Tax Saving Tips for Salaried Employees FY 2026-27

Table of Contents

Tax Saving for Salaried Professionals: What Has Changed in FY 2026-27

A new financial year means a fresh opportunity to plan your taxes correctly from day one. FY 2026-27 is particularly significant because the Income Tax Act 2025 has replaced the Income Tax Act 1961, bringing several practical changes that directly affect how salaried professionals save tax.

This guide covers every tax saving opportunity available to you in FY 2026-27, including the changes that came into effect from April 1, 2026, that most people are not yet aware of.

New from April 1, 2026: The terms “Financial Year” and “Assessment Year” have been replaced by a single term called “Tax Year” under the new Income Tax Act 2025. FY 2026-27 is now officially called Tax Year 2026-27. For clarity, this article uses both terms interchangeably.

Step 1: Choose the Right Tax Regime First

Every tax saving decision this year starts with one question: old regime or new regime?

The new regime is the default from FY 2023-24. If you do not actively choose, you are automatically in the new regime.

| Feature | New Regime | Old Regime |

|---|---|---|

| Zero tax limit | Rs. 12,75,000 (salaried) | Rs. 5,50,000 |

| Standard Deduction | Rs. 75,000 | Rs. 50,000 |

| Section 80C | Not available | Up to Rs. 1,50,000 |

| HRA Exemption | Not available | Available |

| Section 80D | Not available | Up to Rs. 1,00,000 |

| Home loan interest | Not available | Up to Rs. 2,00,000 |

| Employer NPS (80CCD2) | Available (14% of basic) | Available (14% of basic) |

For a detailed salary-wise comparison with real calculations, read the old vs new tax regime guide.

Quick rule: If your total deductions (80C + 80D + HRA + home loan interest) exceed Rs. 3,75,000, the old regime likely saves more. If they are below Rs. 2,00,000, the new regime almost always wins.

Tax Saving Tips for Salaried Employees: New Regime

Tip 1: Maximize Employer NPS Contribution (Section 80CCD2)

This is the single most powerful tax saving tool available in the new regime.

Your employer can contribute up to 14% of your basic salary to your NPS account. This entire amount is deductible from your taxable income even under the new regime.

Example: Basic salary Rs. 60,000 per month (Rs. 7,20,000 per year). Employer NPS at 14% = Rs. 1,00,800 deduction. At 20% tax bracket this saves Rs. 20,160 in taxes annually.

If your employer does not currently offer NPS contribution, request HR to restructure your CTC to include it. The total CTC stays the same but your tax liability reduces significantly.

Tip 2: Children’s Education Allowance (Major Update FY 2026-27)

This is one of the biggest changes most salaried professionals do not know about yet.

| Allowance | Old Limit | New Limit from April 2026 |

|---|---|---|

| Children’s Education Allowance | Rs. 100 per month per child | Rs. 3,000 per month per child |

| Hostel Allowance | Rs. 300 per month per child | Rs. 9,000 per month per child |

If you have two children, the combined annual tax-free allowance is now Rs. 2,88,000 per year. Check your April 2026 salary slip and inform HR if this has not been updated.

Tip 3: Tax-Free Salary Components to Include in CTC

- Gift vouchers: Up to Rs. 15,000 per year tax-free from FY 2026-27 (increased from Rs. 5,000)

- Meal allowance: Up to Rs. 200 per meal, twice a day is tax-free

- Mobile and internet reimbursement: Actual expenses for official use are tax-free

- Medical loans from employer: Now exempt up to Rs. 2,00,000 (previously only Rs. 20,000)

Tax Saving Tips: Old Regime

Tip 4: Exhaust Section 80C Completely (Rs. 1,50,000)

Before investing anything new, list what you already have:

- EPF contribution (automatic from salary)

- Children’s tuition fees (up to 2 children)

- Home loan principal repayment

- Existing LIC premiums

Calculate the gap up to Rs. 1,50,000. Fill only that gap with ELSS SIP, PPF, or NSC. Do not over-invest beyond the limit as excess gives no additional deduction.

Complete list of all 14 options: Section 80C deductions guide.

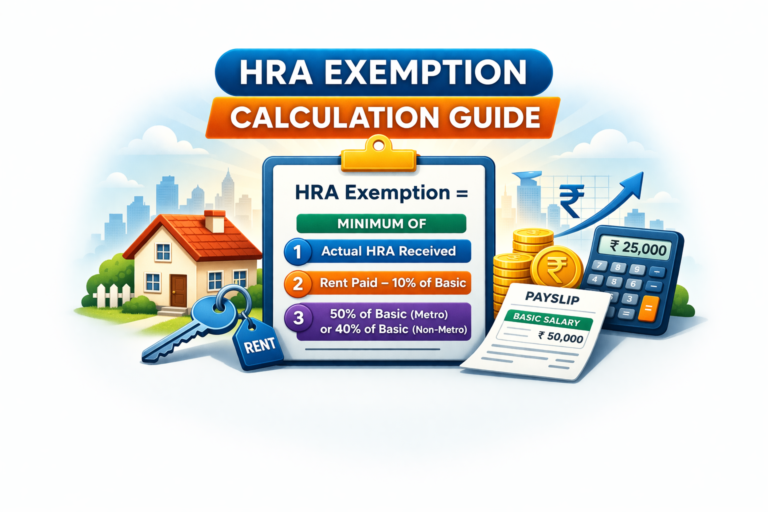

Tip 5: HRA Exemption (Big Change for 4 More Cities)

New for FY 2026-27: Eight cities now qualify for 50% HRA exemption.

Newly added cities (50% from April 2026): Bangalore, Hyderabad, Pune, Ahmedabad

If you live in any of these four cities, your HRA exemption cap increases from 40% to 50% of basic salary from FY 2026-27.

Example: Basic salary Rs. 60,000/month. Earlier cap: Rs. 24,000/month (40%). New cap: Rs. 30,000/month (50%). Difference: Rs. 6,000/month = Rs. 72,000/year in additional exemption.

Note: For FY 2025-26 ITR (filed July 2026), the old 4-city rule still applies. The 50% rate for new cities applies from FY 2026-27 onwards.

Use our HRA Calculator to find your correct exemption. Read the HRA exemption guide for all scenarios.

Tip 6: Section 80D: Claim Parents Separately

Self and family deduction and parents deduction are two separate buckets. Both can be claimed together.

- Self and family below 60: Rs. 25,000

- Senior citizen parents: Rs. 50,000

- Senior citizen parents with no insurance: Actual medical bills up to Rs. 50,000

Maximum combined: Rs. 1,00,000. Read the Section 80D guide for complete details. If you are comparing insurers, our overview of public sector insurance companies covers government-backed options like New India, Oriental, and United India.

Tip 7: Home Loan: Two Separate Deductions

- Principal repayment: Under Section 80C, within Rs. 1,50,000 limit

- Interest on self-occupied property: Up to Rs. 2,00,000 per year separately

Get your annual home loan certificate from your lender showing both amounts separately. Submit to employer for TDS calculation.

Tip 8: NPS Additional Rs. 50,000 Over and Above 80C

Section 80CCD(1B) gives Rs. 50,000 deduction for your own NPS contribution, completely separate from 80C. This takes total deductions from this cluster to Rs. 2,00,000.

At 30% tax bracket: Rs. 50,000 extra deduction saves Rs. 15,600 in taxes. Every year.

Important New Changes in FY 2026-27 Every Salaried Professional Must Know

Change 1: Salary Structure Likely Changed

Under the new Labour Code, basic salary must be at least 50% of CTC. Many companies have restructured salaries from April 2026. Higher basic means higher EPF and different HRA calculation. Review your April salary slip carefully.

Change 2: Form 16 Replaced by Form 130

The last Form 16 will be issued in June 2026 for FY 2025-26. From June 2027, your employer will issue Form 130 instead. It is more detailed and fully system-generated. Read the complete guide on Form 16 replaced by Form 130.

Change 3: Revised Return Deadline Extended

You can now file a revised ITR up to March 31 of the following year with a fee. Previously the deadline was December 31. More time to correct mistakes in your return.

Change 4: TCS on Foreign Travel Reduced

TCS on overseas tour packages reduced from 5% to 2%. On a Rs. 5 lakh international tour, TCS is now Rs. 10,000 instead of Rs. 25,000.

Change 5: Section Numbers Have Changed

| Old Section | New Section | What It Covers |

|---|---|---|

| Section 80C | Section 123 | Investment deductions |

| Section 80D | Section 124 | Health insurance |

| Section 24(b) | Section 22 | Home loan interest |

| Form 16 | Form 130 | TDS certificate |

| Form 26AS | Form 168 | Annual tax statement |

Benefits remain exactly the same. Only the numbers have changed. For FY 2025-26 ITR filing this July, use old section numbers.

Tax Saving Action Plan: Start in April

The biggest mistake is waiting until January to plan. Here is what to do in April itself:

- Decide old or new regime. Inform employer immediately via investment declaration.

- Check April salary slip for education allowance updates and salary restructuring.

- Start ELSS SIP from April if in old regime. Monthly SIP from April beats March lump sum.

- Make first PPF deposit before April 5 to earn interest for the full month.

- Submit investment declaration to employer early to prevent excess TDS deduction.

- If in Bangalore, Hyderabad, Pune, or Ahmedabad, inform employer about 50% HRA rate from FY 2026-27.

- Ask HR about employer NPS contribution if not already in your CTC.

- Review your family’s insurance coverage. A comprehensive family life insurance plan ensures both life cover and health protection are in place before the financial year begins.

Frequently Asked Questions

What is the zero tax salary limit in FY 2026-27?

Under new regime: Gross salary up to Rs. 12,75,000 for salaried professionals. With optimal salary structuring including employer NPS and education allowances, this can extend closer to Rs. 15,00,000. Under old regime: Taxable income up to Rs. 5,00,000 attracts zero tax after Section 87A rebate.

Is HRA 50% or 40% for Bangalore in FY 2026-27?

50% from FY 2026-27. Bangalore, Hyderabad, Pune, and Ahmedabad have been added to the metro category from April 2026. For FY 2025-26 ITR (filed July 2026), Bangalore still gets 40%. Read the complete HRA exemption guide.

Can I change my tax regime mid-year?

Not mid-year with your employer. However, when you file your ITR, you can choose a different regime than what your employer applied for TDS. The difference is adjusted as a refund or additional payment at filing time.

What are the income tax slabs for FY 2026-27?

Same as FY 2025-26. No changes announced in Budget 2026. Read the complete income tax slabs guide for FY 2026-27.

What is the maximum Section 80C deduction for FY 2026-27?

Rs. 1,50,000 combined across all 80C instruments. No change from previous years. Read the complete Section 80C guide for all eligible options.

Quick Reference: Tax Saving Checklist FY 2026-27

| Action | Regime | Maximum Benefit |

|---|---|---|

| Decide regime and inform employer | Both | Correct TDS all year |

| Standard deduction | Both | Rs. 75,000 (new) / Rs. 50,000 (old) |

| Employer NPS contribution | Both | 14% of basic salary |

| Education allowance (updated) | Both | Rs. 2,88,000 (2 children) |

| Gift vouchers from employer | Both | Rs. 15,000 |

| Section 80C investments | Old only | Rs. 1,50,000 |

| Additional NPS 80CCD(1B) | Old only | Rs. 50,000 |

| HRA exemption | Old only | Variable (50% for 8 cities now) |

| Section 80D health insurance | Old only | Rs. 1,00,000 |

| Home loan interest | Old only | Rs. 2,00,000 |

Tax planning is not a year-end activity. Starting in April gives you the full year to optimize. Beyond Section 80C, several other deductions are available: Section 80EEA (affordable housing loan), Section 80GG (rent without HRA), Section 80P (cooperative societies), Section 80TTB (senior citizens’ interest income), Section 80U (disability), and Section 80E (education loan interest).

For the complete picture of income tax including how to file your return, read the Complete Income Tax Guide India 2025-26 and 2026-27.

Questions about your specific tax situation for FY 2026-27? Drop them in the comments below. Women taxpayers should read our guide on income tax for women FY 2026-27. Check the new PAN rules 2026 before filing. The tax saving limits above were set by Union Budget 2025. Freelancers should read our guide on income tax for freelancers, explore freelancer tax deductions FY 2026-27, and check Section 44ADA. Property owners should read about income from house property rules.

📚 Also Read:

- Section 80C Deductions: Complete List for FY 2025-26

- Standard Deduction FY 2026-27: Rs. 75,000 for New Regime

- HRA Exemption Calculation Guide FY 2026-27

- Maximize Your Savings with Tax Saving Schemes Beyond 80C

- Tax Planning for Salaried Employees in India 2025

- Complete Income Tax Guide India 2025-26 & 2026-27