ELSS vs Tax Saver FD vs NSC: Best 80C Investment Comparison 2026

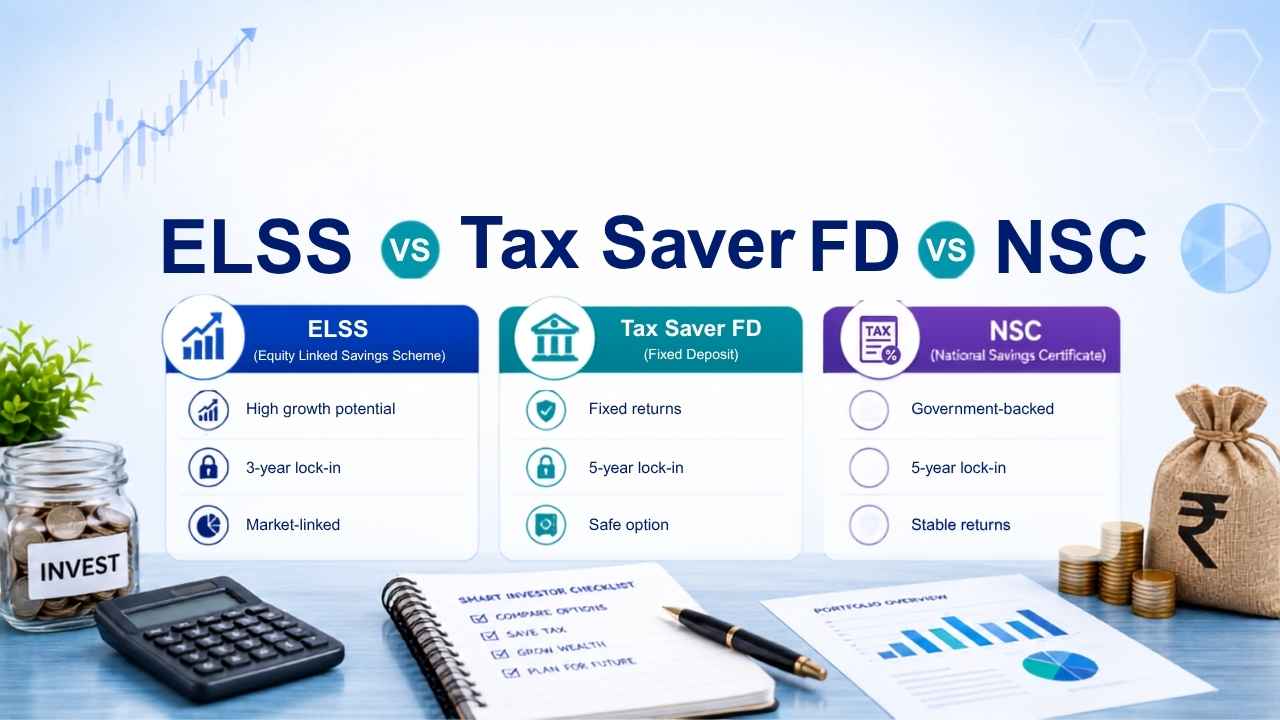

ELSS vs tax saver FD vs NSC is the question every salaried professional faces at the start of each financial year when planning Section 80C investments. All three qualify for a deduction of up to Rs. 1.5 lakh under the old tax regime, but they could not be more different in terms of risk, returns, lock-in period, and tax treatment.

In my seven years of working with salaried professionals on tax planning, I have seen people pick an 80C option simply because their bank recommended it or because their parents invested in it. That approach consistently leads to suboptimal outcomes. The right choice among ELSS, tax saver FD, and NSC depends entirely on three things: your risk appetite, your tax slab, and how long you can stay invested.

This guide gives you a side-by-side breakdown with verified numbers for FY 2025-26.

Quick Comparison: ELSS vs Tax Saver FD vs NSC

| Feature | ELSS | Tax Saver FD | NSC |

|---|---|---|---|

| Nature | Equity mutual fund | Bank fixed deposit | Post office savings |

| Lock-in Period | 3 years (shortest) | 5 years | 5 years |

| Current Returns | Market-linked (~12% CAGR historical) | 6.35% to 6.5% p.a. | 7.7% p.a. (Q1 FY 2026-27) |

| Returns Guarantee | Not guaranteed | 100% fixed | 100% fixed |

| Capital Safety | No guarantee | 100% safe (DICGC Rs.5L) | 100% safe (sovereign guarantee) |

| Section 80C Deduction | Yes (old regime only) | Yes (old regime only) | Yes (old regime only) |

| New Regime Benefit | Not available | Not available | Not available |

| Minimum Investment | Rs. 500 via SIP | Rs. 100 to Rs. 1,000 | Rs. 1,000 |

| Maximum for 80C | Rs. 1.5 lakh | Rs. 1.5 lakh | No upper limit (80C on Rs.1.5L) |

| Tax on Returns | LTCG 12.5% above Rs. 1.25L | Slab rate every year | Year 5 interest at slab rate only |

| Tax Payment Timing | Only at redemption | Annually (even in cumulative FD) | Only in Year 5 |

| TDS by Institution | No TDS on capital gains | 10% if annual interest >Rs. 50,000 | No TDS |

| Premature Exit | Not allowed before 3 years | Not allowed before 5 years | Not allowed before 5 years |

| Liquidity after Lock-in | Anytime after 3 years | Anytime after 5 years | Anytime after 5 years |

| Loan Against Investment | Not available | Not available (tax saver FD) | Yes (can be pledged) |

| Maturity Value (Rs.1.5L, 5 yr) | Rs. 2,64,351 (at 12% CAGR) | Rs. 2,07,063 (at 6.5%) | Rs. 2,17,355 (at 7.7%) |

| Post-Tax Maturity (30% slab) | Rs. 2,64,351 (zero LTCG within exemption) | ~Rs. 1,91,853 | ~Rs. 2,12,507 |

| Best For | Long-term equity growth, 30% slab investors | Capital safety, senior citizens, low tax slab | Guaranteed returns better than FD, tax deferral benefit |

All three options are relevant only if you are in the old tax regime. Under the new tax regime, Section 80C deductions are not available, which means none of these instruments offer any additional tax benefit over regular investments. If you have switched to the new regime, refer to my guide on the old vs new tax regime to understand whether this deduction is worth switching back for.

ELSS: Equity Linked Savings Scheme

ELSS is a diversified equity mutual fund that qualifies for Section 80C deduction. It invests primarily in equities and has a mandatory 3-year lock-in – the shortest among all 80C options. You can invest via SIP or lump sum. For the official ELSS category definition and registered fund houses, refer to AMFI India.

Returns

ELSS returns are market-linked and not guaranteed. Historically, diversified large-cap and multi-cap ELSS funds have delivered 10% to 14% CAGR over 10-year periods. For this comparison, I am using a conservative 12% CAGR.

Example: Rs. 1,50,000 invested in ELSS at 12% CAGR

| Tenure | Value at Exit | Gain |

|---|---|---|

| At 3 years (minimum) | Rs. 2,10,739 | Rs. 60,739 |

| At 5 years | Rs. 2,64,351 | Rs. 1,14,351 |

These are indicative figures. Actual returns depend on market conditions and which fund you choose. In a bad market cycle, a 3-year ELSS could show flat or negative returns.

Tax on ELSS Gains

ELSS gains are treated as Long Term Capital Gains since the minimum holding is 3 years. LTCG up to Rs. 1.25 lakh per financial year is exempt from tax. Gains above Rs. 1.25 lakh are taxed at 12.5% plus 4% cess.

In the example above, at the 3-year exit point, the gain of Rs. 60,739 is entirely within the Rs. 1.25 lakh annual exemption – zero tax. At 5 years with Rs. 1,14,351 gain, still within the exemption – zero LTCG tax payable. Since the minimum holding period is 3 years, all ELSS gains at redemption are Long Term Capital Gains by definition.

Who Should Choose ELSS

ELSS suits investors who are comfortable with equity market risk, have at least a 5 to 7 year investment horizon beyond the lock-in, and are in the 20% to 30% tax bracket where the tax efficiency of LTCG matters most.

Tax Saver FD: 5-Year Fixed Deposit

A tax saver FD is a bank fixed deposit with a 5-year lock-in period. It qualifies for Section 80C deduction exactly like ELSS and NSC. The key difference is predictability; the interest rate is locked in at the time of opening and does not change over the tenure.

Current Interest Rates (2026)

| Bank | General Citizens | Senior Citizens |

|---|---|---|

| SBI | 6.50% p.a. | 7.00% p.a. (7.50% under SBI WeCare scheme) |

| HDFC Bank | 6.35% p.a. | 6.85% p.a. |

| ICICI Bank | 6.50% p.a. | 7.10% p.a. |

| Axis Bank | 6.45% p.a. | 6.95% p.a. |

For this comparison, I am using 6.5% p.a. (SBI/ICICI representative rate) with quarterly compounding, which is standard for most bank FDs.

Example: Rs. 1,50,000 in Tax Saver FD at 6.5% p.a. (quarterly compounding, 5 years)

| Particulars | Amount |

|---|---|

| Principal | Rs. 1,50,000 |

| Rate | 6.5% p.a. (quarterly compounding) |

| Maturity value | Rs. 2,07,063 |

| Total interest | Rs. 57,063 |

Tax on Tax Saver FD Interest

This is where tax saver FDs become significantly less attractive for high-bracket investors. The interest earned on FD is taxed at your applicable slab rate every year as it accrues – not at maturity. This applies even to cumulative FDs where interest is reinvested rather than paid out.

For an investment of Rs. 1.5 lakh at 6.5%, the annual interest earned is approximately Rs. 9,750 – well below the Rs. 50,000 TDS threshold for general citizens. The bank will not deduct TDS on this amount. However, you must still declare this interest income in your ITR every year under Income from Other Sources. The absence of TDS does not mean the income is exempt from tax.

For a professional in the 30% tax bracket, the annual tax burden on Rs. 9,750 in interest is approximately Rs. 3,042 (30% plus 4% cess). Over 5 years, this adds up to roughly Rs. 15,210 in additional tax paid on the interest income.

The 80C deduction on the principal saves Rs. 45,000 in tax (30% of Rs. 1.5 lakh), which is common across all three options.

Who Should Choose Tax Saver FD

Tax saver FDs suit conservative investors who cannot tolerate any capital risk, retirees or near-retirees who benefit from senior citizen rates, and investors in the 5% to 10% tax slab where the annual tax on FD interest is minimal.

NSC: National Savings Certificate

NSC is a government-backed post office savings instrument with a 5-year tenure. It is considered one of the safest fixed-income instruments in India, backed by a sovereign guarantee – the same credibility as a Government of India bond.

Current Rate

The NSC interest rate for Q1 FY 2026-27 (April to June 2026) is 7.7% per annum, compounded annually and paid in full at maturity. This rate has held steady since April 2023.

Example: Rs. 1,50,000 in NSC at 7.7% p.a. (compounded annually, 5 years)

| Year | Opening Balance | Interest Earned | Closing Balance |

|---|---|---|---|

| Year 1 | Rs. 1,50,000 | Rs. 11,550 | Rs. 1,61,550 |

| Year 2 | Rs. 1,61,550 | Rs. 12,439 | Rs. 1,73,989 |

| Year 3 | Rs. 1,73,989 | Rs. 13,397 | Rs. 1,87,387 |

| Year 4 | Rs. 1,87,387 | Rs. 14,429 | Rs. 2,01,815 |

| Year 5 | Rs. 2,01,815 | Rs. 15,540 | Rs. 2,17,355 |

| Particulars | Amount |

|---|---|

| Principal | Rs. 1,50,000 |

| Total interest earned | Rs. 67,355 |

| Maturity value | Rs. 2,17,355 |

NSC Tax Treatment: The Key Advantage

NSC has a unique and often misunderstood tax treatment.

Years 1 to 4: The interest accrued is not paid out – it is reinvested in the certificate automatically. This reinvested interest is deemed to be a fresh investment under Section 80C and qualifies for an additional 80C deduction, subject to the Rs. 1.5 lakh annual cap.

| Year | Interest Accrued | 80C Treatment |

|---|---|---|

| Year 1 | Rs. 11,550 | Deductible under 80C (if cap available) |

| Year 2 | Rs. 12,439 | Deductible under 80C (if cap available) |

| Year 3 | Rs. 13,397 | Deductible under 80C (if cap available) |

| Year 4 | Rs. 14,429 | Deductible under 80C (if cap available) |

| Year 5 | Rs. 15,540 | Taxable at slab rate |

Year 5: The final year’s interest of Rs. 15,540 is taxable at your applicable slab rate and is not eligible for any 80C deduction.

Important clarification on the 80C interest benefit: If you have invested the full Rs. 1.5 lakh in NSC itself, there is no remaining room in the annual 80C cap for the accrued interest to get an additional deduction. This benefit works best for investors who split their 80C allocation. For example, if you invest Rs. 80,000 in NSC and Rs. 70,000 in ELSS, your Year 1 NSC interest of approximately Rs. 6,160 can still get an 80C deduction since the Rs. 1.5 lakh cap is not fully exhausted by NSC alone. Investors who put the entire Rs. 1.5 lakh into NSC do not get this additional benefit.

For an investor in the 30% slab, tax on Year 5 interest = Rs. 15,540 x 30% x 1.04 (cess) = approximately Rs. 4,848.

Who Should Choose NSC

NSC suits conservative investors who want guaranteed returns better than typical tax saver FDs, can leave money untouched for 5 years, and have not fully exhausted the Rs. 1.5 lakh 80C limit through other instruments so they can benefit from the Years 1 to 4 interest deduction.

Tax Efficiency Comparison

A critical factor that most comparison articles miss is the timing of when tax is paid.

Tax Saver FD: Tax liability arises every year on accrued interest, regardless of whether you receive the money or not. In a 30% slab, you pay approximately Rs. 3,042 in additional tax each year on the interest. This cash outflow happens throughout the 5-year period.

NSC: Tax liability arises only in Year 5 on the final year’s interest. Years 1 to 4 interest gets 80C deduction if cap is available. This deferred tax structure makes NSC significantly more tax-efficient than tax saver FD for most investors.

ELSS: Tax liability arises only at redemption. With the Rs. 1.25 lakh annual LTCG exemption, most individual investors who stay invested for 5 years face little to no tax on ELSS gains. This makes it the most tax-efficient of the three – when returns are positive.

Impact of the New Tax Regime

This is a critical point that many investors miss in 2026. All three instruments – ELSS, tax saver FD, and NSC – qualify for Section 80C deduction only under the old tax regime. Under the new tax regime, Section 80C is not available.

If you are a salaried professional who has opted for the new tax regime (which is the default from FY 2023-24), investing in any of these purely for tax saving makes no sense. The return on investment should be evaluated purely on its financial merits, independent of any tax deduction.

To understand your complete deduction picture under both regimes, refer to my guide on Section 80C deductions. For a comprehensive view of tax saving options under both regimes, my guide on tax saving tips for salaried employees covers the full range.

Who Should Choose What: Decision Framework

Choose ELSS if:

- You are in the old tax regime and want to exhaust your 80C limit

- You can stay invested for at least 5 to 7 years beyond the lock-in

- You are comfortable with equity market volatility

- You are in the 20% to 30% tax bracket and want the most tax-efficient long-term return

- You already have adequate fixed-income investments elsewhere in your portfolio

Choose Tax Saver FD if:

- You are in the old tax regime and specifically need capital protection

- You are in the 0% to 5% tax slab where annual interest tax is minimal

- You are a senior citizen benefiting from preferential rates

- You want the simplicity of a bank product you already use

Choose NSC if:

- You are in the old tax regime and want better guaranteed returns than bank FDs

- You are comfortable with a post office product

- You have not fully exhausted your 80C limit in other investments so the Years 1 to 4 interest can get additional deduction

- You are in the 20% to 30% slab and want the tax deferral advantage over FDs

Combination approach: Many salaried professionals in the 30% bracket use ELSS for growth and NSC for the stable portion of their 80C allocation, avoiding tax saver FDs altogether due to the annual tax drag.

Conclusion

For a salaried professional in the old tax regime with a long investment horizon and moderate risk appetite, ELSS offers the best long-term outcome when markets perform well. NSC is the stronger guaranteed-return option, ahead of tax saver FDs at current rates due to both the higher rate of 7.7% and the better tax treatment of its interest income.

Tax saver FDs make sense mainly for conservative investors, senior citizens who get preferential rates, or those in the lowest tax brackets where the annual tax on FD interest is not a meaningful drag.

The most important reminder for 2026: if you are in the new tax regime, none of these three provide any tax benefit on the investment itself. Evaluate them purely as investment products, not as tax-saving tools. For income tax slabs and which regime applies to you, refer to my guide on income tax slabs FY 2026-27.

Frequently Asked Questions

Can I invest in all three under Section 80C?

Yes. You can split your Rs. 1.5 lakh 80C limit across ELSS, tax saver FD, and NSC in any combination. The total deduction is still capped at Rs. 1.5 lakh regardless of how many instruments you use.

Is ELSS better than NSC in every situation?

Not necessarily. ELSS is better when markets perform well. In a period of poor equity returns, ELSS could underperform NSC. NSC’s 7.7% is guaranteed; ELSS returns are not. Investors near retirement should prefer NSC over ELSS.

Can NRIs invest in NSC?

No. NSC is restricted to resident Indians. NRIs cannot open a new NSC account, though they may continue holding existing certificates till maturity.

What happens if I need money before the lock-in ends?

None of the three allow premature withdrawal under normal circumstances. Tax saver FDs and NSC can only be redeemed before maturity in exceptional cases like death of the investor or court order. ELSS units cannot be redeemed before 3 years under any circumstances.

Is NSC interest compounded monthly or annually?

NSC interest is compounded annually, not monthly. The interest for each year gets added to the principal and earns further interest in subsequent years, but the compounding happens once a year.

Which gives the highest maturity value on Rs. 1.5 lakh over 5 years?

At historical averages, ELSS gives the highest maturity value at Rs. 2,64,351 (12% CAGR assumption). NSC gives Rs. 2,17,355. Tax Saver FD gives Rs. 2,07,063 at 6.5%. But ELSS returns are not guaranteed; NSC and FD returns are.

Will the bank deduct TDS on my tax saver FD interest?

If your annual FD interest from a single bank is below Rs. 50,000 (Rs. 1 lakh for senior citizens), the bank will not deduct TDS. For Rs. 1.5 lakh invested at 6.5%, annual interest is approximately Rs. 9,750, which is below the threshold. However, you must still declare this interest in your ITR every year.