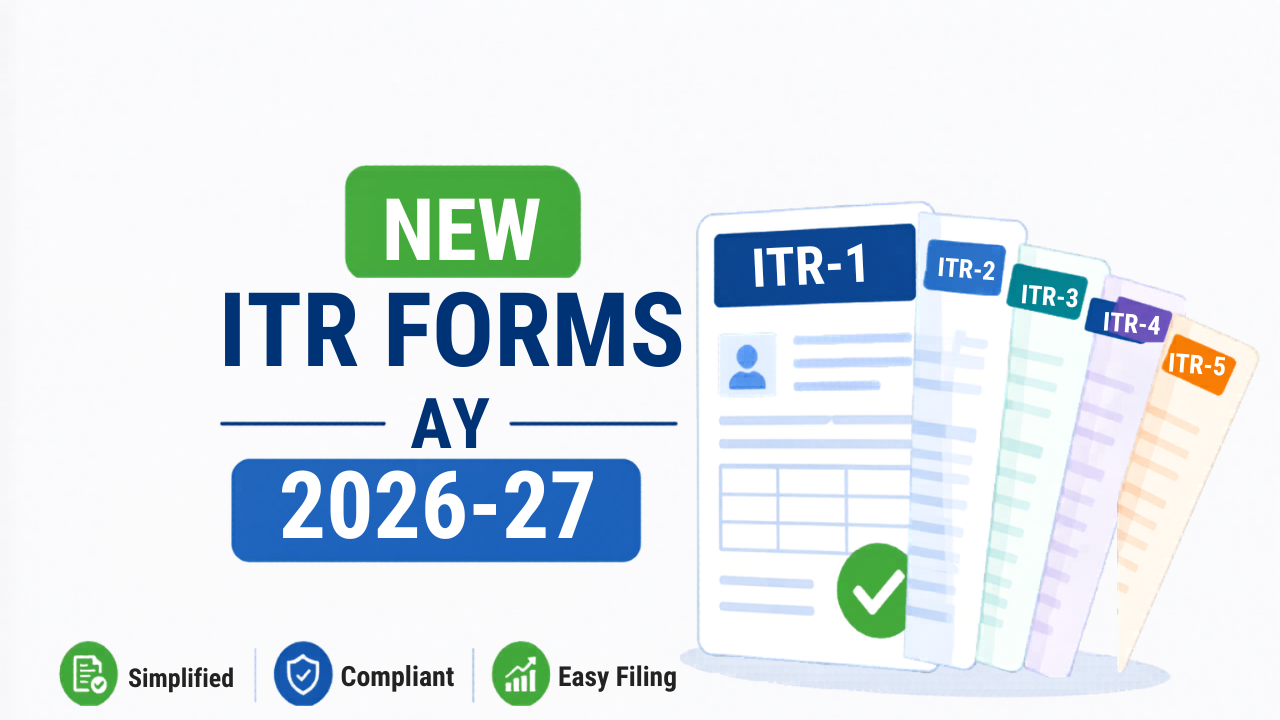

New ITR Forms AY 2026-27: Key Changes Every Taxpayer Must Know Before Filing

The Central Board of Direct Taxes (CBDT) notified the Income Tax Return forms for Assessment Year 2026-27 on March 30, 2026. This was followed by a corrigendum on April 10, 2026, correcting certain technical errors in the originally notified forms. The complete set includes ITR-1 through ITR-7, along with ITR-V and ITR-U.

This year, the ITR forms were notified before the start of the new financial year. Unlike the previous year, when late notification caused delays and eventually led to an extension of filing deadlines, taxpayers and professionals can now plan their filings in advance.

This article covers every key change in the new ITR forms AY 2026-27, who must file which form, and what is new this filing season.

Critical Clarification: Which Law Governs AY 2026-27 Returns?

Even though the Income Tax Act 2025 came into force from April 1, 2026, the ITR forms for AY 2026-27 are governed entirely by the Income Tax Act 1961.

This is because AY 2026-27 relates to income earned between April 1, 2025 and March 31, 2026, a period that falls under the old Act. The CBDT has confirmed this explicitly. The new ITR forms under the Income Tax Act 2025 will be applicable only from Tax Year 2026-27 onwards, meaning they will be notified before FY 2027-28 and used for returns filed in July 2027.

Taxpayers should therefore use the familiar old-regime section references such as 80C, 80D, 24(b), and 87A when filing their FY 2025-26 returns.

Complete List of ITR Forms for AY 2026-27

| Form | Who Should File |

|---|---|

| ITR-1 (Sahaj) | Resident individuals with total income up to Rs. 50 lakh from salary, up to two house properties, other sources, and LTCG under Section 112A up to Rs. 1.25 lakh |

| ITR-2 | Individuals and HUFs with income above Rs. 50 lakh, capital gains beyond the ITR-1 limit, foreign income, or more than two house properties |

| ITR-3 | Individuals and HUFs with income from business or profession |

| ITR-4 (Sugam) | Individuals, HUFs, and firms (excluding LLPs) opting for presumptive taxation under Sections 44AD, 44ADA, or 44AE with income up to Rs. 50 lakh |

| ITR-5 | Firms, LLPs, AOPs, and BOIs |

| ITR-6 | Companies other than those claiming exemption under Section 11 |

| ITR-7 | Trusts, political parties, and institutions filing under specific sections |

| ITR-V | Verification form when return is not e-verified electronically |

| ITR-U | Updated return to correct or add income within 48 months from end of relevant AY |

Biggest Change This Year: Expanded Scope of ITR-1

The most significant change in the AY 2026-27 forms is the expansion of ITR-1 (Sahaj).

For previous years, ITR-1 could be used only by taxpayers with income from one house property. From AY 2026-27, ITR-1 now allows reporting of income from up to two house properties.

This means a large number of salaried professionals who own two residential properties, one self-occupied and one vacant or let-out, can now file the simpler ITR-1 form instead of being required to shift to ITR-2.

However, ITR-1 still cannot be used in the following situations:

- Income from business or profession

- Capital gains exceeding Rs. 1.25 lakh under Section 112A (long-term capital gains on listed equity)

- Any other capital gains (short-term or otherwise)

- Foreign assets or foreign income

- Income from more than two house properties

- Agricultural income above Rs. 5,000

- Director in a company or holder of unlisted equity shares

Key Changes in ITR-2 for AY 2026-27

Removal of dual capital gains reporting: In AY 2025-26, ITR-2 required separate reporting of capital gains before July 23, 2024 and on or after July 23, 2024, due to the mid-year rate change introduced by the Finance Act 2024. Since no such mid-year rate change exists for FY 2025-26, this dual reporting requirement has been removed. Taxpayers with capital gains in FY 2025-26 will report them in a single schedule without date-wise bifurcation.

Detailed deduction disclosure: More granular disclosure is now required for deductions under Section 80C and Section 10(13A) (HRA). Taxpayers must provide specific breakdowns of the components they are claiming under these sections.

TDS section reporting: A new field requires taxpayers to specify the TDS section under which tax was deducted in the Details of TDS schedule. This improves accuracy and reconciliation with Form 26AS.

Buy-back loss reporting: A new field in the capital gains schedule allows taxpayers to report losses arising from share buy-backs, in line with the amended tax treatment of buy-backs introduced in FY 2024-25.

Reporting threshold raised: Detailed reporting is now required only if total income exceeds Rs. 1 crore. The earlier threshold was lower.

For a detailed guide on choosing the correct ITR form based on your income sources, see: Which ITR Form to File for FY 2025-26

Key Changes in ITR-3 for AY 2026-27

Extended due date now reflected in the form: The Finance Act 2026 extended the due date for filing ITR-3 from July 31 to August 31 for taxpayers with business or professional income whose accounts are not required to be audited. This change is now formally incorporated in Part A of ITR-3, where the taxpayer specifies the applicable due date.

This is an important update for non-audit professionals, freelancers, and self-employed individuals. If your accounts do not require a tax audit, your ITR-3 deadline for AY 2026-27 is August 31, 2026.

Key Changes in ITR-4 for AY 2026-27

New investment disclosure requirement: A new column has been added under Financial Particulars of the Business section in ITR-4. Taxpayers opting for the presumptive taxation scheme must now disclose the amount of investments made during the year. This is an additional disclosure requirement that was not present in earlier years.

Corrigendum corrections: The April 10, 2026 corrigendum corrected sub-row numbering under the Salary schedule in Part B (Gross Total Income) of ITR-4. Taxpayers filing ITR-4 must use the updated form available on the portal and not the version originally notified on March 30, 2026.

Changes in ITR-U (Updated Return) for AY 2026-27

Time limit extended to 48 months: The window to file an updated return under Section 139(8A) has been extended from 24 months to 48 months from the end of the relevant assessment year. This means taxpayers can correct past filing errors or report omitted income for up to 4 years after the end of the relevant AY.

For AY 2026-27, the updated return can be filed until March 31, 2031.

New column added: The updated ITR-U form for AY 2026-27 includes a new column in Part B ATI Computation for additional income-tax liability on updated income where the return is filed in response to a notice issued under Section 148. The applicable rate is 35%, 60%, 70%, or 80% of the additional tax liability depending on when the updated return is filed.

Penalty structure for ITR-U:

| When Filed | Additional Tax on Incremental Income |

|---|---|

| Within 12 months from end of AY | 25% |

| Between 12 and 24 months from end of AY | 50% |

| Between 24 and 36 months from end of AY | 60% |

| Between 36 and 48 months from end of AY | 70% |

ITR-V: Updated Verification Form

The ITR-V form has been updated and comes into effect from March 31, 2026. It applies to returns filed for AY 2026-27 where the taxpayer chooses to verify the return by sending a physical signed copy to the CPC in Bengaluru instead of e-verifying online.

E-verification through Aadhaar OTP or net banking remains the fastest and recommended method and does not require submission of ITR-V.

Corrigendum of April 10, 2026: What Was Corrected

The CBDT issued corrections to several ITR forms and schedules through notifications on April 10, 2026. Key corrections include:

ITR-1: Schedule-IT, which covers advance tax and self-assessment tax payment details, was completely substituted with a revised format. Taxpayers must use the updated ITR-1 utility from the portal.

ITR-4: Sub-row numbering under the Salary schedule in Part B was corrected.

Schedule CG (Capital Gains): Figure and letter references corrected. Certain columns in Schedule 112A and Schedule 115AD removed. Grey shading corrections made for clarity.

Schedule OS (Other Sources): Corrections to date columns in specific rows.

Schedule UD (Unabsorbed Depreciation): Mathematical expressions and figure references corrected.

All taxpayers should download the updated ITR utilities from the income tax portal before filing. Forms downloaded before April 10, 2026 may contain errors.

Deadlines for AY 2026-27

| Category | Due Date |

|---|---|

| Individuals with salary income (ITR-1, ITR-2) | July 31, 2026 |

| Individuals with business or professional income, non-audit (ITR-3, ITR-4) | August 31, 2026 |

| Tax audit cases | October 31, 2026 |

| Transfer pricing cases | November 30, 2026 |

| Belated return | December 31, 2026 |

| Revised return | March 31, 2027 |

| Updated return (ITR-U) | March 31, 2031 (48 months from end of AY 2026-27) |

For a complete guide on deadlines, penalties for late filing, and belated return rules, see: ITR Filing Last Date 2026

Which ITR Form Should You File? Quick Reference

Salaried employee with one or two house properties and no capital gains: ITR-1

Salaried employee with capital gains from mutual funds or stocks: ITR-2 (if LTCG under 112A exceeds Rs. 1.25 lakh or any STCG exists)

Salaried employee with LTCG under Section 112A up to Rs. 1.25 lakh: ITR-1 (new provision for AY 2026-27)

Freelancer or consultant with professional income: ITR-3 (actual income) or ITR-4 (if opting for presumptive taxation under Section 44ADA)

Small business owner under presumptive taxation: ITR-4

Partner in a firm: ITR-3

Taxpayers can download the updated ITR utilities directly from the official income tax portal.

Practical Tips for Filing AY 2026-27 Returns

Download updated forms: Always download ITR utilities from the income tax portal after April 10, 2026 to ensure you have the corrected versions.

Use Tab 1 on the portal: The income tax portal now shows two tabs, one for the Income Tax Act 1961 and one for the Income Tax Act 2025. For FY 2025-26 returns, always select Tab 1 (Income Tax Act 1961) or AY 2026-27.

Check AIS before filing: The Annual Information Statement on the portal shows all income linked to your PAN. Cross-check this against your return before submitting.

E-verify within 30 days: A return not verified within 30 days of filing is treated as not filed. Use Aadhaar OTP for fastest verification.

Salaried taxpayers in new ITR-1 scope: If you have two house properties and previously filed ITR-2, check whether you now qualify for the simpler ITR-1 under the expanded scope for AY 2026-27.

For a complete explanation of why this transition works this way, read our guide: Income Tax Act 2025 vs Income Tax Act 1961

Conclusion

The new ITR forms for AY 2026-27 bring one significant relief in the expansion of ITR-1 to cover two house properties. The extended August 31 deadline for non-audit business and professional income filers is also a welcome change. The corrigendum of April 10, 2026 corrected technical errors in the originally notified forms, and all taxpayers must use the updated utilities available on the portal.

The ITR forms for AY 2026-27 continue to be governed by the Income Tax Act 1961. New ITR forms under the Income Tax Act 2025 will come into effect only for Tax Year 2026-27 returns filed in 2027.

📚 Also Read: