TDS on Salary: Section 192 Complete Guide FY 2026-27

Table of Contents

What Is TDS on Salary and Why Every Salaried Professional Must Understand It

Every month, a portion of your salary is deducted before it reaches your bank account. This deduction is called TDS or Tax Deducted at Source. For millions of salaried professionals in India, TDS is the primary mechanism through which income tax is collected, yet most people have only a surface-level understanding of how it is calculated, what affects it, and what to do when it is wrong.

With over 7 years of experience working in finance and income tax, I have seen firsthand how incorrect TDS deductions cost professionals thousands of rupees every year, either through excess deductions that tie up cash flow, or under-deductions that lead to surprise tax demands at ITR filing time.

This guide explains everything you need to know about TDS on salary: how it is calculated, what you can do to reduce it, what happens when it is wrong, and the important changes under the Income Tax Act 2025 that affect TDS from April 2026.

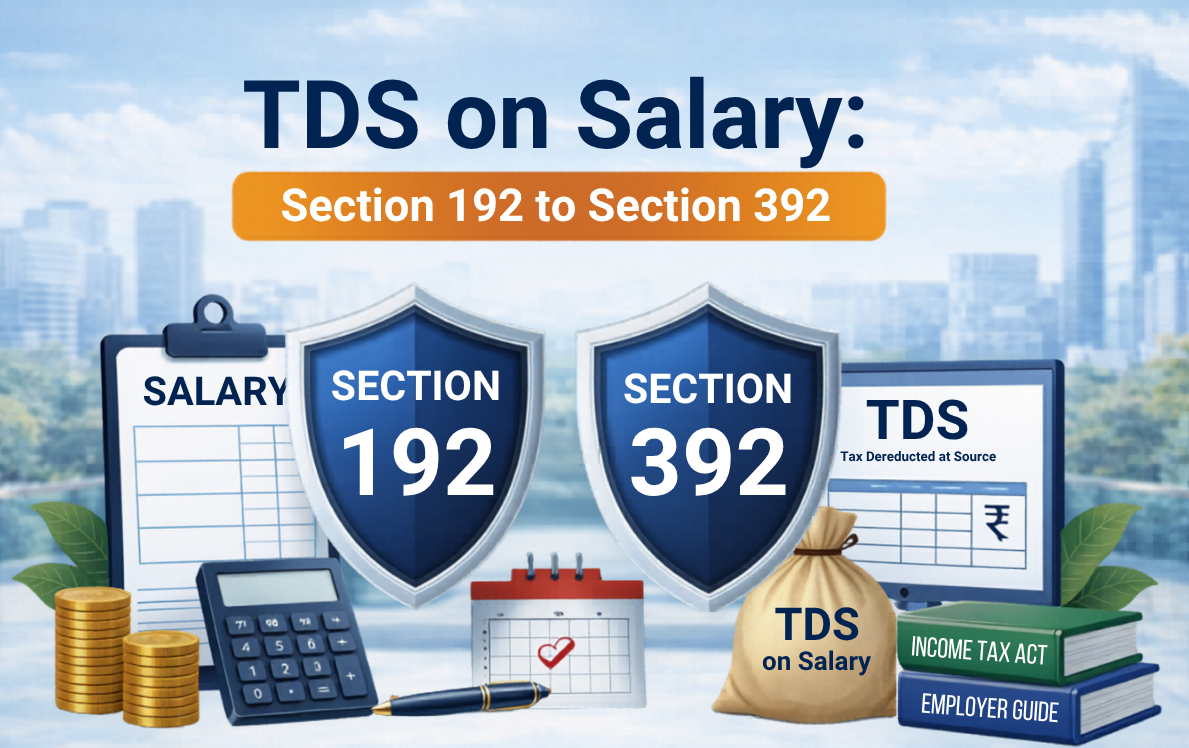

Important Update for FY 2026-27: Under the Income Tax Act 2025, Section 192 (TDS on salary) has been renumbered as Section 392. Additionally, Form 12BB (employee investment declaration) has been replaced by Form 124, and Form 24Q (employer’s quarterly TDS return) has been replaced by Form 143. The mechanics of TDS calculation remain the same. Only the section and form numbers change.

What Is TDS on Salary: Section 192 (Now Section 392)?

Section 192 of the Income Tax Act 1961 (now Section 392 under the Income Tax Act 2025) is the provision that requires every employer to deduct income tax from an employee’s salary before paying it out.

The employer acts as a tax collector on behalf of the government. Every month, the employer estimates the employee’s total annual income, calculates the applicable tax, divides it by the remaining months in the financial year, and deducts that amount from the monthly salary.

This deducted amount is then deposited with the government by the 7th of the following month (March TDS must be deposited by April 30).

How TDS on Salary Is Calculated: Step by Step

Understanding this calculation helps you verify whether your employer is deducting the right amount and take corrective action if not.

Step 1: Estimate Annual Gross Salary

The employer adds up all salary components: basic salary, HRA, special allowance, bonus, and any other taxable components for the full financial year.

Step 2: Deduct Exempt Allowances

Under the old tax regime, exempt allowances are subtracted:

- HRA exemption (based on rent paid and city)

- LTA exemption

- Children’s education allowance

- Any other Section 10 exemptions

Under the new tax regime, most exemptions are not available.

Step 3: Deduct Standard Deduction

- Old regime: Rs. 50,000

- New regime: Rs. 75,000

Step 4: Deduct Chapter VI-A Deductions (Old Regime Only)

Subtract declared investments and expenses:

- Section 80C up to Rs. 1,50,000

- Section 80D health insurance premium

- Section 80E education loan interest

- Any other declared deductions

Step 5: Arrive at Estimated Taxable Income

Gross salary minus all exemptions and deductions.

Step 6: Calculate Annual Tax

Apply applicable slab rates to taxable income. Add 4% health and education cess. Apply Section 87A rebate if eligible.

Step 7: Calculate Monthly TDS

Divide the annual tax by the number of remaining months in the financial year.

Formula: Monthly TDS = Annual Tax Liability divided by Remaining Months

TDS Calculation Example: Real Numbers

Example: Salaried Professional, Old Tax Regime

Gross Annual Salary: Rs. 12,00,000 HRA Exemption declared: Rs. 72,000 Standard Deduction: Rs. 50,000 Section 80C: Rs. 1,50,000 Section 80D: Rs. 25,000

| Step | Amount |

|---|---|

| Gross Salary | Rs. 12,00,000 |

| Less: HRA Exemption | Rs. 72,000 |

| Less: Standard Deduction | Rs. 50,000 |

| Less: Section 80C | Rs. 1,50,000 |

| Less: Section 80D | Rs. 25,000 |

| Taxable Income | Rs. 9,03,000 |

| Tax on Rs. 9,03,000 (old regime) | Rs. 86,100 |

| Add: 4% Cess | Rs. 3,444 |

| Annual TDS | Rs. 89,544 |

| Monthly TDS (divided by 12) | Rs. 7,462 |

Same Professional, New Tax Regime

| Step | Amount |

|---|---|

| Gross Salary | Rs. 12,00,000 |

| Less: Standard Deduction | Rs. 75,000 |

| Taxable Income | Rs. 11,25,000 |

| Tax on Rs. 11,25,000 (new regime) | Rs. 57,500 |

| Less: Section 87A Rebate | Rs. 57,500 (income below Rs. 12L) |

| Annual TDS | Rs. 0 |

| Monthly TDS | Rs. 0 |

This is why the new regime is beneficial for many professionals at the Rs. 12 lakh salary level — see our guide on how to save tax on 12 lakh salary. Zero TDS means higher monthly take-home throughout the year. For a complete regime comparison with real examples, read the old vs new tax regime guide.

How to Reduce Your Monthly TDS Legally

The most effective way to reduce TDS is to declare all eligible investments and deductions to your employer at the start of the financial year. This is done through Form 12BB (now Form 124 from FY 2026-27).

What to Declare in Form 124 (Earlier Form 12BB)

| Declaration | Deduction Section | Maximum |

|---|---|---|

| PPF, ELSS, EPF, LIC, School fees | Section 80C | Rs. 1,50,000 |

| Health insurance premium | Section 80D | Rs. 25,000 to Rs. 1,00,000 |

| Education loan interest | Section 80E | No limit |

| House rent paid | HRA Exemption | Depends on salary and city |

| Home loan interest | Section 24(b) | Rs. 2,00,000 |

| NPS contribution | Section 80CCD(1B) | Rs. 50,000 |

Declare these in April at the start of the financial year. The earlier you declare, the lower your monthly TDS throughout the year, which improves your monthly cash flow significantly.

For a complete list of all deductions available under the old regime, read the tax saving tips for salaried employees guide.

What Happens If You Do Not Submit Investment Declaration

If you do not submit Form 124 (earlier Form 12BB) to your employer, your employer assumes no deductions and calculates TDS on your full taxable salary without any deductions. This results in significantly higher monthly TDS deductions.

You will recover this excess TDS when you file your ITR and claim the deductions directly. However, the excess amount is locked with the government until your refund is processed, which can take 2 to 6 weeks after filing.

The practical impact: if your annual tax benefit from deductions is Rs. 46,800 (full 80C at 30% bracket), not declaring means you lose Rs. 3,900 per month from your take-home salary throughout the year.

New Tax Regime as Default from FY 2026-27

From FY 2026-27, the new tax regime is the default. This means if an employee does not submit Form 122 (the new declaration form for regime choice) to their employer, the employer must calculate TDS under the new tax regime.

Under the new regime, TDS is calculated with only the Rs. 75,000 standard deduction. No HRA, no 80C, no 80D deductions are considered.

Action required: If you want the old tax regime, you must submit Form 122 to your employer explicitly opting for it. Do not assume your employer will continue with last year’s regime automatically.

TDS When You Have Multiple Employers

This is a situation many professionals face, especially those who change jobs mid-year or work with two employers simultaneously.

Changing Jobs Mid-Year

When you join a new employer, submit Form 12B (now Form 122) to your new employer with details of:

- Salary received from previous employer

- TDS already deducted by previous employer

Your new employer will factor in the previous salary and TDS when calculating the remaining monthly TDS. Without this information, your new employer may under-deduct TDS, leading to a tax demand when you file your ITR.

Always collect Form 16 (Form 130 from FY 2026-27) from both employers. For step-by-step ITR filing guidance including handling two Form 16s, read how to file ITR online.

Two Simultaneous Employers

If you work for two employers at the same time, you must nominate one employer to deduct TDS on your aggregate salary from both. Provide the salary details from the second employer to your nominated employer via Form 122. The second employer does not deduct TDS separately once you have nominated one employer for aggregate TDS.

TDS on Perquisites and Benefits

TDS is not just deducted on your basic salary. It applies to the total value of salary including perquisites provided by your employer. From FY 2026-27 under the Income Tax Rules 2026, perquisite valuation rules have been tightened.

Taxable perquisites include:

- Company car used for personal purposes (fixed monthly taxable value)

- Employer-provided accommodation (percentage of salary based on city)

- Club memberships for personal use

- Personal expenses paid on company credit card

- Gifts above Rs. 15,000 per year (limit increased from Rs. 5,000 from April 2026)

Non-taxable perquisites include:

- Medical treatment at employer-approved hospitals

- Medical insurance premium paid by employer

- Employer NPS contribution up to 14% of basic salary

- Festival vouchers up to Rs. 15,000 per year (increased from April 2026)

What to Do If Too Much TDS Is Deducted

Excess TDS happens when:

- You did not submit investment declarations to your employer

- Your employer made a calculation error

- You have deductions your employer was not aware of

The solution is straightforward: file your ITR and claim all eligible deductions. The excess TDS already deducted will be refunded to your bank account after the return is processed.

Ensure your bank account is pre-validated on the income tax portal for faster refund credit. Track refund status at incometax.gov.in under Services.

What to Do If Too Little TDS Is Deducted

Under-deduction happens when:

- You declared deductions that you did not actually make

- You received a bonus or increment mid-year that was not accounted for

- You have income from other sources (FD interest, rental income) that your employer does not know about

In this case, you will have a tax demand when filing your ITR. You must pay this as Self-Assessment Tax (Challan 280) before filing. Interest under Section 234B and 234C may also apply if advance tax was not paid.

To avoid this, if you have income beyond salary, consider paying advance tax quarterly. Read the dedicated guide on advance tax payment for detailed instructions.

TDS and Form 26AS: How to Verify

Every TDS deduction from your salary must reflect in your Form 26AS (now Form 168 under the new Act). This is your consolidated tax statement available on the income tax portal.

Check your Form 26AS at least once every quarter to verify:

- TDS deducted matches what your salary slip shows

- Your employer has deposited the TDS with the government

- PAN is correctly recorded

If TDS deducted from your salary does not appear in Form 26AS, your employer may not have deposited it. This is a serious compliance issue. Raise it with your HR or finance team immediately. TDS that does not appear in Form 26AS cannot be claimed as credit when filing your ITR.

Key Form Changes Under Income Tax Act 2025

| Old Form | New Form | Purpose |

|---|---|---|

| Form 12BB | Form 124 | Employee investment declaration to employer |

| Form 16 | Form 130 | TDS certificate issued by employer to employee |

| Form 24Q | Form 143 | Employer’s quarterly TDS return |

| Form 26AS | Form 168 | Annual tax statement showing all TDS credits |

| Section 192 | Section 392 | TDS on salary provision |

For FY 2025-26 ITR filing (due July 2026), old form numbers still apply. New form numbers apply from FY 2026-27 onwards. Read the complete guide on Form 16 replaced by Form 130 for detailed information.

File your return directly at the official portal: incometax.gov.in

Frequently Asked Questions on TDS on Salary

What is Section 192 of the Income Tax Act?

Section 192 (now Section 392 under Income Tax Act 2025) requires employers to deduct income tax from employee salaries before payment. The employer calculates annual tax liability, divides by remaining months, and deducts that amount monthly.

How is TDS on salary calculated?

TDS is calculated by estimating annual taxable salary (after exemptions and deductions), applying slab rates and cess to determine annual tax, then dividing by the remaining months in the financial year to get monthly TDS.

Can I reduce my monthly TDS?

Yes. Submit Form 124 (earlier Form 12BB) to your employer at the start of the financial year declaring all eligible investments and deductions including Section 80C, 80D, HRA, and home loan interest. The employer factors these in when calculating monthly TDS, reducing the amount deducted each month.

What if my employer deducts too much TDS?

File your ITR and claim all eligible deductions. The excess TDS will be refunded to your bank account after the return is processed. Ensure your bank account is pre-validated on the income tax portal for faster refund.

What is Form 26AS and how does it relate to TDS?

Form 26AS (now Form 168) is your annual tax credit statement showing all TDS deducted on your PAN from all sources. Verify it quarterly to ensure your employer is depositing TDS correctly. TDS that does not appear in Form 26AS cannot be claimed as credit in your ITR.

Is TDS deducted on bonus and increments?

Yes. Bonus, performance pay, and increments are part of salary income and TDS applies to them. If a bonus is paid mid-year, your employer recalculates the annual tax estimate and adjusts the remaining monthly TDS accordingly, which may result in higher deductions for the rest of the year.

What if I have income from other sources besides salary?

Your employer deducts TDS only on salary income. Income from FD interest, rental income, capital gains, or other sources is not accounted for by your employer. You must pay advance tax on this additional income quarterly to avoid interest under Section 234B and 234C.

What happens to TDS if I resign mid-year?

Your employer deducts TDS up to your last working day. Collect Form 16 (Form 130 from FY 2026-27) from your previous employer showing salary paid and TDS deducted. Submit this information to your new employer via Form 122 so they can account for it in their TDS calculation for the rest of the year.

Summary: Key Things to Do Every Financial Year

- April: Submit Form 124 to your employer declaring all investments and deductions for the year. Choose your tax regime explicitly.

- April to March: Check Form 26AS quarterly to verify TDS is being deposited correctly.

- June: Collect Form 130 (earlier Form 16) from your employer after it is issued.

- July: File ITR before the deadline. Reconcile Form 130 with actual income and deductions.

- Year-round: If you have income beyond salary, pay advance tax quarterly to avoid interest.

For the complete picture of income tax including slabs, deductions, and ITR filing, read the Complete Income Tax Guide India 2025-26 and 2026-27. And to understand all deductions that can reduce your TDS, the Section 80C guide, Section 80D guide, and HRA exemption guide cover each deduction in detail. Key salary-related exemptions include gratuity tax exemption and leave encashment tax exemption at retirement. For a full list of TDS rates across income types, see the TDS rate chart FY 2025-26.

Questions about your specific TDS situation? Drop them in the comments below.

📚 Also Read: