 3 years

After claiming the exemption, if you buy an additional house (other than the new one) within 1 year, or construct one within 3 years, the exemption is withdrawn.

Condition 5: The new house must not be sold within 3 years

If you sell the newly purchased or constructed house within 3 years of acquisition, the exemption claimed will be revoked, and the capital gain will become taxable in the year of sale.

How is Section 54F Exemption Calculated?

Unlike Section 54 (where the entire LTCG is exempt if you reinvest the gain amount), Section 54F requires you to reinvest the entire net sale consideration, not just the capital gain.

The exemption is calculated proportionally:

Exemption = (Capital Gain x Amount Invested in New House) / Net Sale Consideration

If you invest the full net sale consideration in the new house, the entire capital gain is exempt. If you invest only a part, only a proportionate exemption is allowed.

Section 54F Calculation: Practical Example

Scenario: Rohan, a salaried professional in Bengaluru, sells listed equity shares in December 2025.

- Sale price of shares: Rs. 50,00,000

- Cost of acquisition (indexed or actual): Rs. 20,00,000

- Long-Term Capital Gain: Rs. 30,00,000

- Net Sale Consideration: Rs. 50,00,000

Rohan uses Rs. 45,00,000 of the sale proceeds to purchase a residential flat in January 2026.

Exemption Calculation:

Exemption = (30,00,000 x 45,00,000) / 50,00,000 Exemption = Rs. 27,00,000

Taxable LTCG = 30,00,000 – 27,00,000 = Rs. 3,00,000

Since Rohan did not invest the full Rs. 50,00,000, only a proportionate exemption of Rs. 27,00,000 is available. The remaining Rs. 3,00,000 is taxable at 12.5% (equity LTCG rate above Rs. 1.25 lakh threshold).

Had Rohan invested the full Rs. 50,00,000, the entire Rs. 30,00,000 gain would have been exempt.

What Happens to Uninvested Sale Proceeds? Capital Gains Account Scheme

If you have made the capital gain but have not yet purchased or constructed the house before the ITR filing deadline (July 31, 2026), you must deposit the uninvested amount in a Capital Gains Account Scheme (CGAS) with a scheduled bank before filing your ITR.

This preserves your exemption claim. You can then withdraw from CGAS to purchase or construct the house within the stipulated time.

If the amount deposited in CGAS is not used within the required time period, it becomes taxable in the year the period expires.

Important: Simply keeping the money in a regular savings account does not protect your exemption. It must be deposited in a CGAS account specifically.

Section 54F vs Section 54: Key Differences

| Parameter | Section 54 | Section 54F |

|---|---|---|

| Asset Sold | Residential house property | Any LTCA except residential house |

| Reinvestment Required | Capital Gain amount | Full Net Sale Consideration |

| Exemption | Full gain if reinvested | Proportionate |

| Max Houses Owned | No restriction | Maximum 1 house on transfer date |

| Time to Purchase | 1 year before / 2 years after | 1 year before / 2 years after |

| Time to Construct | 3 years | 3 years |

| Lock-in on New House | 3 years | 3 years |

Rs. 10 Crore Cap on Section 54F Exemption

From FY 2023-24 onwards, a cap of Rs. 10 crore applies on the cost of the new residential house for computing the exemption under Section 54F. Even if you invest more than Rs. 10 crore in the new house, only Rs. 10 crore will be considered for the exemption calculation.

This cap was introduced to prevent ultra-high-net-worth individuals from parking unlimited gains into luxury properties to avoid tax. For most salaried professionals, this cap is not a practical concern.

Common Mistakes to Avoid

Mistake 1: Confusing net sale consideration with capital gain

Section 54F requires reinvestment of the full net sale consideration (the actual amount you received), not just the profit. Many taxpayers reinvest only the gain amount, resulting in only a proportionate exemption instead of full relief.

Mistake 2: Already owning two houses

If you own two residential houses on the date of sale, you are not eligible for Section 54F at all. Check your property ownership before planning to claim this exemption.

Mistake 3: Not using CGAS before ITR filing

If your new house purchase is pending and ITR due date is approaching, deposit the balance in a Capital Gains Account Scheme. Missing this step forfeits the exemption.

Mistake 4: Selling the new house within 3 years

The new house has a mandatory 3-year lock-in. Selling before that reverses the exemption and adds the capital gain to your income in the year of sale.

Mistake 5: Buying the new property in a joint name carelessly

If you buy the new house jointly but the original asset was sold solely in your name, ensure the purchase structure does not create complications in claiming the exemption. Consult a CA if the ownership structure is complex.

Section 54F and ITR Filing

If you are claiming Section 54F exemption, you need to report the capital gain and the exemption in your ITR. You cannot file ITR-1 (Sahaj) if you have capital gains. You will need to file ITR-2 (if you are a salaried individual with capital gains) or ITR-3 (if you have business income as well).

Refer to our guide on which ITR form to file for FY 2025-26 to confirm the right form for your situation.

The capital gains schedule in ITR-2 has a specific section where you enter the exemption claimed under Section 54F along with details of the new property purchased.

How Section 54F Fits Into Your Overall Tax Planning

Section 54F works best when combined with your broader capital gains planning. If you are selling shares or equity mutual funds with significant LTCG, the Rs. 1.25 lakh annual LTCG exemption under Section 112A will apply first. Beyond that, Section 54F can shelter the remaining gains if you are planning to buy a house.

For example, if you have Rs. 30 lakh LTCG from equity and plan to buy a house worth Rs. 80 lakh anyway, Section 54F can make that house purchase essentially tax-free on the capital gains side.

This kind of planning is exactly what separates a reactive taxpayer from a proactive one. Understanding capital gains tax rules for FY 2025-26 in full helps you see all the levers available to you.

You can also read more about all available tax saving strategies for salaried employees to plan your investments alongside capital gains exemptions.

Frequently Asked Questions

Can I claim Section 54F on STCG (Short-Term Capital Gains)? No. Section 54F applies only to long-term capital gains. Short-term gains do not qualify.

Can I buy two houses and claim Section 54F? No. Section 54F allows exemption for only one residential house. If you purchase two houses, the exemption is restricted to one. Also, you must not own more than one house on the date of the original asset transfer.

Can a salaried person claim Section 54F on sale of equity shares? Yes, absolutely. If you held the shares for more than 12 months, the gain is long-term, and Section 54F applies if you reinvest the sale consideration in a residential house.

What if I invest in an under-construction property? Under-construction property qualifies, provided it is completed and possession is taken within 3 years from the date of transfer of the original asset.

Is Section 54F available under the new tax regime? Yes. Capital gains exemptions under Section 54F are available regardless of whether you opt for the old or new tax regime. The regime choice affects your salary income deductions, not capital gains exemptions.

What is the difference between Section 54 and Section 54F in simple terms? Section 54 is for people who sell a house and buy another house. Section 54F is for people who sell anything else (shares, gold, land) and buy a house. In Section 54F, you must reinvest the full sale amount, not just the profit.