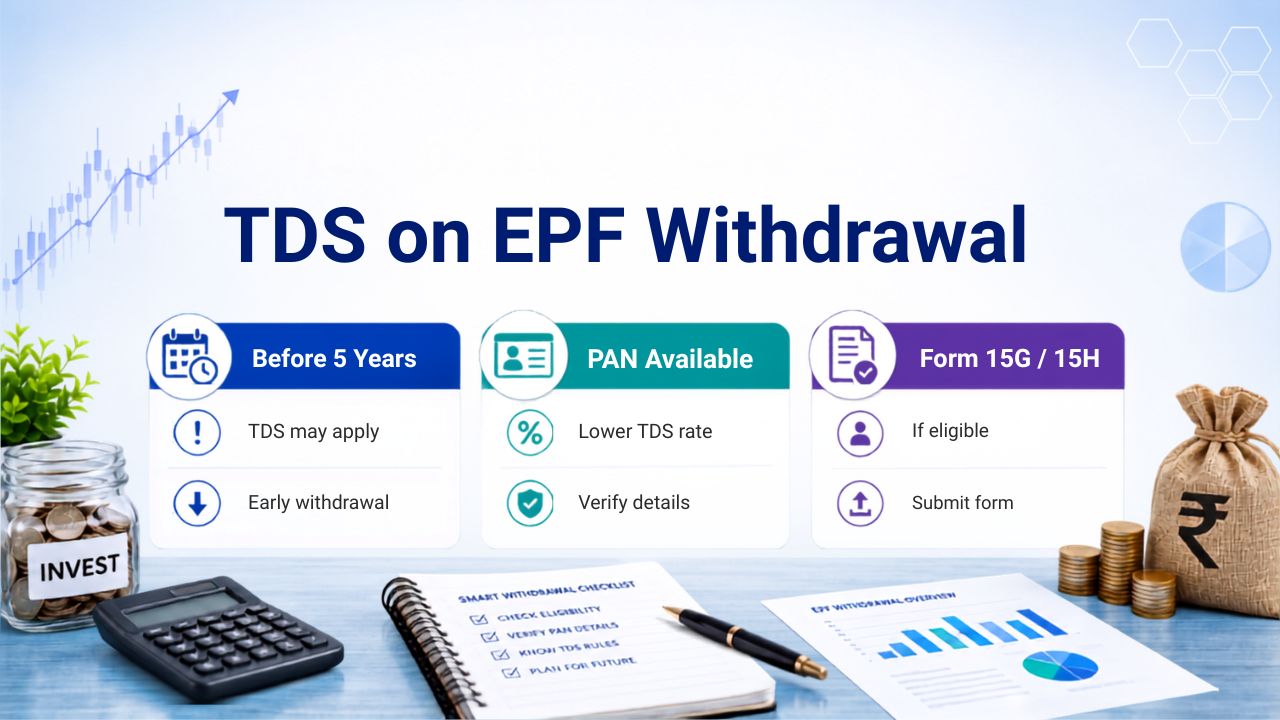

TDS on EPF Withdrawal: Before vs After 5 Years Comparison

TDS on EPF withdrawal before vs after 5 years is one of the most commonly misunderstood tax rules among salaried professionals. Many people assume their EPF balance is completely tax-free no matter when they withdraw it. That assumption can lead to a surprise TDS deduction at the time of withdrawal and unnecessary tax liability when filing ITR.

Table of Contents

The actual rule depends entirely on one factor: how many years of continuous service you have completed before withdrawing. Get this right and you either pay zero tax or know exactly what to expect.

Here is a complete breakdown of how TDS on EPF withdrawal works in 2026. If you want a broader overview of Indian income tax first, our complete income tax guide covers all the fundamentals.

What Is Section 192A and When Does It Apply?

Section 192A of the Income Tax Act governs TDS on EPF withdrawals. It applies specifically when a member withdraws their EPF balance before completing 5 years of continuous service.

Under this section, EPFO (Employees Provident Fund Organisation) deducts TDS directly from your withdrawal amount before crediting the balance to your account. The TDS is then reflected in your Form 168 (the updated Form 26AS under the new Income Tax Act 2025).

Two key numbers under Section 192A:

TDS threshold: Rs. 50,000. If your total EPF withdrawal is below Rs. 50,000, no TDS is deducted regardless of your years of service.

TDS rate: 10% if your PAN is linked with your UAN. 20% if PAN is not linked or not available.

TDS on EPF Withdrawal Before 5 Years

If you withdraw your EPF balance before completing 5 years of continuous service and the amount exceeds Rs. 50,000, TDS at 10% is deducted on the entire withdrawal amount.

But TDS is just the starting point. The more important question is: how much of your EPF withdrawal is actually taxable and under which head?

What Gets Taxed and What Does Not

Not every rupee of your EPF balance is taxed the same way when you withdraw before 5 years.

Employer’s contribution and interest on it: Fully taxable as salary income. Your employer’s EPF share was never taxed when deposited, so the entire amount including interest earned on it becomes taxable when you withdraw. Note that this refers to your employer’s EPF contribution specifically (3.67% of basic salary). The employer’s 8.33% contribution goes to EPS (Employee Pension Scheme), which is a separate account with different withdrawal rules and is not covered under Section 192A.

Employee’s own contribution: Not taxable as income. Your own contribution comes from your salary, which was already included in your taxable income. However, if you claimed a Section 80C deduction (Section 123 under the new Act 2025) on this contribution in previous years, that deduction will be reversed on premature withdrawal and added back to your taxable income as salary.

Interest on employee’s contribution: Taxable as income from other sources. Even though the principal is not taxable, the interest it earned inside EPF is taxable on premature withdrawal.

Example: EPF Withdrawal Before 5 Years

You withdraw Rs. 4,80,000 from your EPF account after 3 years of service. This example covers the EPF account balance only and excludes the EPS portion.

Your EPF balance consists of:

- Employer EPF contribution: Rs. 2,00,000

- Interest on employer contribution: Rs. 40,000

- Employee contribution: Rs. 2,00,000

- Interest on employee contribution: Rs. 40,000

TDS deducted by EPFO: 10% of Rs. 4,80,000 = Rs. 48,000

Actual taxable amount:

- Employer contribution + interest: Rs. 2,40,000 (taxable as salary)

- Interest on employee contribution: Rs. 40,000 (taxable as income from other sources)

- Employee contribution principal: Rs. 2,00,000 (not taxable, unless 80C was claimed)

Total taxable: Rs. 2,80,000 (plus any 80C reversal amount if applicable)

When filing your ITR, you declare Rs. 2,80,000 as income and claim credit for Rs. 48,000 TDS already deducted. If your total income including this amount falls in a lower tax bracket, you may get a refund of some or all of the TDS. You can track your refund using the ITR refund status check process.

TDS on EPF Withdrawal After 5 Years

After 5 years of continuous service, EPF withdrawal is completely exempt from tax under Section 10(12) of the Income Tax Act. You can read more about what falls under Section 10 in our Section 10 exemptions guide.

No TDS is deducted. No income tax is payable. While you do not need to declare this as taxable income, it is advisable to report it under Schedule EI (Exempt Income) in your ITR for completeness.

This exemption applies to the entire EPF withdrawal amount, including employer contribution, employee contribution, and all interest earned over the years.

This is why most financial advisors recommend not withdrawing EPF before 5 years unless absolutely necessary. The tax cost of an early withdrawal can be significant, especially if the amount is large and you are in a higher tax bracket.

What Counts as 5 Years of Continuous Service?

This is where many people make a mistake. The 5-year rule is about continuous service, not 5 years with the same employer.

If you changed jobs:

If you transferred your PF balance from your previous employer’s account to your new employer’s account via UAN, your service period from the previous employer also counts. The total years of service across both employers is considered continuous for this rule.

If you withdrew PF from a previous job:

If you withdrew your EPF balance when you left your previous employer instead of transferring it, the continuity breaks. Your service count restarts from the date you joined the new employer.

If your employer’s business shut down:

If your employer discontinued business or you were terminated for reasons beyond your control, the 5-year rule does not apply even if you have not completed 5 years. TDS is not deducted in such cases. Retirement on reaching the age of superannuation also falls under this exception.

If you left due to ill health:

If the withdrawal is due to the member’s own ill health, TDS is not deducted even before 5 years.

When TDS Is Not Deducted Even Before 5 Years

Section 192A provides specific exceptions where TDS is not applicable even if you withdraw before completing 5 years:

The withdrawal amount is less than Rs. 50,000. The member is terminated due to ill health. The employer discontinued business. The withdrawal is caused by reasons beyond the employee’s control, including retirement at superannuation age. The EPF balance is being transferred to another employer’s account rather than withdrawn.

In all these cases, you receive your full EPF amount without any TDS deduction. However, taxability rules may still apply depending on the reason for withdrawal. If in doubt, consult a tax professional before filing your ITR.

How to Avoid TDS on EPF Withdrawal: Form 15G and 15H

If you are withdrawing before 5 years but your total income for the year is below the taxable limit, you can submit Form 15G to EPFO before processing your withdrawal claim. This instructs EPFO not to deduct TDS.

Under the new Income Tax Act 2025, Form 15G and Form 15H are now called Form 121. However, for withdrawals processed during FY 2025-26 and the ITR filing in July 2026, the old Act 1961 provisions under Tab 1 apply.

Who can submit Form 15G: Individuals below 60 years of age whose estimated total income for the year does not exceed the basic exemption limit and on whom no tax is payable.

Who can submit Form 15H: Senior citizens (60 years and above) whose estimated tax liability for the year is nil.

Important for salaried professionals: If your salary income alone already exceeds the basic exemption limit of Rs. 3 lakh (new regime) or Rs. 2.5 lakh (old regime), you are not eligible to submit Form 15G regardless of how small your EPF withdrawal is. Form 15G for EPF is primarily relevant for those who have left employment and have no other significant income in the year of withdrawal.

Submit the form online through the EPFO member portal at the time of raising your withdrawal claim. If TDS has already been deducted and you were eligible for Form 15G, claim a full refund by filing your ITR correctly and crediting the TDS shown in your Form 168. The ITR filing last date for FY 2025-26 is July 31, 2026.

What Happens If PAN Is Not Linked to UAN?

If your PAN is not linked to your UAN at the time of EPF withdrawal, EPFO deducts TDS at 20% instead of 10%. On a withdrawal of Rs. 4,80,000, this means Rs. 96,000 in TDS instead of Rs. 48,000.

To avoid this, ensure your PAN is linked to your UAN through the EPFO member portal before raising any withdrawal request. Linking your PAN also ensures the TDS reflects correctly in your Form 168, which is essential when you file your ITR and claim TDS credit. For more on how TDS is handled across different income types, see our guide on TDS on salary under Section 192.

Partial Withdrawals and EPF Advances: Are They Taxable?

EPF allows certain partial withdrawals for specific purposes such as medical emergencies, home purchase, home loan repayment, education, and marriage. These are technically treated as advances against your EPF balance, not final withdrawals.

Advances from EPF for these specified purposes are not taxable, regardless of how many years of service you have completed. No TDS is deducted on these advances, and you do not need to declare them as income in your ITR.

Only a final settlement or full withdrawal of your EPF balance triggers the taxability and TDS rules discussed in this article.

Before vs After 5 Years: Quick Comparison

| Factor | Before 5 Years | After 5 Years |

|---|---|---|

| TDS applicable | Yes, if amount above Rs. 50,000 | No |

| TDS rate (PAN linked) | 10% | Nil |

| TDS rate (PAN not linked) | 20% | Nil |

| Taxability | Partially taxable | Fully exempt under Section 10(12) |

| Employer EPF contribution | Taxable as salary | Exempt |

| Employee contribution | Not taxable (80C reversal if applicable) | Exempt |

| Interest earned | Taxable as IFOS | Exempt |

| 80C deduction reversal | Yes, if previously claimed | No |

| Form 15G applicable | Only if total income below exemption limit | Not needed |

| Declare in ITR | Yes, taxable portion | Report under Schedule EI (exempt income) |

What to Do If TDS Was Deducted on Your EPF Withdrawal

If EPFO deducted TDS on your EPF withdrawal and you believe you are entitled to a refund, here is what to do.

First, verify that the TDS is reflecting in your Form 168 on the Income Tax portal. If it is not showing, contact EPFO with your UAN details and request a correction.

Once it reflects in Form 168, file your ITR for FY 2025-26 by July 31, 2026, declaring the taxable portion of the EPF withdrawal under the correct income head. Claim credit for the TDS deducted. If your tax liability is lower than the TDS deducted, the excess will be refunded to your bank account.

Conclusion

The 5-year rule is the single most important factor in determining your EPF withdrawal tax liability. Withdraw after 5 years and your entire EPF corpus is tax-free. Withdraw before 5 years and a portion of it becomes taxable, with TDS deducted upfront by EPFO.

If you are in a situation where early withdrawal is unavoidable, make sure your PAN is linked to your UAN to limit TDS to 10% instead of 20%. Check your Form 15G eligibility carefully, keeping in mind that salaried professionals with active income are rarely eligible. And always file your ITR to claim back any excess TDS that was deducted.

Frequently Asked Questions

Is EPF withdrawal taxable after 5 years?

No. After 5 years of continuous service, the entire EPF withdrawal is exempt from tax under Section 10(12). No TDS is deducted. You do not need to declare it as taxable income but should report it under Schedule EI in your ITR.

What is the TDS rate on EPF withdrawal before 5 years?

10% if your PAN is linked to your UAN. 20% if PAN is not linked or not available. TDS applies only if the withdrawal amount exceeds Rs. 50,000.

If I changed jobs and transferred my PF, does the 5-year count restart?

No. If you transferred your PF balance to your new employer’s account instead of withdrawing it, your previous service period is included in the 5-year count. Only withdrawing the PF balance at the time of job change resets the counter.

Can I submit Form 15G for EPF withdrawal even if I am withdrawing before 5 years?

Only if your estimated total income for the year is below the basic exemption limit and your tax liability is nil. Most salaried professionals with active salary income will not meet this condition and are not eligible for Form 15G on EPF withdrawal.

What if EPFO deducted TDS at 20% because my PAN was not linked?

Link your PAN to your UAN immediately. For TDS already deducted at 20%, file your ITR and claim the full TDS credit. If your actual tax liability on the withdrawal is less than 20%, you will receive the excess as a refund.

Are partial EPF withdrawals for medical or housing purposes taxable?

No. EPF advances for specified purposes such as medical emergencies, home purchase, education, or marriage are not treated as income and are not taxable. No TDS is deducted on these advances.