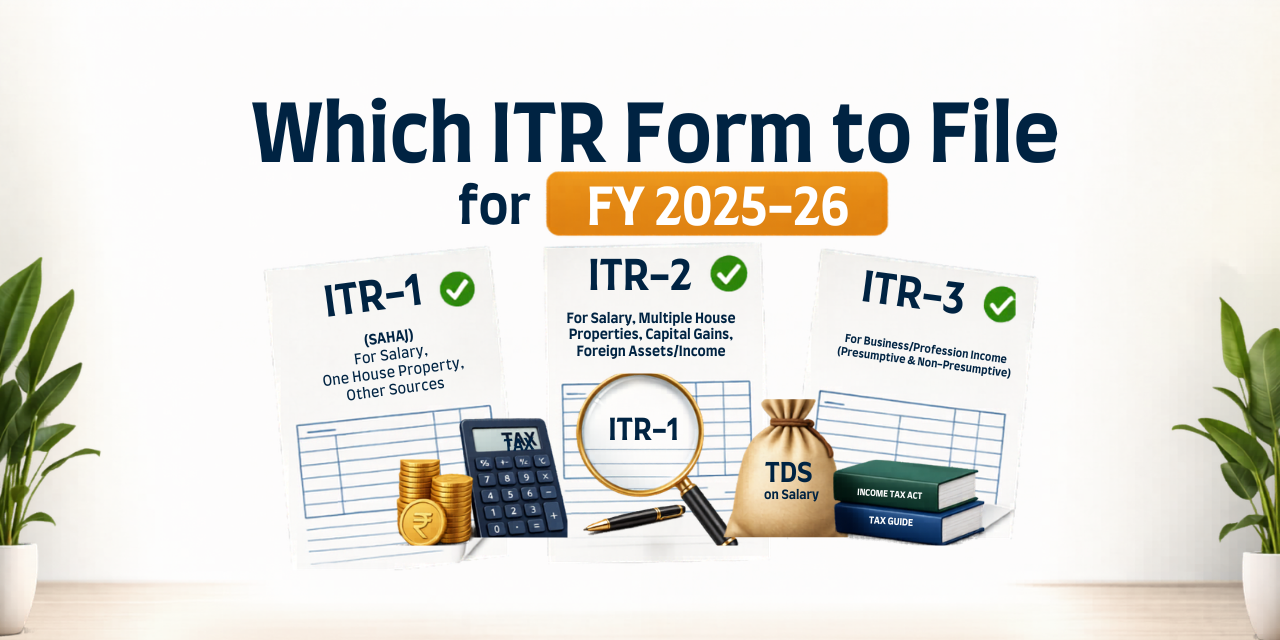

Which ITR Form to File for FY 2025-26: Complete Decision Guide

Which ITR Form to File for FY 2025-26?

Filing the wrong ITR form is not a minor mistake. The income tax department classifies it as a defective return under Section 139(9) and sends you a notice to correct it within 15 days. If you miss that window, your return is treated as not filed at all, which means penalties, interest, and loss of carry-forward benefits.

Every year, lakhs of taxpayers in India file the wrong ITR form, either because they did not know their income situation required a different form, or because their situation changed from the previous year and they used the same form out of habit.

With 7 years of experience in income tax education, I have seen this mistake repeatedly. This guide gives you a clear, scenario-based decision framework so you know exactly which form applies to your situation for FY 2025-26.

Quick Decision Chart: Which ITR Form Is Right for You?

| Your Situation | Correct Form | Deadline |

|---|---|---|

| Salaried, income below Rs. 50 lakh, no capital gains above Rs. 1.25 lakh, one house property | ITR-1 (Sahaj) | July 31, 2026 |

| Salaried with capital gains from stocks or mutual funds, two or more house properties, income above Rs. 50 lakh, director of a company | ITR-2 | July 31, 2026 |

| Freelancer, consultant, business owner (not under presumptive scheme), individual with both salary and professional income | ITR-3 | August 31, 2026 |

| Freelancer or small business under presumptive taxation (Section 44AD, 44ADA, 44AE), income below Rs. 50 lakh | ITR-4 (Sugam) | August 31, 2026 |

| Partnership firms, LLPs, AOPs, BOIs | ITR-5 | October 31, 2026 |

| Companies (all types except those claiming exemption under Section 11) | ITR-6 | October 31, 2026 |

| Trusts, political parties, universities, mutual funds, scientific research institutions | ITR-7 | October 31, 2026 |

For most individual taxpayers reading this, the choice is between ITR-1, ITR-2, ITR-3, and ITR-4. The sections below explain each in detail.

ITR-1 (Sahaj): The Simplest Form for Salaried Professionals

Who Can File ITR-1?

ITR-1 is for resident individuals (not HUFs) whose total income does not exceed Rs. 50 lakh from the following sources only:

- Salary or pension

- Income from one house property (excluding brought-forward losses)

- Income from other sources (interest from savings account, FD interest, family pension)

- Agricultural income up to Rs. 5,000

- Long-term capital gains under Section 112A up to Rs. 1.25 lakh with no brought-forward or carry-forward losses (new addition from AY 2025-26)

Who Cannot File ITR-1?

- Non-resident Indians (NRIs)

- Directors of any company

- Individuals who hold unlisted equity shares

- Individuals with income from business or profession

- Individuals with capital gains above Rs. 1.25 lakh or any short-term capital gains

- Individuals with more than one house property

- Individuals with foreign income or foreign assets

- Individuals with agricultural income above Rs. 5,000

- Individuals whose TDS has been deferred on ESOPs

New Change in ITR-1 for FY 2025-26

From AY 2025-26 onwards, small investors with long-term capital gains up to Rs. 1.25 lakh from listed equity shares or equity mutual funds can now file ITR-1, provided there are no brought-forward or carry-forward capital losses. Earlier, any capital gains income required ITR-2. This is a significant simplification for small investors who sold a few mutual fund units during the year.

ITR-2: For Salaried Professionals with Complex Income

Who Should File ITR-2?

ITR-2 is for resident and non-resident individuals and HUFs who have income from any source except business or profession. You must file ITR-2 if:

- Total income exceeds Rs. 50 lakh

- You have capital gains from stocks, mutual funds, or property sale

- You have long-term capital gains above Rs. 1.25 lakh

- You have short-term capital gains (any amount)

- You are a director of any company

- You hold unlisted equity shares

- You have income from more than one house property

- You are an NRI with Indian income

- You have foreign assets or foreign bank accounts

- You have income from winning lottery, horse racing, or gambling

- You have agricultural income above Rs. 5,000

Common Real Scenario: When to Switch from ITR-1 to ITR-2

Priya has been filing ITR-1 for 3 years as a salaried employee. In FY 2025-26, she sold mutual funds and earned Rs. 2 lakh in short-term capital gains. Even though her total income is below Rs. 50 lakh and she has just one salary, she must now file ITR-2 because she has short-term capital gains.

This is one of the most common mistakes salaried investors make. If you sold any stocks or mutual funds in FY 2025-26, check whether those sales resulted in capital gains. Even Rs. 5,000 in short-term capital gains requires ITR-2.

ITR-3: For Freelancers, Consultants, and Business Owners

Who Should File ITR-3?

ITR-3 is for individuals and HUFs who have income from business or profession. File ITR-3 if:

- You are a freelancer or independent consultant earning professional fees

- You run a business of any kind

- You have both salary income and freelance or business income

- You are a partner in a partnership firm

- You have income from business but are not eligible for or do not want the presumptive taxation scheme

- Your professional gross receipts exceed Rs. 75 lakh (cannot use ITR-4)

- You want to claim actual business expenses instead of the 50% presumptive deduction

ITR-3 vs ITR-4: The Key Question

If you are a freelancer or small business owner, you can choose between ITR-3 and ITR-4. ITR-4 is simpler. The decision comes down to whether you qualify for and benefit from the presumptive taxation scheme under Section 44ADA or 44AD.

Read the complete guide on income tax for freelancers to understand which option saves more tax in your situation.

ITR-4 (Sugam): For Freelancers Under Presumptive Taxation

Who Can File ITR-4?

ITR-4 is for resident individuals, HUFs, and firms (other than LLPs) who have opted for the presumptive taxation scheme. You can file ITR-4 if:

- You are a freelancer or professional under Section 44ADA (gross receipts up to Rs. 75 lakh, if 95% digital)

- You run a small business under Section 44AD (turnover up to Rs. 3 crore, if 95% digital)

- You are a goods transport operator under Section 44AE

- Total income does not exceed Rs. 50 lakh

- Income from one house property only (excluding losses)

- Long-term capital gains under Section 112A up to Rs. 1.25 lakh

When You Cannot Use ITR-4

- If you are a director of a company

- If you hold unlisted equity shares

- If your professional gross receipts exceed Rs. 75 lakh

- If you have short-term capital gains

- If you are an NRI

- If you want to carry forward business losses (ITR-4 does not allow this)

Scenarios That Confuse Most Taxpayers

Scenario 1: Salaried Employee Who Also Does Freelance Work

Rahul works full-time at an IT company (salary Rs. 12 lakh) and also does freelance content writing on weekends (income Rs. 3 lakh).

Which form: ITR-3 or ITR-4, not ITR-1 or ITR-2. His freelance income is business/professional income. If his freelance income qualifies under Section 44ADA and total income is below Rs. 50 lakh, he can use ITR-4. Otherwise ITR-3.

Many salaried people in this situation file ITR-1 out of habit. This is a defective return.

Scenario 2: Salaried Employee Who Sold Stocks

Anita is a salaried employee with total income of Rs. 8 lakh. She sold some shares and made Rs. 30,000 in short-term capital gains.

Which form: ITR-2, not ITR-1. Any short-term capital gains, regardless of amount, disqualify you from ITR-1.

Scenario 3: Salaried Employee With Two Flats

Vikram owns two flats. He lives in one and has given the other on rent. His salary is Rs. 15 lakh.

Which form: ITR-2, not ITR-1. Having two house properties disqualifies you from ITR-1, regardless of income level.

Scenario 4: Doctor with Private Practice

Dr. Sharma is a physician with professional income of Rs. 40 lakh from private practice. All receipts are through bank transfers.

Which form: ITR-4 (using Section 44ADA presumptive scheme) if gross receipts are within Rs. 75 lakh and total income is below Rs. 50 lakh. Otherwise ITR-3.

Scenario 5: Retired Person with Pension and FD Interest

Mr. Gupta is retired, receiving pension of Rs. 4 lakh per year and FD interest of Rs. 80,000. He has no other income.

Which form: ITR-1. Pension is treated as salary for ITR purposes, and FD interest falls under income from other sources. Both are covered under ITR-1.

Scenario 6: Company Director

Meena is a salaried employee and also serves as a director on the board of her family’s private limited company. Her only income is her Rs. 18 lakh salary.

Which form: ITR-2, not ITR-1. Being a director of any company, regardless of whether you earn director’s remuneration, disqualifies you from ITR-1.

Scenario 7: Person Who Changed Jobs in FY 2025-26

Suresh left Company A in September 2025 and joined Company B in October 2025. He has two Form 16s and only salary income below Rs. 50 lakh with no capital gains.

Which form: ITR-1 is fine as long as his total income stays below Rs. 50 lakh and he has no capital gains. But he must combine income from both Form 16s and declare the total. Do not file two separate returns.

What Happens If You File the Wrong ITR Form?

The income tax department will send you a defect notice under Section 139(9). You then have 15 days to respond and file the correct form.

If you do not respond within 15 days:

- Your return is treated as invalid (not filed at all)

- Penalty under Section 234F applies (Rs. 5,000 or Rs. 1,000 depending on income)

- You lose the right to carry forward capital losses, business losses, and other losses

- If you were expecting a refund, it is delayed until you file the correct form

- You may have to pay interest under Section 234A if the revised filing crosses the deadline

The good news: if you catch the mistake yourself before getting a notice, you can file a revised return using the correct form. This can be done until March 31, 2027 for FY

ITR Form Changes for FY 2025-26: What Is New

1. ITR-1 Can Now Include Limited LTCG

From AY 2025-26, small investors with long-term capital gains up to Rs. 1.25 lakh from listed shares or equity mutual funds can use ITR-1, provided there are no carried-forward losses. This was not allowed in previous years.

2. ITR-4 Also Allows Limited LTCG

Similar to ITR-1, ITR-4 now allows LTCG up to Rs. 1.25 lakh under Section 112A. Freelancers using the presumptive scheme who sold a few mutual fund units can still use ITR-4 as long as gains do not exceed Rs. 1.25 lakh and there are no brought-forward capital losses.

3. Deductions Must Be Selected from Dropdown

Earlier you could simply enter the deduction amount. From AY 2025-26, deductions under Sections 80C to 80U must be selected from a dropdown menu specifying the exact sub-section. This means you must know which specific investment (PPF, ELSS, LIC) falls under which clause. Review the complete Section 80C deductions guide before filing.

4. AIS Data Pre-filled More Comprehensively

The Annual Information Statement (AIS) now captures more data: GST turnover, securities transactions, foreign remittances, and all TDS credits. Before filing, download your AIS from the income tax portal and verify all information. Any mismatch between your declared income and AIS data triggers an automatic scrutiny notice.

ITR Form Comparison Table: Complete Quick Reference

| Feature | ITR-1 | ITR-2 | ITR-3 | ITR-4 |

|---|---|---|---|---|

| Salary income | Yes | Yes | Yes | Yes |

| Business or professional income | No | No | Yes (actual) | Yes (presumptive) |

| Capital gains | LTCG up to Rs 1.25L only | Yes (all) | Yes (all) | LTCG up to Rs 1.25L only |

| More than one house property | No | Yes | Yes | No |

| Foreign assets | No | Yes | Yes | No |

| Director of company | No | Yes | Yes | No |

| NRI | No | Yes | Yes | No |

| Income limit | Rs. 50 lakh | No limit | No limit | Rs. 50 lakh |

| Filing deadline | July 31, 2026 | July 31, 2026 | August 31, 2026 | August 31, 2026 |

Step-by-Step: How to Decide Your ITR Form

Step 1: Are you an individual or HUF? If yes, continue. If you are a company, LLP, or firm, you need ITR-5 or ITR-6.

Step 2: Do you have any business or professional income (freelancing, consulting, trading, running a shop)? If yes, go to Step 3. If no, go to Step 4.

Step 3: Do you qualify for and want to use the presumptive scheme (Section 44ADA or 44AD)? If yes, and if total income is below Rs. 50 lakh with no capital gains above Rs. 1.25 lakh, use ITR-4. If no, use ITR-3.

Step 4: Is your total income below Rs. 50 lakh? Do you have only salary, one house property, FD interest, and long-term capital gains not exceeding Rs. 1.25 lakh? Are you a resident Indian with no foreign assets and not a company director? If yes to all, use ITR-1.

Step 5: If you answered no to any part of Step 4, use ITR-2.

Frequently Asked Questions on ITR Form Selection

Can I file ITR-2 when ITR-1 is applicable?

Yes. ITR-2 covers more situations than ITR-1. If you are eligible for ITR-1 but file ITR-2 instead, it is technically valid. However, ITR-1 is simpler and faster to file. Use ITR-1 when eligible.

I sold mutual funds this year. Which ITR form do I use?

It depends on the type of gains. If you have only long-term capital gains (held more than 1 year) not exceeding Rs. 1.25 lakh with no brought-forward losses, you can still use ITR-1 or ITR-4. If gains exceed Rs. 1.25 lakh, or if you have any short-term capital gains, use ITR-2.

I am a salaried employee who also has rental income from one flat. Which form?

ITR-1, as long as total income is below Rs. 50 lakh and you have only one house property. Rental income from one property is covered under ITR-1 under the head income from house property.

I am a salaried person who started a small online business this year. Which form?

ITR-3 if you are maintaining actual books. ITR-4 if you opt for the presumptive scheme under Section 44AD and total income is below Rs. 50 lakh. You cannot use ITR-1 or ITR-2 once you have business income.

What if I used ITR-1 last year but my situation changed this year?

You must use the form that matches your current year situation, not last year. ITR form selection is based on income sources in that specific financial year. If you sold stocks, became a director, or started freelancing in FY 2025-26, your form changes accordingly for this filing.

I am a doctor with a private clinic. Which ITR form should I file?

ITR-4 if you opt for Section 44ADA (50% presumptive income) and your gross receipts are within Rs. 75 lakh. ITR-3 if receipts exceed Rs. 75 lakh or if you want to claim actual expenses.

Documents to Keep Ready Based on Your ITR Form

For all forms: PAN, Aadhaar, Form 26AS, AIS, bank statements, pre-validated bank account details.

Additional for ITR-1 and ITR-2: Form 16 from employer, rent receipts for HRA, investment proofs for Section 80C and 80D.

Additional for ITR-2: Capital gains statements from brokers and mutual fund houses, home loan interest certificate for second property.

Additional for ITR-3 and ITR-4: All invoices and receipts, bank statements showing professional receipts, business expense records.

For the complete ITR filing process step by step, read our guide on how to file ITR online. For understanding all deductions to maximize before filing, refer to the tax saving tips for salaried employees guide.

Questions about which ITR form applies to your specific situation? Drop them in the comments below.