HRA Exemption Calculation Guide FY 2025-26

Why Most Salaried Professionals Leave HRA Money on the Table

Every year, thousands of salaried professionals in India either skip their HRA exemption entirely or calculate it wrong. Not because the rule is complicated, but because nobody has explained it clearly with real numbers that match actual salaries.

I have worked with professionals earning anywhere from Rs. 6 lakh to Rs. 30 lakh annually, and the HRA mistakes are shockingly consistent: people in Bangalore claiming 50% metro rate (wrong), professionals paying Rs. 15,000 rent in cash with no trail (risky), and high earners not knowing they can legally pay rent to their parents and save an additional Rs. 40,000 to Rs. 60,000 in taxes every year.

This guide fixes all of that. Real numbers, real situations, no jargon.

Important: HRA exemption is available only under the old tax regime. If you have chosen the new tax regime, your entire HRA received is taxable. If you are unsure which regime suits you better, read the old vs new tax regime comparison before proceeding.

HRA Allowance vs HRA Exemption: The Difference That Matters

This is the first thing to get clear, because most professionals confuse these two terms.

- HRA Allowance: The amount your employer pays you as part of your CTC (fully taxable by default)

- HRA Exemption: The portion of that HRA which you can legally remove from your taxable income under Section 10(13A)

Your employer does not automatically exempt your entire HRA. The exemption is calculated using a specific formula, and only the eligible amount is tax-free. The rest gets added to your taxable salary.

This means even if your salary slip shows HRA of Rs. 25,000 per month, you might only get exemption on Rs. 12,000 or Rs. 18,000 depending on your rent and city. Knowing this number is what separates smart tax planning from guesswork.

Who Can Claim HRA Exemption?

All four conditions below must be true for you to claim HRA exemption:

- You are a salaried employee (self-employed professionals cannot claim under Section 10(13A))

- Your employer includes HRA as a named component in your salary structure or offer letter

- You actually live in rented accommodation

- You have opted for the old tax regime

If your employer does not pay HRA separately but you still pay rent, there is a separate provision called Section 80GG. I have covered that further below.

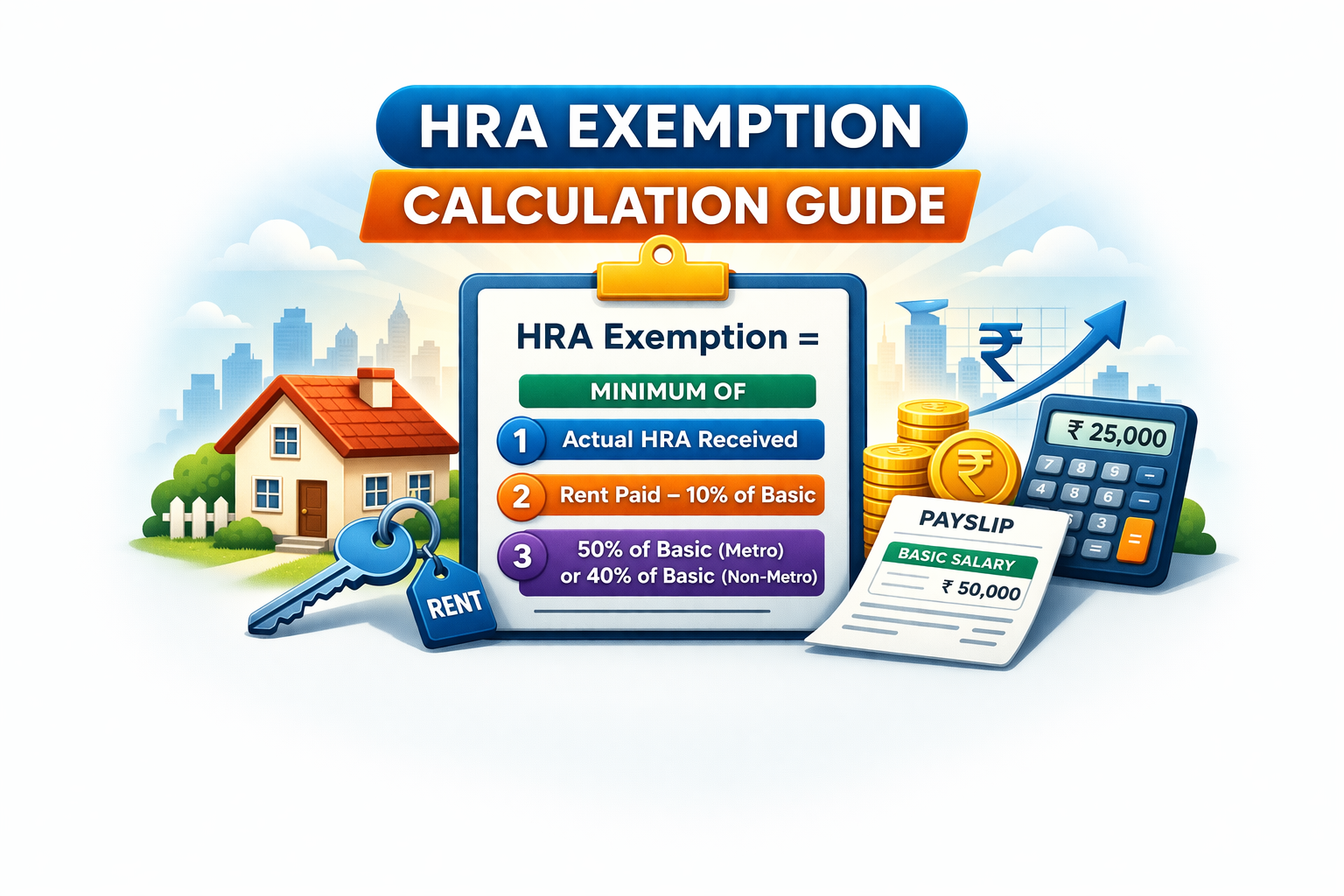

The HRA Exemption Formula: Three Conditions, Take the Lowest

The exempt amount is always the minimum (lowest) of these three:

| Condition | What to Calculate |

|---|---|

| Condition 1 | Actual HRA received from employer |

| Condition 2 | Actual rent paid minus 10% of Salary |

| Condition 3 | 50% of Salary if metro city, 40% if non-metro city |

Calculate all three. The lowest one is your HRA exemption for the year.

“Salary” here means Basic Salary plus Dearness Allowance (DA), but only the DA that forms part of retirement benefits. For most private sector professionals, there is no DA component, so “Salary” simply means Basic Salary.

Metro vs Non-Metro: The Most Common Mistake

This is where a large number of professionals, especially in South and West India, make an expensive error.

For HRA purposes, only these four cities are metro:

- Delhi

- Mumbai

- Kolkata

- Chennai

Every other city is non-metro, including Bangalore, Hyderabad, Pune, Ahmedabad, Jaipur, Chandigarh, Kochi, and all others.

This matters because metro city residents can use 50% of basic salary as Condition 3, while non-metro residents are capped at 40%. On a basic salary of Rs. 7 lakh, that is a difference of Rs. 70,000 in the cap alone.

| City | Classification | Condition 3 Cap |

|---|---|---|

| Delhi | Metro | 50% of Basic Salary |

| Mumbai | Metro | 50% of Basic Salary |

| Kolkata | Metro | 50% of Basic Salary |

| Chennai | Metro | 50% of Basic Salary |

| Bangalore | Non-Metro | 40% of Basic Salary |

| Hyderabad | Non-Metro | 40% of Basic Salary |

| Pune | Non-Metro | 40% of Basic Salary |

| Ahmedabad | Non-Metro | 40% of Basic Salary |

| All other cities | Non-Metro | 40% of Basic Salary |

HRA Calculation: 4 Real Salary Scenarios

Scenario 1: Mid-level professional in Delhi (Metro)

Basic Salary: Rs. 50,000/month, HRA received: Rs. 20,000/month, Rent paid: Rs. 18,000/month, City: Delhi

Annual figures: Basic Rs. 6,00,000 | HRA Rs. 2,40,000 | Rent Rs. 2,16,000

| Condition | Calculation | Amount |

|---|---|---|

| Condition 1 | Actual HRA received | Rs. 2,40,000 |

| Condition 2 | Rs. 2,16,000 minus 10% of Rs. 6,00,000 = Rs. 2,16,000 minus Rs. 60,000 | Rs. 1,56,000 |

| Condition 3 | 50% of Rs. 6,00,000 (metro) | Rs. 3,00,000 |

HRA Exemption = Rs. 1,56,000 (Condition 2 is the lowest)

Taxable HRA = Rs. 2,40,000 minus Rs. 1,56,000 = Rs. 84,000 added to taxable salary.

Scenario 2: IT professional in Bangalore (Non-Metro)

Basic Salary: Rs. 60,000/month, HRA received: Rs. 24,000/month, Rent paid: Rs. 22,000/month, City: Bangalore

Annual figures: Basic Rs. 7,20,000 | HRA Rs. 2,88,000 | Rent Rs. 2,64,000

| Condition | Calculation | Amount |

|---|---|---|

| Condition 1 | Actual HRA received | Rs. 2,88,000 |

| Condition 2 | Rs. 2,64,000 minus 10% of Rs. 7,20,000 = Rs. 2,64,000 minus Rs. 72,000 | Rs. 1,92,000 |

| Condition 3 | 40% of Rs. 7,20,000 (non-metro) | Rs. 2,88,000 |

HRA Exemption = Rs. 1,92,000 (Condition 2 is the lowest)

This is a practical example of why Bangalore professionals with similar rent and salary as Delhi colleagues get lower HRA exemption. The 40% non-metro cap reduces the ceiling significantly.

Scenario 3: Professional paying low rent relative to salary

Basic Salary: Rs. 40,000/month, HRA received: Rs. 15,000/month, Rent paid: Rs. 5,000/month, City: Pune

Annual figures: Basic Rs. 4,80,000 | HRA Rs. 1,80,000 | Rent Rs. 60,000

| Condition | Calculation | Amount |

|---|---|---|

| Condition 1 | Actual HRA received | Rs. 1,80,000 |

| Condition 2 | Rs. 60,000 minus 10% of Rs. 4,80,000 = Rs. 60,000 minus Rs. 48,000 | Rs. 12,000 |

| Condition 3 | 40% of Rs. 4,80,000 (non-metro) | Rs. 1,92,000 |

HRA Exemption = Rs. 12,000 only (Condition 2 is devastatingly low)

This is the reality for professionals who pay very low rent relative to their salary. Even though the employer gives Rs. 1,80,000 as HRA, the exemption is only Rs. 12,000. The remaining Rs. 1,68,000 is fully taxable.

Scenario 4: Senior professional in Mumbai (High salary, high rent)

Basic Salary: Rs. 1,00,000/month, HRA received: Rs. 50,000/month, Rent paid: Rs. 45,000/month, City: Mumbai

Annual figures: Basic Rs. 12,00,000 | HRA Rs. 6,00,000 | Rent Rs. 5,40,000

| Condition | Calculation | Amount |

|---|---|---|

| Condition 1 | Actual HRA received | Rs. 6,00,000 |

| Condition 2 | Rs. 5,40,000 minus 10% of Rs. 12,00,000 = Rs. 5,40,000 minus Rs. 1,20,000 | Rs. 4,20,000 |

| Condition 3 | 50% of Rs. 12,00,000 (metro) | Rs. 6,00,000 |

HRA Exemption = Rs. 4,20,000 (Condition 2 is the lowest)

At the 30% tax bracket, this single exemption saves approximately Rs. 1,31,040 in taxes annually. This is why HRA structuring matters for senior professionals in metro cities.

Skip the manual math entirely. Use our HRA Calculator to get your exact number in seconds.

Advanced Situations Most Guides Do Not Cover

Situation 1: Paying Rent to Parents

This is one of the most effective and completely legal tax strategies for professionals who live in a house owned by their parents.

How it works: You pay rent to your parents every month via bank transfer. You claim HRA exemption on that rent. Your parents declare that rent as income from house property in their ITR, but they get a standard deduction of 30% on it plus property tax deduction. If your parents are in a lower tax bracket or below the taxable income threshold, the family’s combined tax outgo reduces significantly.

What you need to do this correctly:

- Confirm the house is in your parent’s name (check property documents)

- Transfer rent every month via NEFT or UPI, never cash

- Create a simple rent agreement on stamp paper

- Collect signed rent receipts every month

- Ensure parents file ITR showing this rental income

One hard restriction: you cannot pay rent to your spouse and claim HRA. Only parents or any other non-dependent person who owns the property qualifies.

Situation 2: Claiming Both HRA and Home Loan Deductions

Yes, this is possible. Many professionals do not realise they can claim both simultaneously.

The scenario where this applies: You own a house in City A (with an active home loan) but work and live on rent in City B. In this case you can claim HRA exemption for rent paid in City B, home loan principal under Section 80C, and home loan interest under Section 24(b) up to Rs. 2,00,000 for the City A property.

Where to be careful: If your own house and your workplace are in the same city, tax authorities expect you to occupy your own house. Claiming HRA on top of a home loan in the same city can attract scrutiny. Maintain genuine proof of separate rental accommodation if you are in this situation.

Situation 3: Changed Jobs Mid-Year

Calculate HRA exemption separately for each employer’s period, then add both together for the annual figure.

For example, if you worked at Company A from April to September and joined Company B in October, calculate exemption for April to September using Company A’s salary and HRA data, then calculate October to March using Company B’s data. The total annual exemption is the sum of both periods.

When filing your ITR, you will need Form 16 from both employers. Your new employer would not have accounted for the previous employer’s HRA, so this consolidation happens at the ITR filing stage.

Situation 4: No HRA in Salary Structure (Section 80GG)

If your employer does not include HRA as a separate salary component, you cannot claim exemption under Section 10(13A). However, you may qualify for a deduction under Section 80GG if:

- You do not receive HRA from your employer

- You pay rent for your accommodation

- Neither you, your spouse, minor child, nor HUF owns any residential property at the place of work

Section 80GG deduction is the lowest of: Rs. 5,000 per month (Rs. 60,000 per year), 25% of total income, or actual rent paid minus 10% of total income. This limit is far lower than what most professionals can claim under regular HRA, but it is better than nothing.

Situation 5: Annual Rent Exceeds Rs. 1,00,000

If your monthly rent is above Rs. 8,333, your annual rent crosses Rs. 1 lakh. In this case, providing your landlord’s PAN to your employer is mandatory to claim HRA exemption.

If your landlord does not have or refuses to share their PAN, you can still claim the exemption while filing your ITR with full bank transfer proof and rent receipts. However, getting the PAN upfront is always the cleaner approach.

Documents You Must Keep Ready

| Document | When Required |

|---|---|

| Monthly rent receipts | Always, for every month |

| Rent agreement on stamp paper | Strongly recommended for all situations |

| Bank statements showing rent transfers | Strongly recommended, replaces cash proof |

| Landlord’s PAN | Mandatory when annual rent exceeds Rs. 1,00,000 |

| Parent’s property ownership proof | Required when paying rent to parents |

Always pay rent via bank transfer. Cash payments leave no verifiable trail and create unnecessary risk if you ever receive a tax notice. A UPI or NEFT transfer on the same date every month is the cleanest possible documentation.

How to Submit HRA to Your Employer

At the start of every financial year, your employer collects a declaration of planned exemptions and deductions via Form 12BB. In the HRA section, you declare your monthly rent, landlord’s name and address, and PAN if applicable.

Based on this declaration, your employer reduces your monthly TDS. At year end (typically January or February), your employer asks for actual rent receipts to verify.

If you miss the employer submission deadline, do not worry. You can still claim the full HRA exemption when you file your ITR. The excess TDS already deducted will come back as a refund.

HRA Exemption vs Section 80GG: Side by Side

| Feature | HRA Exemption Sec 10(13A) | Section 80GG |

|---|---|---|

| Who can claim | Salaried professionals receiving HRA | Salaried (no HRA) or self-employed |

| Condition | Must receive HRA from employer | Must NOT receive HRA |

| Maximum benefit | No upper cap, depends on salary and rent | Capped at Rs. 60,000 per year |

| Tax regime | Old regime only | Old regime only |

| House ownership | Can own house in another city | Must not own any house at place of work |

5 Mistakes That Cost Professionals Thousands Every Year

Mistake 1: Not claiming HRA at all

The most expensive mistake. Use our HRA Calculator right now to see what you are leaving behind. It takes under 2 minutes.

Mistake 2: Paying rent in cash

No bank trail means no proof. If you get a tax notice, a landlord saying “yes I received cash” is not sufficient documentation. Switch to bank transfer immediately.

Mistake 3: Assuming Bangalore or Hyderabad are metro cities

As covered above, only four cities are metro for HRA. Using 50% instead of 40% for non-metro cities is an incorrect claim that can be rejected.

Mistake 4: Not getting landlord PAN when rent crosses Rs. 1 lakh per year

If you pay Rs. 8,334 or more monthly, get the PAN upfront. Chasing it at year end when your employer deadline is approaching creates unnecessary pressure.

Mistake 5: Claiming HRA while in the new tax regime

HRA exemption does not exist in the new regime. If you have opted for it, your entire HRA is taxable. Run both regimes through a comparison before deciding. The old vs new tax regime guide has salary-wise examples to help you decide.

Frequently Asked Questions

Is HRA exemption available in the new tax regime?

No. HRA exemption is not available under the new tax regime. The entire HRA received forms part of your taxable salary. This is one of the primary reasons why professionals paying significant rent tend to save more under the old tax regime.

Can I claim HRA if I live in my own house?

No. HRA exemption requires you to actually pay rent for accommodation you live in. If you own and occupy your own home, any HRA received from your employer is fully taxable.

Is Bangalore a metro city for HRA?

No. For HRA calculation, only Delhi, Mumbai, Kolkata, and Chennai are metro cities. Bangalore residents are subject to the 40% cap under Condition 3, not 50%.

Can I pay rent to my parents and claim HRA?

Yes, this is completely legal provided the house is genuinely owned by your parents, rent is paid via bank transfer, your parents show it as rental income in their ITR, and you have a proper rent agreement and receipts.

What if my rent changes during the year?

HRA exemption is calculated on a monthly basis. Calculate each month’s exemption separately using the rent applicable for that month, then total up all 12 months for the annual figure.

Is there a maximum limit on HRA exemption?

No fixed upper limit. The exemption is determined entirely by the three-condition formula based on your actual salary, HRA received, rent paid, and city type.

Can I claim both HRA and home loan tax benefits?

Yes, if your own property is in a different city from where you work and live on rent. You can claim HRA for your rented accommodation and simultaneously claim Section 80C principal and Section 24(b) interest deduction on your home loan.

What if I forgot to submit rent receipts to my employer?

You can still claim the full HRA exemption when filing your ITR. Your employer would have deducted higher TDS, but that excess amount will be refunded once you declare the correct exemption in your return.

The Bottom Line

HRA exemption is one of the largest tax benefits available to salaried professionals in India, and it requires no additional investment. You are already paying rent. The only question is whether you are claiming it correctly.

Three things to do right now:

- Use the HRA Calculator to find your exact exempt amount for this year

- Switch all rent payments to bank transfer if you have not already

- If your monthly rent is above Rs. 8,333, get your landlord’s PAN today

For the full picture of every deduction available to you under the old tax regime, including Section 80C investments, standard deduction, and more, read the Complete Income Tax Guide India 2025-26 and 2026-27.

Have a specific HRA situation you are unsure about? Drop it in the comments and I will work through the numbers with you.